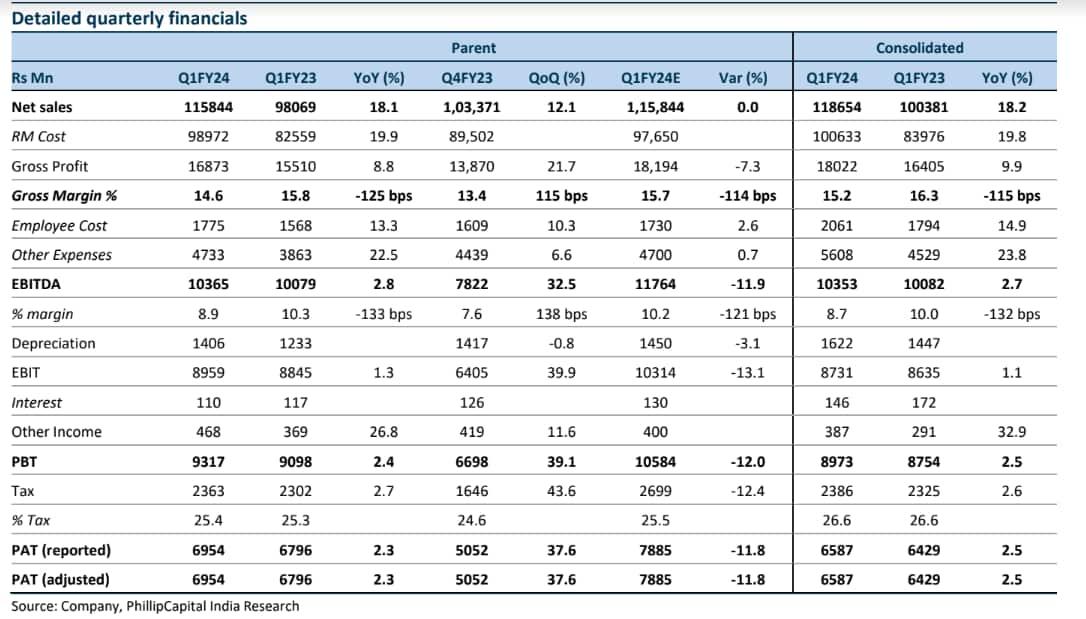

Avenue Supermarts (DMart) reported just a 2.3 percent year-on-year (YoY) rise in net profit for the quarter ended June to ₹695.36 crore, versus ₹680 crore in the year-ago period.

DMart disappoints in Q1! Should you still buy the stock?

TL;DR.

Brokerages remain mixed on DMart post the June quarter earnings. While some retained ‘buy’ calls on the back of long-term growth opportunities, others have ‘neutral’ or ‘sell’ calls on the stock due to weak margins in Q1.

However, sequentially, its net profit rose 43 percent from ₹460.10 crore in the previous quarter.

Meanwhile, it reported an 18 percent YoY growth in revenue for the quarter under review at ₹11,584.40 crore versus ₹10,038.07 crore a year ago. Sequentially, the revenue was up 12 percent from ₹10,594.11 crore in the previous quarter.

"Overall gross margins are lower compared to the same period in the previous year, primarily due to lower sales contribution of apparel and general merchandise," said Neville Noronha, CEO & Managing Director, Avenue Supermarts Limited.

Stock Price Trend

Shares of Avenue Supermarts fell almost 4 percent on Monday to its intraday low of ₹3,694 on the back of weak June quarter earnings.

The stock has fallen 2 percent in the last 1 year and over 5 percent in 2023 YTD, giving negative returns in 5 of the 7 months in the current calendar year so far. The stock has lost 3.5 percent in July so far after a 12 percent jump in June.

It gave negative returns in May, March, Feb and Jan but was positive only in April and June.

DMart stock price trend

Brokerage views

Brokerages remain mixed on the stock post the June quarter earnings. While some retained ‘buy’ calls on the back of long-term growth opportunities, others have ‘neutral’ or ‘sell’ calls on the stock due to weak margins in Q1.

Prabhudas Lilladher: The brokerage has a ‘buy’ call on the stock but cut its target price to ₹4,587 ( ₹4,651 earlier), indicating an upside of 19 percent from its current market price of ₹3,840 (as on July 14).

Post the June quarter earnings, the brokerage cut EPS (earnings per share) estimates of DMart by 3 percent and 1.5 percent for FY24E and FY25, respectively, and target price following disappointing margin performance led by 1) deterioration in sales mix given lower sales in general merchandise and apparel and 2) structural competitive pressures from mass market apparel players (Zudio, Reliance Trends).

