Q. I am a 60-year-old retired civil servant, I have received a significant sum as gratuity. I intend to invest the same and I am considering non-stock market options. I was planning to invest in physical gold, however some of my acquaintances have suggested that I should rather invest in a sovereign gold bonds scheme. I understand that it is backed by the government and is extremely safe. Can you please elaborate on the Sovereign Gold Bond Scheme IV and the procedure to invest in it?

Ravneet Chaddha, Mohali, Punjab

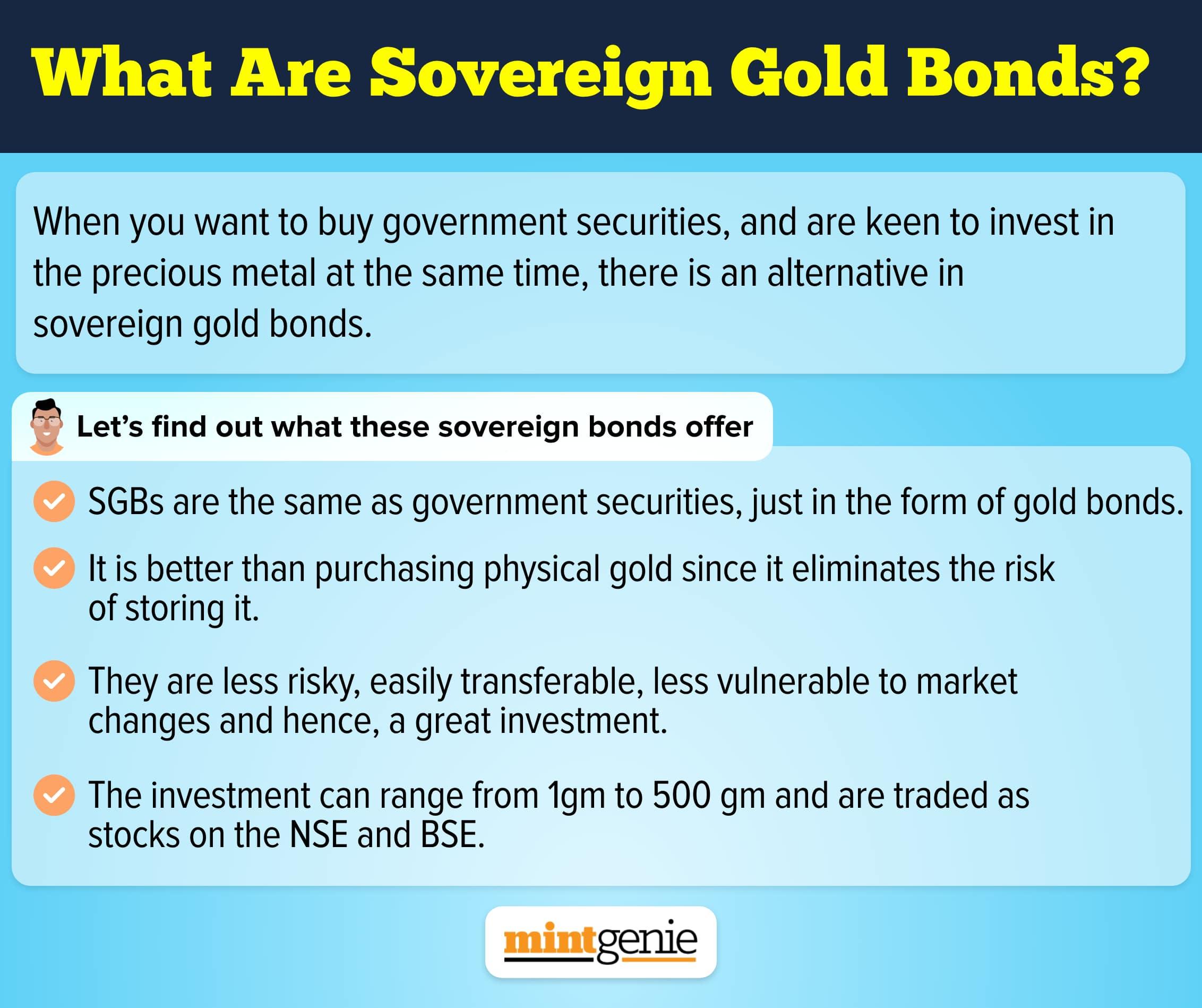

The Indian government introduced the sovereign gold bond scheme in November 2015 with the objective of (a) reducing the demand for physical gold and shift a part of the domestic savings - used for the purchase of gold - into financial savings and (b) to provide an alternative to investing in physical gold with similar benefits and lower risks.

