Q1. I am a first-time investor. I would like to start with mutual funds about which I have some basic knowledge. Any suggestions, please?

Glad to hear that you are starting your investment journey with mutual funds. Mutual funds have proven to be profitable options. So, you are on the right track!

It’s very important to choose your first mutual fund wisely. Here are some of the options best suited to first-time investors:

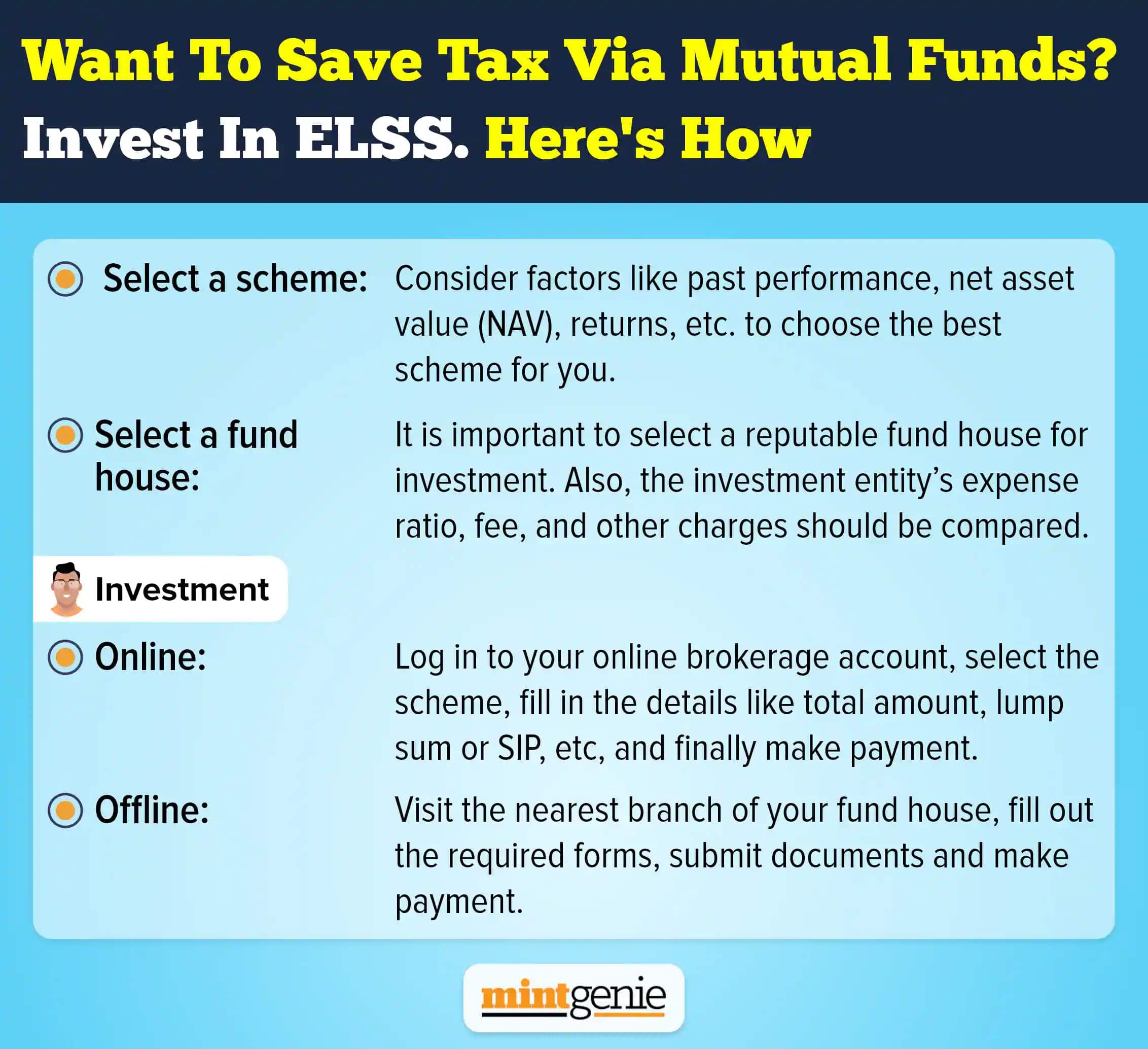

ELSS funds: Equity linked savings schemes (ELSS) allow you to save tax and build long-term wealth. You can invest up to ₹1,50,000 in a financial year and claim it as a deduction under section 80C. Just to keep you informed, the total deduction under section 80C is ₹1,50,000. ELSS is one of the investment options that can be claimed under this section.

If one wants to invest more than ₹1,50,000 (assuming one does not invest in any other investment options eligible under section 80C) then he/she is not allowed to claim any deduction in excess of ₹1,50,000. As these schemes invest in companies of all sizes across sectors you get a portfolio diversified enough to reduce risk. ELSS funds come with a 3-year lock-in period. This benefits first-time investors, as it forces them to remain invested for long.