It noted that D’Mart needs to restructure its apparel business given the new threat perception, which will take a few quarters for turnaround. However, it added that D’Mart Ready is on a fine footing with highly competitive consumer pricing and an increase in delivery charges by competitors due to huge losses.

"We believe D’Mart has a huge runway to grow with 1500+ store potential and scale up in D’Mart Ready. We expect growth pressures to sustain in 2Q also before recovery in 2H24. D’Mart lacks near triggers, although the stock remains a long-term Buy," it explained.

JM Financial: The brokerage also retained its ‘buy’ call on the stock with a target price of ₹4,255, indicating an upside of 10.6 percent from its CMP. The brokerage noted that DMart’s Jun-Q report was not too different from those seen in recent quarters.

“Growth in sales per store, though a tad better vs the last few quarters, is still not good enough given the business’s true potential, in our view. Discretionary sales remained an issue and continued to impact both throughput (and, therefore, operating leverage) and also gross margin. Management commentaries, interestingly, point to a silver lining in this regard. As per the company, “general merchandise contribution is recovering and trending towards pre-pandemic levels”; the apparel category still seems to need some work. A recovery in this part of the portfolio would help gross margin and also bring scale efficiencies back into the business,” it said.

"We continue to like DMart - businesses with such long growth runways are rare and we recommend investors to not get too carried away by short-term weakness(es)," added the brokerage.

Motilal Oswal: The brokerage has retained a ‘buy’ call on the stock with a target price of 4,420, implying a 15 percent upside. DMart clocked 19 percent revenue CAGR over FY20-23 led by 20 percent footprint additions, said MOSL. It further noted that the subdued same-store sales growth (SSSG) was mainly due to: 1) the additions of bigger stores over the last couple of years, and 2) weak discretionary demand.

However, despite its weak SSSG, DMart has managed to protect its EBITDA margin at pre-Covid levels, through its strong cost-control measures unlike most other retailers, added MOSL. It believes that SSSG is set to recover in FY24, due to: 1) easing general inflation along with RM cost reduction that may help in reviving discretionary demand; and 2) the company’s strategy to open larger stores as the smaller ones are likely to report a growth plateau after almost three years (with their SSSG peaking out). Those larger stores are now in the base and will start contributing to store productivity, with further room to grow their footfalls.

The brokerage has largely maintained estimates, factoring in a revenue/PAT CAGR of 26 percent/27 percent over FY23-25 aided by 16 percent/9 percent growth in footprints/revenue productivity.

Phillip Capital: The brokerage reiterated its ‘neutral’ call on the stock with a target price of ₹3,830, indicating no upside.

The brokerage has revised its revenue and EBITDA estimates downward for FY24/FY25 by 1.7 percent/0.8 percent and 4.1 percent/1.0 percent respectively due to disappointment in gross margin led by slow recovery in general merchandise.

"Inflation in food staples continues to impact discretionary spends for consumers, especially in the mass segment. This has led to a drag in the category sales mix for the company as FMCG and food continue to outperform general merchandise and apparel sales. However, the management guides that general merchandise contribution is recovering and trending towards pre-pandemic levels. We expect near-term pain to persist and gross margin to remain under pressure on the back of unfavourable sales mix," said the brokerage.

Nuvama: The brokerage also has a ‘hold’ call on the stock with a target price of ₹4,015, indicating an upside of just 4.5 percent.

"Avenue Supermarts (DMart) reported a muted showing with Q1FY24 EBITDA/PAT coming in 11 percent below our estimate (10 percent/7 percent to consensus). This was again driven by a weak GM. Management did make a statement that the mix is improving and trending towards the pre-pandemic level, but this quarter’s performance is not an improvement over last. Hence, this remains a concern while we await further clarity," it said.

Factoring in a lower gross margin and miss on Q1FY24, the brokerage reduced its FY24E PAT estimates by 3 percent.

Kotak Institutional Equities: The brokerage has a ‘sell’ call with a target price of ₹3,475, indicating a downside of almost 10 percent.

The brokerage revised FY24-26 revenue estimates downwards by 1-4 percent resulting in an EPS cut of 2-6 percent. “Roll-forward coupled with lower capex estimates drives an unchanged FV of ₹3,475. We retain a cautious stance on the stock with SELL,” it said.

Source: Phillip Capital

First Published: 17 Jul 2023, 01:58 PM IST

Related Stories

Explain Like I am 5

markets

What are the investing mistakes retail investors make and how to avoid them?

Manik Kumar Malakar