What is a sovereign gold bond?

A Sovereign Gold Bond (SGB) is a government security denominated in grams of gold. It is a substitute for holding physical gold and is issued by the Reserve Bank of India on behalf of the Government of India. Investors have to pay the issue price in cash and the bonds will be redeemed in cash on maturity. SGBs are considered a secure investment option and offer capital appreciation as well as interest every year

The Sovereign Gold Bonds Scheme 2022-23 (Series IV) will be open for subscription from Monday, March 06, 2023 to Friday, March 10, 20231. The issue price of the Bond during the subscription period shall be ₹5,611 (Rupees Five Thousand Six Hundred Eleven) per gram.

The bonds bear interest at the rate of 2.50 per cent (fixed rate) per annum on the amount of initial investment. The minimum permissible investment in Sovereign Gold Bonds is one gram of gold. The maximum permissible investment is 4 kg for individuals, 4 kg for Hindu Undivided Families (HUFs), and 20 kg for trusts and similar entities per fiscal year (April – March).

Taxation

Any capital gain earned from sale of Sovereign Gold Bond is tax exempt. The exemption is only available on redemption after the maturity period of eight years and not on premature redemption or transfer. The capital gains tax exemption on sovereign gold bonds redemption is available under Section 47 (viic) of the Income Tax Act, 1961.

This exemption is only applicable to individual taxpayers and not to other categories like HUF, trusts etc. The interest income on SGB is taxable in India as per the provisions of the Income Tax Act, 1961. You will have to pay tax on the interest income as per your tax slab.

From where can one purchase sovereign gold bonds?

Sovereign Gold Bonds can be purchased from any of the following entities:

- Designated post offices.

- The Stock Holding Corporation of India Limited or SHCIL.

- Recognized stock exchanges of India, such as the National Stock Exchange of India Limited and the Bombay Stock Exchange Limited.

- Scheduled commercial banks

- Investment apps.

Investing in gold vs investing in physical gold

There are several advantages of investing in Sovereign Gold Bonds over physical gold. Some of the benefits include:

Assurance of safety: SGBs are backed by the Government of India, providing a high level of security.

Zero risk of handling physical gold: There is no need to worry about the storage or security of sovereign gold bonds if you purchase them in demat form they will be stored safely and securely in NSDL/CDSL.

Easy exit options: SGBs are tradable on exchanges and can be redeemed once the lock-in period of 5 years is over. Even before the lock-in period is over one can sell their SGBs on a stock exchange.

Assured interest rate: SGBs have a tenure of 8 years with an assured interest rate of 2.5%, disbursed bi-annually.

Cost-effective: There are no making charges (20-30% of jewellery cost) associated with SGBs.

What are some of the disadvantages of investing in SGB?

Here are some disadvantages of investing in Sovereign Gold Bonds:

Long maturity period: The eight-year maturity period may discourage some potential investors.

Only available in tranches: Unlike other investment options, you can’t invest in a primary issue of sovereign gold bonds at any time. You can only invest in the primary issue of SGB when the government opens a new tranche for subscription.

Low liquidity: SGBs may have low liquidity on stock exchanges, and the price may not be reflective of the current price of gold.

Interest rate risk: The interest rate on SGBs is fixed at the time of issuance, and may not be competitive with other fixed income investments if interest rates rise.

Conclusion

Sovereign Gold Bonds is an optimal investment option for those investors who are risk-averse and intend to invest in a safe investment option like gold. There are a number of advantages which SGBs offer over physical gold, enumerated above the biggest being capital gains on SGB being tax exempt.

Kuvera is a free direct mutual fund investing platform.

Note: This is for informational purposes. Please speak to a financial advisor for detailed solutions to your questions.