Q1. I work in a private company. My employer has given me health insurance worth ₹5 lakhs. Do I still need to have separate personal health insurance?

A personal health insurance plan, different from and in addition to the one provided by the employer can provide you with extra financial protection in case of unexpected medical expenses. Here is how:

Covering gaps in employer-provided coverage: Your employer-provided health insurance may not cover certain types of treatments or may have limits on the amount it will pay for certain procedures. For example, it may not cover the cost of prescription drugs or may have a cap on the amount it will pay for hospital stays. A separate health insurance policy can help cover these gaps, thus ensuring that you do not have to compromise on the medical care for want of financial resources.

Providing portable coverage: If you leave your job, you could lose your employer-provided health insurance if the new employer does not provide one. If you have a pre-existing medical condition, it may make it difficult for you to obtain coverage from a new employer. A separate health insurance policy can provide you with continuous coverage, even if you change jobs or experience a gap in employment.

Covering dependents: Your employer-provided health insurance may /may not cover your dependents, like spouse and children or dependent . In this case, you may need to purchase a separate policy to ensure that they have access to necessary medical care.

Personalised cover: Depending on the personal health insurance plan you choose; you may be able to customise your coverage to better meet your specific needs. For example, you may be able to choose a plan with a higher deductible and lower premiums, or a plan with a lower/no deductible and higher premiums.(A deductible is a portion of the claim that an individual will have to bear before the insurance company honours the claim).

You may also be able to choose a plan that covers specific types of treatments or procedures, such as maternity care or mental treatment coverage, etc. Personal health insurance plans may also offer different levels of coverage, which allow you to choose the level of coverage that best fits your budget and needs. This level of customization is usually not available with employer-provided health insurance plans.

Offering additional benefits: A separate health insurance policy may offer additional benefits that are not included in your employer-provided coverage. For example, it may cover preventive care services, such as annual health check-ups, at no additional cost. It may also offer coverage for alternative therapies, such as those under AYUSH, which may not be covered under your employer-provided plan.

Adequate cover: Your company insurance may not be sufficient to cover the cost of major medical expenses. If the claim amount exceeds ₹5 lakhs, even with company insurance, you would have to pay a portion of your healthcare costs from your pocket. Having additional insurance can help to cover these costs and protect you financially, especially during major illnesses.

Pre-existing conditions: It is very important to have personal health coverage at an early age when you do not have any pre-existing medical conditions. Even if you have group insurance coverage, you may lose it when you retire or when you change jobs. If you apply for personal health coverage at this time and have recently developed a medical condition, your proposal might be rejected, you may be charged additional premium, or exclusions may be applied to your coverage.

Co-existence of both policies: In case of a claim over and above the corporate cover, it is important to declare at the hospital desk where the cashless claims are applied, the existence of another personal policy. In that even the claim over and above the corporate cover could be claimed from the personal insurance as well.

It is important to carefully consider your healthcare needs and budget when deciding whether to purchase additional health insurance. Please consult a financial advisor to make an informed decision.

Q2. I am 24 and got married recently. One of my friends is investing in mutual funds. I am interested too, but how do I decide which mutual fund is best for me?

Before you look at the funds, be clear about your financial goals. Then choose the fund or funds that are the best match for your goals. Your investment horizon, the amount you plan to invest, and your risk appetite are all important factors. As a first-time investor, it is important for you to understand the risk-reward metrics before investing in any fund.

You may have some goals planned for different time periods and that should be the basis for selecting the fund category and the specific fund.

For example, if you are investing for the long term, a short-term market downturn should not concern you. It is the compounding gains over time that will help you reach long-term financial goals.

For shorter-term goals you may choose more conservative investments, such as debt mutual funds or fixed-income investments. These tend to be more resilient against equity market movements.

There are many tools available online that can help you to understand your risk tolerance—that is, how much market volatility you can handle and how you can evaluate funds.

Avoid giving too much emphasis to returns. Instead check the asset management company's credibility, how they counter risk and the consistency in long-term returns.

