Debt traps are a big problem, and most debtors don't even realise until they're in one. To be financially fit, however, one must be aware of the warning indications that one is going to fall into a debt trap. Even debt consolidation mistakes should be avoided.

Because it might go undiscovered until a person's neck-deep in it, a debt trap can be even more hazardous than usual. People are, at times, compelled to take out a second loan to pay off their first.

Debt traps are caused by a variety of factors

Not figuring out how you got into debt

Debt consolidation is a way to get out of debt. But if you don't care about uncovering the fundamental cause, you may not be able to put a stop to the problem. Determining the actual cause of your debt may also allow you to alter some of your spending patterns in the future. It is therefore imperative that you address the root cause of your financial difficulties if you want to get yourself out of debt.

Not verifying your credit card use

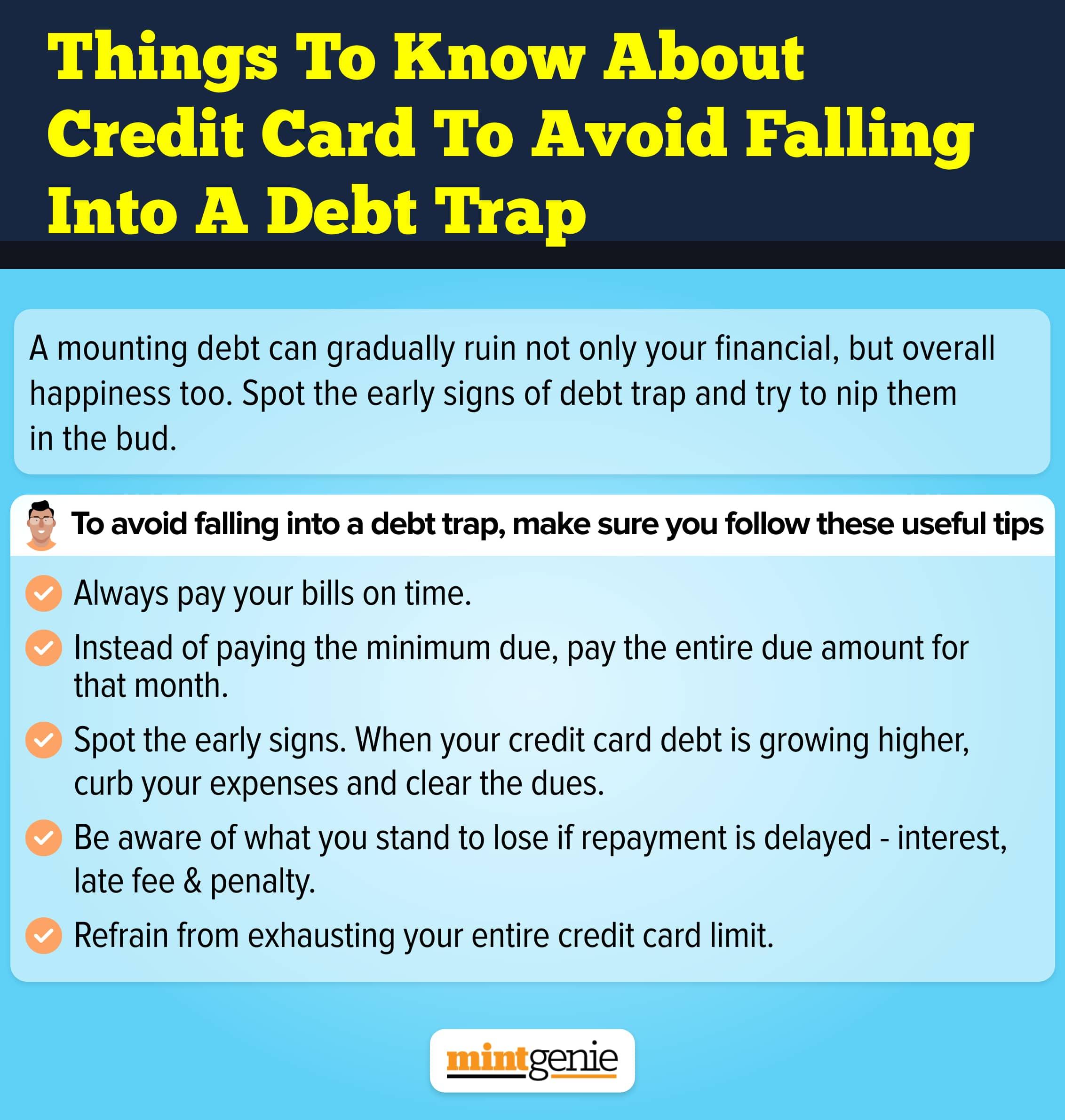

Getting into credit card debt is the quickest way to get into trouble. This is due to the fact that they come with large incentives and most individuals are easily swayed by them. It's crucial to note that credit card interest rates can range from 16 to 32 percent yearly. Because of this, anytime you use your credit card, you should keep a record of it.

Payment of credit card bills on time comes in second place. If you pay your credit card bills after the interest-free period has expired, you may be charged interest, and late payments might result in steep penalties.

Not having a repayment plan before borrowing

Even while credit cards and loans may seem appealing, it's crucial to have a repayment strategy in place before you take the plunge. This can help you plan your repayment strategy by giving you an idea of what your EMI is likely going to be before you apply for the loan. Remember, borrowing money is easy, but repaying it might be difficult if you don't have a strategy.

Ignorance of research & information

To get a loan quickly, many people apply for the first one that comes their way. Unchecked, this can lead to a significant financial trap. Doing appropriate research should be your first move anytime you become aware that a loan is required.

Defaulting loan repayments

Your score will be lowered if you default on your EMI payments. Regularly failing to pay your monthly EMIs signals that you have a major financial management problem that can lead to a debt trap. Borrow according to your ability to repay and make your payments on schedule (EMIs).

Therefore, it is clear that loans can be a good financial asset but if not used carefully, they can turn into a disaster. So, to summarise, it's important to practise caution when using credit cards. You can prevent debt traps by reading your contract carefully and paying your obligations on time.

Don't get caught up in high-interest lending schemes such as payday and title loans, pawn shop loans, renting to own loans or loan repayments from your tax refund. No one should have to pay to fix their credit. Your credit record can be corrected and your credit score can be improved by yourself, with a little time and effort.