PSU banks have been in focus on the back of their stellar quarterly results on nearly all fronts - a healthy increase in margins, healthy loan growth, and continued benign asset quality trends. The banks' earnings are indicative of a favorable operating environment, which is the best in the last decade, noted market experts. Despite this, the banking stocks trade well below their decade's peaks.

Bank of Baroda vs Punjab National Bank: Which is a better long-term investment?

TL;DR.

On the back of strong earnings but a fall in stock prices, PSU banks have been in focus. But from a long-term perspective, let's find out which is a better PSU bank between Bank of Baroda (BoB) and Punjab National Bank (PNB).

All PSU bank stocks have given negative returns in 2023 so far. The Nifty PSU Bank index is down 13 percent in 2023 YTD after rallying over 40 percent in the last 1 year.

On the back of strong earnings but a fall in stock prices, PSU banks have been in focus. But from a long-term perspective, let's find out which is a better PSU bank between Bank of Baroda (BoB) and Punjab National Bank (PNB).

Stock Price Trend

While both these banks outperformed benchmarks in the last 1 year, they have been in the red YTD.

In the last 1 year, BoB surged 57 percent whereas PNB rose 39 percent. However, in 2023 YTD, Both BoB and PNB have lost around 13 percent each.

In the last 1 month, BoB rose around 5 percent while PNB shed a little over 3 percent.

BoB shed 5.3 percent in February after a 9.6 percent decline in January 2023. However, before falling in Jan, it had given positive returns in 6 consecutive months between July and December 2022, rising 90 percent in this period.

Similarly, PNB lost nearly 10 percent in February after a 5 percent fall in January 2023. Before declining in Jan, it had also given positive returns in 6 straight months between July and December 2022, jumping nearly 95 percent in this time.

Bank of Baroda hit its 52-week high of ₹197 on December 12, 2022, and a 52-week low of ₹89.9 on June 20, 2022. PNB, on the other hand, touched its 52-week high of ₹62 on December 15, 2022, and a 52-week low of ₹28 on June 20, 2022.

Meanwhile, from a long-term perspective, BoB has given multi-bagger returns, up 127 percent in the last 3 years whereas PNB is up just 15 percent.

Bank of Baroda Stock price trend

About the firms

Bank of Baroda is a public sector enterprise that provides banking and financial services in India. It offers personal banking services, which include savings accounts, current accounts, and term deposits. It also provides a range of digital products like mobile banking, cards, etc. Among loans, it offers home loans, personal loans, vehicle loans, fintech, education loans, and gold loans. It has 8,185 branches and 11,535 ATMs and cash recyclers supported by self-service channels.

Punjab National Bank also provides various banking and financial products and services in India. The company operates through Treasury, Corporate/Wholesale Banking, Retail Banking, and Other Banking Operations segments. It offers personal banking products and services, schemes for micro, small, and medium enterprises, agricultural banking services, corporate banking products, etc. In addition, it also offers insurance, depository, mutual fund, and merchant banking services. It operates a network of branches in India; and branches in Hong Kong and Dubai, as well as representative offices in Bangladesh and Myanmar. The company was founded in 1895 and is headquartered in New Delhi, India.

Earnings

In the December quarter (Q3FY23), Bank of Baroda reported its highest-ever quarterly net profit of ₹3,853 crore, up 75 percent compared to a net profit of ₹2,197 crore in the same quarter last year. Sequentially, the net profit was up by 16.29 percent.

Its net interest income rose 26.5 percent to ₹10,818 crore for the three months ended December. This comes on the back of a robust loan growth of 19.7 percent and an improvement in net interest margins as well. Meanwhile, provisions declined 4 percent to ₹2,403.93 crore for the quarter ended December 31, 2022. In the same period of the previous year, the bank's provisions totaled ₹2,507 crore.

Together with healthy NII growth and modest provisions, the bank's operating profit surged 50 percent year-on-year to ₹8,232.19 crore from ₹5,483.33 crore a year ago. Its NIM also improved to 3.37 percent for the December quarter, 24 basis points higher than that in the corresponding quarter of the previous year. Its asset quality metrics showed further improvement, with the share of bad loans in the overall loan book falling. The gross bad loan ratio dropped to 4.53 percent in the December quarter, from 7.25 percent a year ago.

On the other hand, Punjab National Bank's net profit fell 44 percent to ₹629 crore in the quarter ended December 2022. The net profit stood at ₹1,127 crore in the same period last year.

