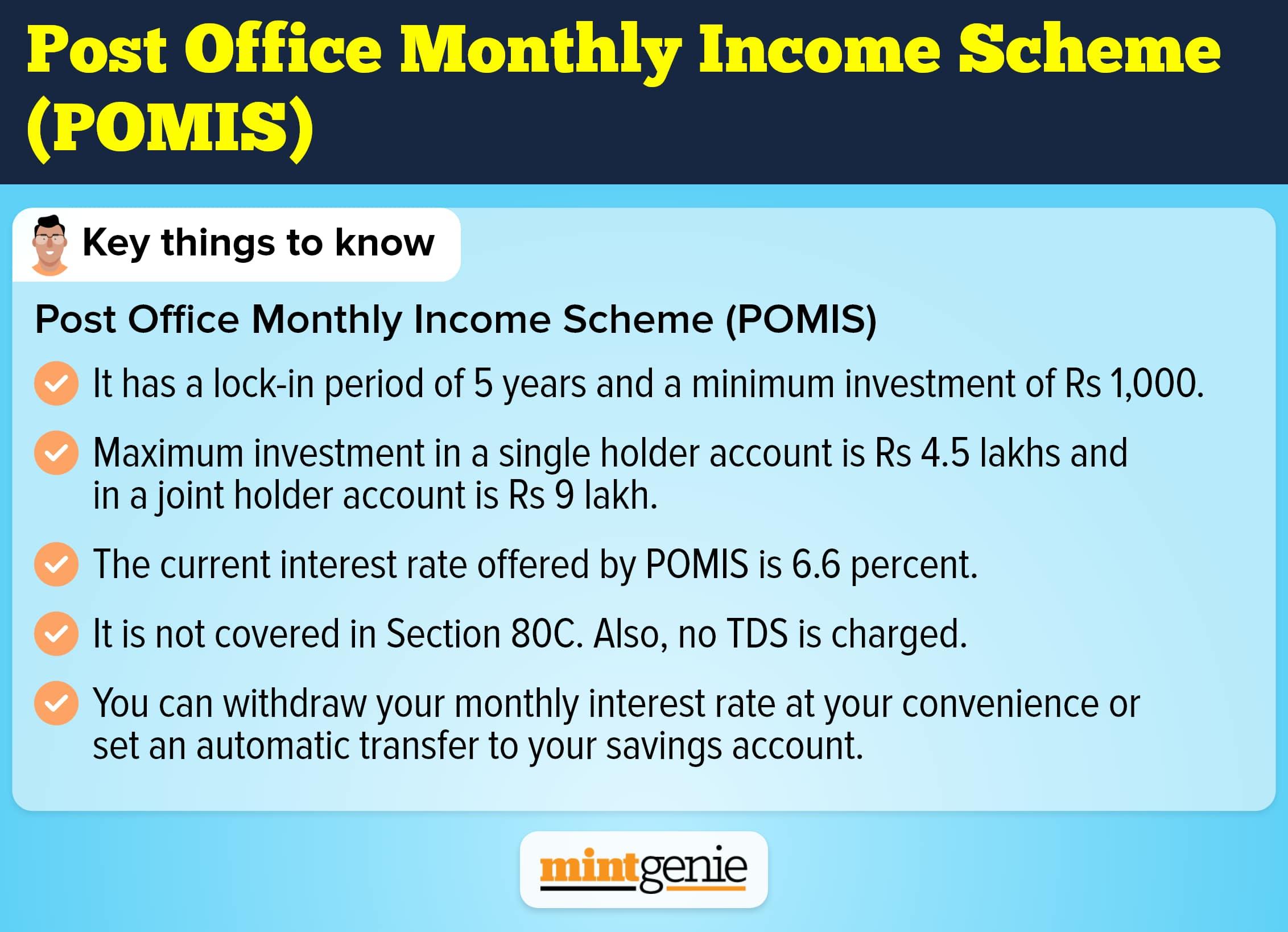

The post office time deposit is also known as post office fixed deposit (POFD). It is similar to the fixed deposit (FD) facility of banks. This scheme is offered by the India Post. The scheme provides a guaranteed return to the depositor who deposits an amount for a fixed period of time.

Opening a POTD account

POTD accounts can be opened by any individual who is a citizen of India. The account can be opened with either cash or cheque. The date of realization of cheque is recorded as the opening date of the account.

The minimum amount required to open such an account is Rs. 1,000. There is no cap on the maximum limit of the amount that can be deposited. The account can also be opened jointly by a maximum of three persons. An individual can create multiple accounts without any restriction. He/she has the freedom to transfer his/her account from one post office to another within India.

Lock-in period

One can lock in their money for a period of either one, two, three, or five years. The tenure can also be extended by sending a formal application to the post office.

Interest rate

The interest rate under this scheme is revised regularly. It is calculated on a quarterly basis and paid on an annual basis. The latest revised rates for the POTD as per the second quarter of the financial year 2021-22, are as follows:

1 Year = 5.5%

2 Years = 5.5%

3 Years = 5.5%

5 Years = 6.7%

Tax exemption

The depositors can also claim the income tax exemptions worth Rs. 1.5 lakh under Section 80C of the Income Tax Act, 1961. However, these exemptions are available only for the lock-in period of five years.

Withdrawal before the maturity period

The depositor is not allowed to withdraw money within six months of the deposit. If the corpus is withdrawn prematurely between six months and 12 months, then the rate of interest offered will be the rate prescribed for a savings account.

The post-office time deposit is best suited for those who do not possess a high-risk appetite.