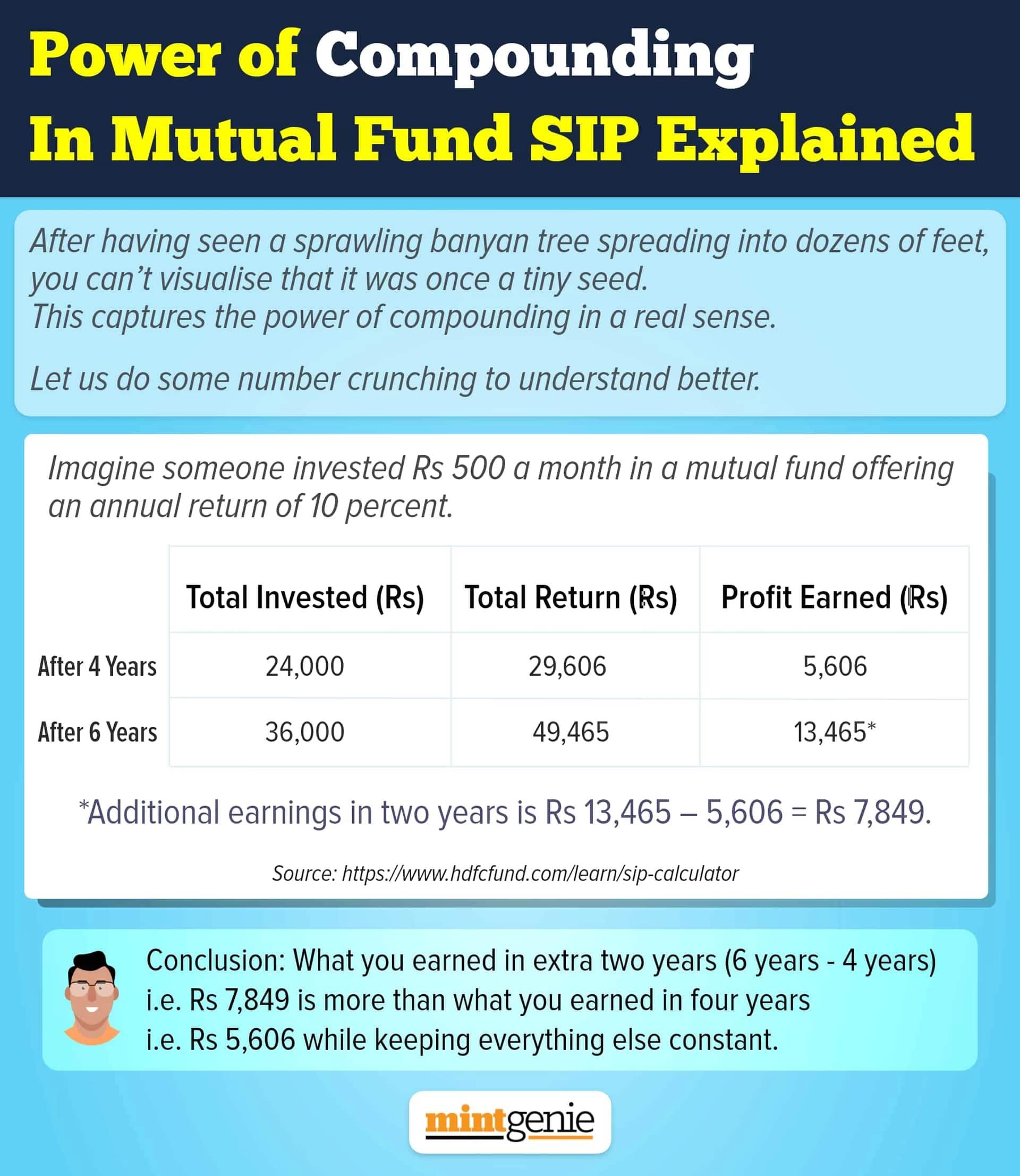

Considering your age, you may start with a combination of index funds and flexi cap funds. Systematic Investment Plan (SIP) is the best strategy to start your financial journey. Investments can be staggered through a few weeks or months for better price averaging.

Post investment, you must monitor your schemes at fixed intervals for changes in the scheme's fundamentals.

Q3. I am 30 and a regular investor. The US market is not performing well now, but it might recover. Should I invest in the US market now?

The global economy goes through multiple market cycles. The US market is currently witnessing a significant correction due to recession fears, high inflation, and interest rate movements. Most stocks in the US markets, especially those of the technology sector have corrected. It is uncertain if the correction would continue. While there has been some impact on growth prospects, most of these companies are global market leaders and generate free cash flows.

Geographical diversification offers stability to your portfolio. Over the long run, markets in developed countries tend to be less volatile than those of the emerging economies. By investing in the US stock market, you can participate in the global growth story. The current period of uncertainty provides an opportunity to build long-term international exposure.

It is advisable to follow certain guidelines before investing internationally. Consider a 10% to 15% allocation of the portfolio for diversification. It is always advisable to invest in diversified exchange traded funds or mutual funds. Also, such investments should be staggered as it helps to take advantage of different market phases.