Its NIIs rose 18 percent to ₹9,179 crore during the third quarter versus ₹7,803 crore in the same quarter last year. Meanwhile, the asset quality of the lender improved substantially during the quarter. Gross non-performing assets declined to 9.76 percent as against 12.88 percent a year ago. Net NPAs, too, dropped to 3.30 percent from 4.90 percent last year.

However, the lender's provisions increased 40 percent to ₹4,713 during the third quarter against ₹3,353 crore in the corresponding quarter of last year. Its total income rose 17 percent to ₹25,722 crore for the quarter under review. It was ₹22,026 crore in the last year's quarter. Meanwhile, operating margins in the said period declined to 22.22 percent against 23.05 percent in the corresponding quarter of last year.

PNB stock price trend

Which is a better long-term investment?

Ajit Kabi, Banking analyst at LKP Securities, has picked Bank of Baroda over PNB.

"Both Bank of Baroda and Punjab National Bank are witnessing improvement in fundamentals. The legacy bad loan cleanup is at the tail-end. However, Bank of Baroda has reported stellar results in the previous few quarters. The profitability of the bank soared further with lower credit cost and the inexpensive valuation may propel the stock further," he said.

Vinit Bolinjkar- Head of Research - Ventura Securities, also likes Bank of Baroda.

Bolinjkar noted that in Q3, Bank of Baroda (BoB) saw another strong quarter with core PPoP at ₹7300 crore led by higher NII, and lower opex while asset quality improved. Bank indicated that increasing retail share, expanding corporate yields and higher MCLR share (50 percent) could drive further NIM expansion, he added. Bank of Baroda has reported a continued improvement in business growth as well as asset quality, which is expected to aid return ratios and, thus, valuations, highlighted the expert.

Meanwhile, for Punjab National Bank, he noted, "The bank is on the mend with better visibility on stress reduction. Issues are being addressed in the RAM segment, which is the major contributor to stress, by tighter underwriting. To avoid further asset quality lapses, most underwriting is now done centrally and branches would only mobilize proposals."

Meanwhile, another analyst, who did not wish to be named also told MintGenie that he prefers Bank of Baroda.

"Both the banks are expected to outperform driven by improvement in core ROA trajectory in near to medium term, riding on the strong tailwinds. In terms of operating metrics and growth outlook, BOB continues to outperform PNB. The downside appears to be very limited in both stocks after recent underperformance in the last 2 months. However, from a long-term perspective, BOB is placed better," he said.

Brokerage house Motilal Oswal has a ‘buy’ call on Bank of Baroda but a ‘neutral’ call on PNB.

"With healthy NII growth and ‘other income’ driving earnings, BOB reported a strong quarter. Margins witnessed an expansion to 3.4 percent. Business growth was healthy at 6.5 percent QoQ, aided by strong traction across segments. Asset quality continues to improve with NNPA at less than 1 percent. A lower SMA book and controlled restructuring provide further comfort on asset quality. We increase our earnings estimate sharply by 21 percent for FY23 and 13-14 percent for FY24/25, factoring in higher NII and other income. We estimate FY25 RoA/ RoE of 1.1 percent/15.3 percent, respectively, and value the stock at ₹240 (1.1x Sep’24E ABV)," it said.

For PNB, the brokerage noted that it reported a weak quarter with high opex and elevated provisions, denting earnings. NII growth, however, came in healthy with margins expanding 19bp QoQ. The brokerage cut its earnings sharply by 39 percent for FY23, factoring in higher opex and provisions, while broadly maintaining our estimates for FY24/25 and projects RoA/RoE of 0.6 percent/8.2 percent, respectively, by FY25E. It reiterates a Neutral rating on the stock with a TP of ₹50.

Outlook

Kabi of LKP noted that the stock price performance of PSU banks has been tepid since the calendar year 2023 started. The price-performance was well anticipated factoring higher interest rate scenario, he said.

However, the increase in deposit rates is likely to squeeze the margins after a peak formed in Q3FY23, he cautioned, adding that the credit growth is likely to slow down in the coming quarters, which was in the higher teens in the previous few quarters. He expects a credit growth of 200bps higher than nominal GDP growth. Additionally, new ECL norms may raise credit loss and hence impact profitability. However, the negatives are priced in, he added.

