Gold and real estate have long been cherished by generations as tangible and traditional ways to preserve wealth. In fact, real estate is a preferred mode of savings for 49% of Indian households, much higher than other asset classes such as equity, gold, bank deposits, etc. The allure of these asset classes is in their perceived stability and intrinsic value.

However, the potential of equities as a wealth-building avenue often goes unnoticed by investors. While equities may carry short-term risks, their long-term performance has consistently outshined other asset classes.

So, understanding the importance of equity investments is crucial for long-term wealth creation. To illustrate the potential of equities, we analysed the returns generated by different asset classes from 1999 to 2023. Here are the asset classes under our analysis:

Equities: To calculate equity returns we considered the Nifty 500 index returns. The Nifty 500 index represents the top 500 companies selected based on market capitalisation. The total return index measures the total return of an investment over a specific period, including both price changes and dividend income.

Real Estate: To calculate real estate returns, we have used the RBI Residex Index. This index provides an average measure of real estate prices across India's top 7 cities.

Gold: The calculation of gold returns is based on the average price of gold in domestic markets.

Public Provident Fund (PPF): PPF offers a fixed interest rate, making it a reliable option for risk-averse investors. To calculate PPF returns, we have considered the interest rates decided by the EPFO for various years.

Fixed Deposit (FD): Fixed deposits provide a predictable and fixed interest rate on bank deposits. For calculating FD returns, we have considered the 1-3 year deposit rates offered by 5 major public sector banks or 5 major banks as provided by RBI.

Return calculation methodology

The calculation of average returns during different holding periods involves using a moving average approach. For instance, to calculate the average returns over a 5-year holding period, consecutive years are considered, starting with 1999 to 2004 as the initial period. The average returns for this specific 5-year period are computed. After this, the subsequent 5-year period, from 2000 to 2005, is analysed, and its average returns are determined. This process is repeated for each successive 5-year period, creating a moving average calculation.

To derive an overall average, the average returns from all the different moving 5-year periods are combined. We picked a moving average as it considers all time periods equally, reducing the impact of outliers.

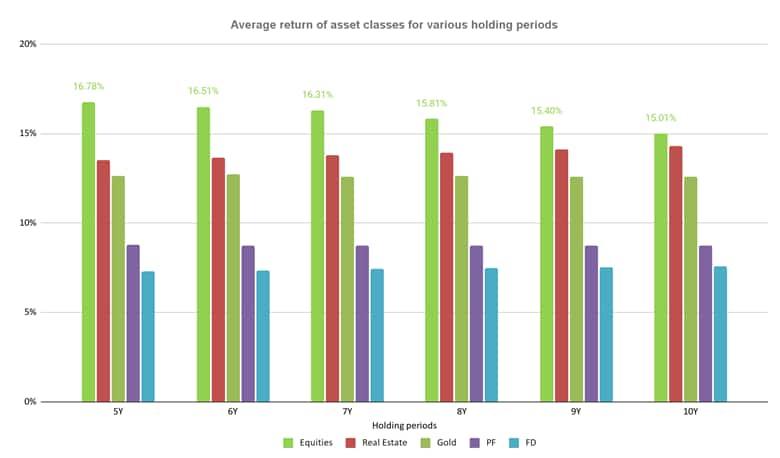

Returns in different holding periods across asset classes

From the moving average approach, we see that average returns in equity are the highest for all 5-10 year holding periods irrespective of the timing of the investment in the past 24 years.

● Equities have consistently delivered attractive returns, averaging 15% across various holding periods ranging from 5 to 10 years. This implies that if you had invested in equities and held them for any consecutive 5, 6, 7, 8, 9, or 10-year period between 1999 and 2023, you would have generated an average return of 15%.

● In comparison, real estate takes the second spot with an average return of 13-14% over different holding periods. Gold follows closely, ranking third with an average return of 12%.

● These findings highlight the potential for significant wealth creation through equities, making them a good choice for long-term investors seeking higher returns.

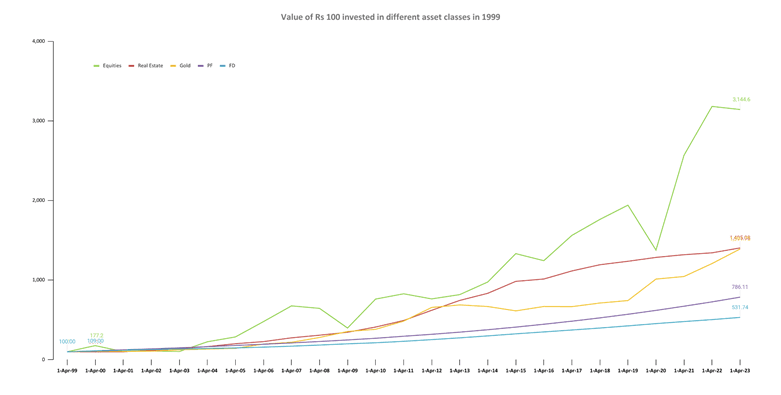

Imagine if you had invested ₹100 in 1999 in different asset classes and held onto your investments until today. How would your initial investment look in 2023?

If you had chosen equities, your investment would have grown to an impressive ₹3,144. Equities have had major dips and rises in the past 20 years but the short-term volatility tends to smooth out. They tend to go up in the long term as economies will continue to expand, and companies can continue to grow their revenues and profits, which typically leads to an increase in stock prices.

In comparison, if you had invested in real estate, your investment would be valued at ₹1,405 today, significantly lesser than the equity component. While real estate can offer potential gains, it is a high-risk asset since its price is dependent on several factors including supply-demand, economic conditions, and interest rates. The complex regulatory landscape and project delays in the Indian real estate sector can also impact returns. Ongoing expenses, such as maintenance and property taxes, further reduce overall gains. Moreover, periods of exponential growth in real estate prices are challenging to predict, making it uncertain for investors. For instance, the average annual growth rate for housing prices significantly varied between 2010-2016 (17%) and 2017-2023 (5%).

In gold, your investment of ₹100 would be ₹1,391 in 2023. As can be seen from the chart, gold has given good returns in times of economic uncertainty: post-2008 financial crisis, COVID-19, and the Russia-Ukraine war. However, when the economic conditions are stable, gold tends to underperform other asset classes. For instance, in 2013-19, gold prices grew at a CAGR of just 1.3% while they grew at a CAGR of 9.2% in 2020-22.

The takeaway

While gold, real estate, and other asset classes provide diversification to your portfolio, equities stand out as the clear winner in terms of generating significant returns. So, equities remain the ideal choice not just for seasoned investors, but for anyone looking to generate long-term wealth.

Naveen KR is Senior Director - Investment Products at Windmill Capital.