Q4. I am 27 and earning well. I have a few savings accounts and some FDs in my name. I haven’t invested anywhere as I am unaware where to start. Should I start now or later? How?

There is no right time to invest. Saving money is important, but it’s only part of the financial story. It is important to build enough funds to cover expenses of 3 to 6 months as an emergency corpus. This can be parked in a savings account, FDs, or liquid funds. Investing the rest in the financial markets will offer many advantages.

Investing is an effective way to put your money to work and build wealth. Smart investing will allow your money to outpace inflation and grow in value, thanks to the power of compounding and the risk-return trade-off.

When is the right time to start investing?

It is good to start as early as you can. That will help you tap the power of compounding to make your money grow faster.

Before you consider the “when”, it is important to understand “why” you want to invest. To know this, you need to be aware of your:

Financial goals: What do you want to achieve through your investments? List your financial goals. Identify your short-, medium- and long-term goals. This will help you determine the right investments.

Risk tolerance: There is an element of risk associated with every investment. You must know how far you are comfortable taking risks. Investments like stocks are considered riskier but have the potential to yield higher returns over the long term. Other investments, such as bonds and cash, are considered less risky but are likely to provide lower returns.

Time horizon: Once you know your goal, you will also know when you would require the funds to achieve that goal. That time horizon will determine your asset allocation—stocks, bonds, short-term investments, etc.

Choosing the right asset class based on your goal and risk appetite will also help you beat inflation in the long run. It is also important to diversify and create a well-balanced portfolio. You must spread your risk over different asset classes.

How does one start to invest?

For beginners, a mutual fund, or an exchange traded fund (ETF) is a good equity investment.

However, it all boils down to when you want to use the money. Your time horizon is extremely important as it will allow your investments to grow at its own pace, flourishing slowly. If you have a shorter time horizon (less than five years) you should not look at the equity market as the time is too short for successful wealth generation. However, if you do not need your investments back for another ten years or so, then it is better to invest in the stock market via mutual funds.

Why must you be realistic about your goals?

Some goals are common to most people.

· Take care of immediate needs

· Take care of yourself and the family

· Save for the future

· Plan for big events.

Every investor is unique and has specific financial goals and risk tolerance. Hence, the need for an investment strategy tailored to the individual.

If you are new to investing or are unsure about which investments are right for you, you may want to consider working with a financial advisor. A financial advisor can help you develop an investment strategy that aligns with your financial goals and risk tolerance.

It is important to carefully consider your options and do your research before making any investment decisions. Again, your financial advisor can advise you about the best investment options available to you.

Q5. I have been working with an IT firm for 14 years, earning enough and have also gathered a few assets. My children are in school, but I want to prepare a will for them. Is it too early?

Death is one certainty that no one can predict. Given its unpredictability, having a will in place is essential. Most of us wrongly believe we should think of a will only when we have sufficient assets or when we are ageing. But there is no need to wait for the right time to draft a will.

Essentially, a will is a legal document that specifies how you want your assets to be distributed after you pass away.

If a person dies intestate (without a will), the inheritance is passed on according to the succession laws applicable as per one’s religion. This could be a lengthy process which can create complications and delay the distribution of the assets among legal heirs. A will makes the process smoother and less painful.

Here are a few steps you can take to prepare a will:

Determine your assets: Make a list of all your assets (physical, financial, digital, intangible) including your property, investments, bank accounts, and personal possessions.

Decide the distribution: Consider how you want to divide the assets among those who you want to inherit your assets. You can also specify any donation to a charitable cause or a special bequest.

Choose a guardian for your children: If your children are minors, you will need to appoint a guardian to take care of them when you move on. Choose someone you trust, who shares your values and parenting style.

Update will regularly: It is important to review and update your will periodically to make sure it reflects your current wishes and circumstances.

In your case, apart from the will, it is important to prepare a Letter of Guardianship, a legal declaration that allows you to transfer the children’s guardianship to others in your absence. The letter should spell out the range of duties, authorities, or rights that the guardian can permit until the child is 18.

It is important to register the will. As a certified copy is kept with the registrar, registration provides safety and security in case the original will is misplaced or destroyed.

To sum up, preparing a will can help ensure that your assets are distributed according to your wishes and that your children are cared for after you are gone. It is a good idea to start the process as soon as possible to ensure that your wishes are carried out.

International Money Matters Pvt Ltd is a 20-year-old SEBI registered financial planning-cum-investment advisory boutique. Please click here to find out more.