Large cap index funds: These funds track specific indices (like Sensex, Nifty 50, and Nifty 100) and invest in the top 100 companies in the index they track. An index is a group of securities that measures the performance of a specific market, asset class or market sector. As these funds invest in established companies, the risk is less compared to mid- and small-cap funds that invest in smaller companies.

Dynamic asset allocation funds: These funds invest in both equity and debt. The managers of such funds closely watch market conditions and change the equity and debt balance in response—when the market looks overvalued, they move from equity to debt. Therefore, these funds typically register a lesser drop when the market corrects. This can boost your confidence as a first-time investor.

Short-duration debt funds: These funds lend to the government and companies for 2 to 3 years. These funds are more tax-efficient than fixed deposits, provided you remain invested for at least 3 years.

Enough pointers to start your investment journey? If you would like to dive deeper, it is best to get in touch with a financial advisor who can tell and help you more.

Q2. I want to start planning my investments. Can you share some tips on how to fulfil my New Year resolution?

The New Year is the time for new resolutions. Embarking on a systematic savings or investment journey is the best New year gift you can give yourself. Here are some ways you can make a beginning:

Start recording all your expenses: The first step is to keep track of all your expenses. You may note those down in a diary or use one of the mobile apps. Tracking all expenses will help you to understand how much you are spending on various things like transportation, shopping, groceries, etc. This will also help you estimate how much you can potentially save. Once you reduce expenses, you can increase your savings.

Start an emergency fund: There is no way we can predict an emergency, an unexpected event which you must deal with on priority. Apart from your savings for the future, you must create a separate fund to tackle such emergencies. You can be at peace knowing that should the need ever occur, you are financially prepared to face the emergency.

Invest your money to make it grow: Simply letting your savings lie in a bank account will not let it grow. Inflation (ever increasing prices) will eat away the purchasing power of your money. The best way you can maintain your purchasing power is by investing regularly, possibly in a mutual fund. Once you are ready and confident, you can also explore other avenues of investment.

Develop new sources of income: It is wise to always have two sources of income, your primary job and secondary sources like rental income, fees for giving tuitions, etc. Assess how you can cultivate this second source based on your interests and experience.

Set a savings goal: First decide your goals (maybe you want to buy a motorcycle this year, after you complete your home loan EMI?) and then plan your savings to achieve those goals. Once you are sure of your goal and timeframe within which you would like to achieve it, that will motivate you to save systematically.

Q3. I had to sell my long term equity mutual fund investment at a loss. Is there any tax provision to offset this loss?

If an equity-oriented mutual fund scheme is redeemed within 1 year from the date of investment, any gain/loss from the redemption is considered as short-term capital gain (STCG) or loss (STCL). On the other hand, the gain/loss from redemption after holding the funds for more than 1 year is considered as long-term capital gain (LTCG) or loss (LTCL).

Setting off capital loss: STCL can be set off against both STCG and LTCG. However, LTCL can be set off against LTCG only.

Carrying forward capital loss: Before LTCG from equities and equity-oriented funds were made taxable, the LTCL on such financial assets was treated as dead loss. Such losses could not be set off against LTCG, as the long-term gains from these assets were tax-free. But after LTCG from equities and equity-oriented mutual funds was made taxable in the Union Budget 2018, LTCL can now be set off against such LTCG.

The loss may also be carried forward next year and offset the same with the next year’s LTCG. If still the entire loss is not set off in the 2nd year then the balance can be carried forward to the 3rd year and so on until the eight consecutive financial years, after which it cannot be carried forward any further.

Benefit of setting off: Currently 10% tax is levied on LTCG of more than ₹1 lakh from the redemption of equities and equity-oriented funds in one financial year. Carrying forward of LTCL if not being adjusted in the given year lets the investor reduce the amount of taxable LTCG in the following years until the LTCL is exhausted. However, this carry forward is allowed only if the income tax return is filed in the year during which the investor incurred the capital loss and all the following years.

Q4. I am 42. I am looking for investments with a three-year horizon. Is a debt fund a good option for me?

Yes, debt funds are a good option for you, keeping in mind your three-year horizon.

Most people in your age group and with similar investment horizons tend to prefer fixed deposits (FDs). However, debt funds are more tax efficient than FDs. The interest you earn on FDs is taxed on an accrual basis. This means even if you don’t withdraw it, you must pay tax on the interest earned.

Tax liability on debt funds arises only when you make a withdrawal. If an investment is sold within three years, the gain is added to income and taxed as per the slab. Otherwise, it is taxed at 20% after providing the benefit of indexation. Since the indexation benefit is available only after 3 years, the real benefit of investing in debt funds arises only when they are held for 3 years and more.

If you choose a debt fund, you will save a lot of money at the time of paying tax, especially if you are in the higher tax bracket. You must also consider the benefit of indexation and the possibility of earning higher returns. However, under debt also there are many options and if you would like to get a recommendation on the same then please feel free to reach out to a financial expert to explore different debt funds to match your specific goals.

International Money Matters Pvt Ltd is a SEBI registered investment advisory firm. If you have any personal finance queries, click here to talk to advisors from IMMPL.

Note: This story is for informational purposes. Please speak to a financial advisor for detailed solutions to your questions.