Meanwhile, Bolinjkar of Ventura believes that weak global demand and monetary tightening by the central bank have impacted the economic growth outlook for PSU banks in the near term. With a recovery in growth and stable asset quality, PSU banks are set for a further re-rating, he forecasted.

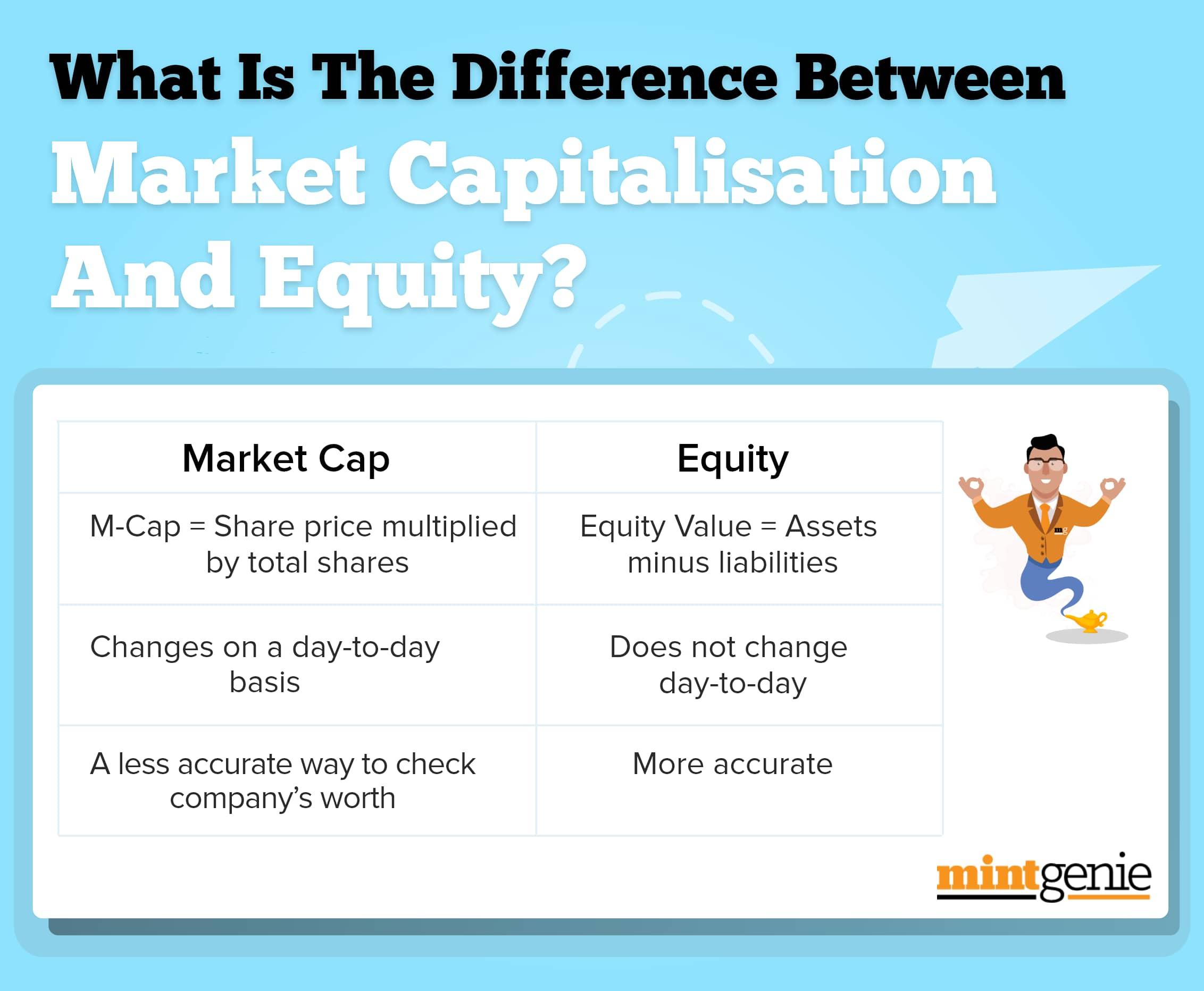

Market cap vs equity

First Published: 01 Mar 2023, 01:15 PM IST

Related Stories

Explain Like I am 5

personal finance

Equity vs real estate: Which will yield better returns in the long term?

Team MintGenie