Indian banks have been in focus on the back of a massive fall in US lenders due to the emergence of a liquidity crisis in the US-based Silicon Valley Bank (SVB). The Nifty Bank index has fallen for 4 straight sessions, down over 5 percent since Thursday (March 9, 2023).

While experts believe Indian banks will continue to decline in the near term due to a knee-jerk reaction to this development, brokerage house Macquarie, in a recent report, noted that they are goldilocks with a minor bump.

According to Macquarie, low credit costs continue to drive multi-year high ROAs (return on assets). Further, EPS (earnings per share) upgrade cycle continues and the brokerage has also raised EPS by 3-9 percent for FY23E-25E. "We increase target prices across most banks as we roll forward to FY25E valuations," it said in the note.

On Thursday, the four biggest USA banks lost nearly $52 billion in market value. The main culprit behind this massive crash in banking stocks was the 60 percent fall in the shares of Silicon Valley Bank (SVB) parent SVB Financial Group. This came after SVB announced the sale of its $21 billion AFS bond portfolio for a big loss of $1.8 billion. The bank further plans to sell $2.3 billion worth of shares to shore up its liquidity, the lender stated in a press release.

The selling of its bonds in losses indicates a major liquidity crisis in the lender, noted experts. This is mainly due to 2 key reasons - high interest rates and declining deposits, noted Samco Securities in a note.

"In simple words, the company depends upon the deposits from technology companies for its liquidity. The tech market has been struggling in the past year, and we all have been hearing about the massive tech layoffs happening across major companies. The weak tech IPO and capital market means tech companies have fewer funds and thus less money to deposit. This resulted in a drag on the company’s liquidity. Further, sighting these liquidity issues the companies are withdrawing their deposits from the bank to safeguard their funds causing more pain," explained Samco.

Let's understand why Macquarie is bullish on Indian banks:

ROAs to remain at multi-year highs: The brokerage believes the goldilocks scenario for private sector banks in India will continue for the next 2 years due to strong asset-quality outcomes. According to Macquarie, the risk arising from a large conglomerate’s exposure is easily manageable as banks carry prudential buffers. It expects ROAs to remain at multi-year highs despite margin compression due to offsets coming from lower treasury losses, better operating leverage, and benign credit costs. PSU banks, on the contrary, have seen their ROAs peaking, and the brokerage sees their ROAs to come off by 15-20bps over the next 2 years due to some normalisation of credit costs and higher expense ratios.

Earnings estimates: Despite concerns of a slowdown in loan growth and margin compression, the earnings upgrade cycle continues for the banking sector, noted the brokerage. It has raised earnings by 3-9 percent for FY23E-25E for private sector banks on better margins and lower credit costs. "Our EPS estimates are more or less in line with consensus estimates for private sector banks. However, for PSU banks, we are 11-13 percent below consensus on account of higher credit costs that we assume," noted Macquarie. Meanwhile, it expects core PPoP growth to be around 16-18 percent for HDFC Bank and IndusInd Bank vs 12 percent for all banks. “They are our top picks in the sector,” said the brokerage.

As per the brokerage, over the past 12 months, banks have continued to see earnings upgrades. Across the board, banks have seen earnings upgrades due to two key aspects: better performance on margins and better performance on asset quality, amid sustained low credit costs, it explained. This is in sharp contrast to most other sectors, which have witnessed earnings downgrades over the past 6 months, it pointed out.

Loan growth to slow down and margins to fall but remain at healthy levels: The brokerage noted that in the last rising rate cycle when rates went up +350 bps, margins for banks went up 50 bps over a period of 3 years, as loans also repriced with a lag and banks were on an opaque base/PLR rate system of repricing of loans. With the more transparent and immediate loan repricing system driven by repo-rate linked loans, bank margins have gone up 50-60 bps in a single year, it said. With deposit repricing catching up with a lag, it expects around 15-20 bps compression in NIMs (net interest margins) for banks in FY24E. It believes loan growth is likely to slow down from a system level of 16-17 percent currently to 13-14 percent driven by lower working capital demand and a general economic slowdown.

Credit costs – the big support to ROA: While margins may compress, there are offsets in the form of lower treasury losses, lower cost ratios and continued low credit costs, which will support ROA, as per Macquarie. "Banks in India carry an excess provisioning buffer of 30-100bps, which acts as a cushion for FY24E earnings/ROA. We are also not worried about exposure to a particular large conglomerate group, as exposure levels are small. Banks have sufficient buffers to manage the stress, in our view," said the brokerage.

Overall ROA and ROE (return on equity) levels to remain high: In FY23E, banks in India reported the highest levels of ROA seen in the past decade, and Macquarie expects that to continue. It believes rising leverage will keep ROEs in the 15-18 percent range, implying that book value will continue to compound at those levels. Even if one argues for no rerating from the current levels, banks remain strong ‘power of compounding’ stories with a high degree of earnings visibility, noted the brokerage.

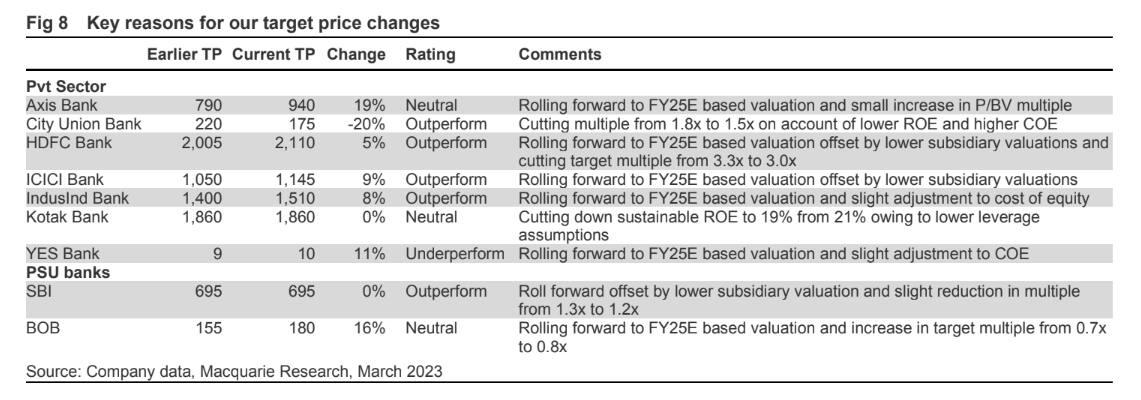

Target prices: The brokerage also increased target prices across most banks mainly on account of rolling forward to FY25E-based valuation. “In some specific cases there has been a cut in TP or lower than expected increase in TP as we have altered target P/BV multiples wherever required,” it noted.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.