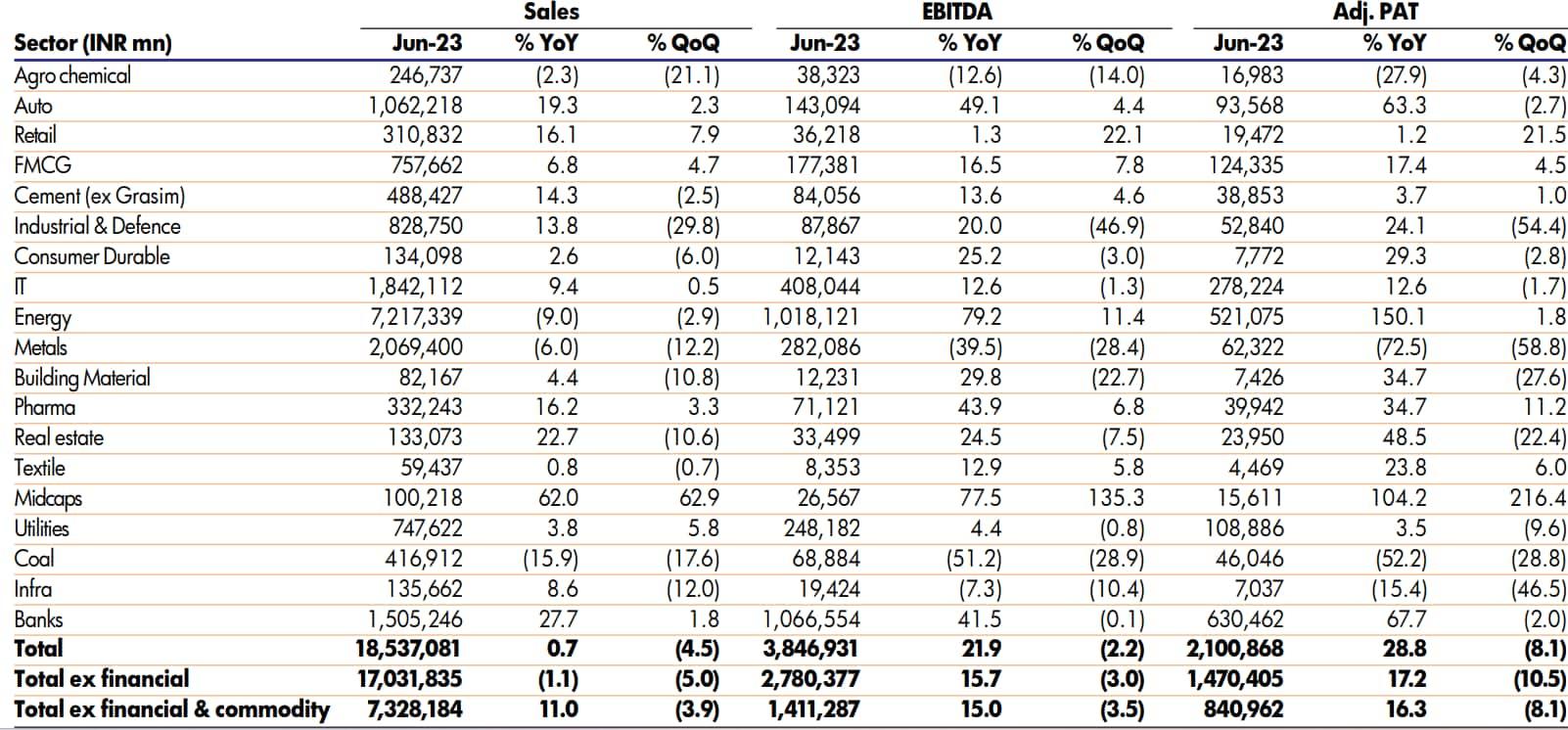

According to brokerage firm Antique Stock Broking, Nifty50 companies (excluding financial, telecom, & commodity) are expected to report revenue, EBITDA, and PAT growth of 8%, 13%, and 23% YoY in 1QFY24. The brokerage has pointed out that macroeconomic factors such as the moderation in inflationary pressures, including a decline in metal and crude oil prices, are expected to contribute to margin improvement.

With metal and crude oil down 17% and 30% YoY, respectively, margins are anticipated to improve by approximately 80 bps YoY, primarily benefiting sectors such as FMCG, auto, and healthcare, it noted.

The broader macroeconomic indicators suggest a positive trend in corporate earnings, driven by the Reserve Bank of India's estimate of real GDP growth of 8.0% YoY in 1QFY24.

Among sectors, the brokerage expects strong operating profit growth in banks, energy, auto, and healthcare. Conversely, coal, metal, agrochemicals, infra, retail, cement, and utilities are likely to be laggards.

Sector-wise Projections:

Note: The below earnings projections are for the companies under the brokerage coverage universe.

Banks: Q1 FY24 is expected to be another strong quarter for the banking sector, helped by the base impact. Banks are likely to report strong earnings growth of 68% YoY, driven by 131% YoY growth by PSU banks, supported by loan growth of approximately 17%–18%, a 40-bps improvement in NIMs, and low credit costs, said Antique Stock Broking.

Energy: The overall energy sector, according to the brokerage, is expected to report a strong quarter, primarily due to the performance of oil marketing companies, which benefit from high retail petrol/diesel margins and moderate GRMs.

However, the performance of other segments within the energy sector is likely to be mixed, it said, with factors such as lower APM prices impacting the upstream segment, normalisation for gas utilities, and varying performance for city gas distribution companies.

Autos: The brokerage expects auto companies to report strong earnings growth of over 60% YoY, driven by healthy revenue growth of approximately 19%. Factors contributing to this growth, as per the brokerage, include price hikes, volume growth from a strong order book and new product launches, and a YoY margin improvement due to the easing of commodity prices.

FMCG: FMCG companies are expected to deliver strong sales, EBITDA, and PAT growth of 7%, 16%, and 17% YoY, respectively. The brokerage said that the sales growth is shifting from pricing-driven to volume-driven, with rural markets experiencing an upswing while urban markets remain steady. Margins are anticipated to improve due to a decline in commodity prices.

Pharma: The pharmaceutical sector, according to the brokerage, is expected to witness strong earnings growth, with a projected 35% YoY increase and 11% QoQ.

This growth is attributed to 16% YoY revenue growth, primarily due to a low base in US generics, and a significant YoY margin improvement of around 400% resulting from a better product mix and lower raw material and freight costs, it said.

Metals: On the other hand, metal companies are likely to report a weak quarter, with an expected EBITDA de-growth of 40% YoY and 29% QoQ. Softened non-ferrous metal prices due to recession fears and narrow steel spreads resulting from lower realisation and higher input costs are likely to impact metal companies, the brokerage noted.

Utilities: Within the utilities sector, Coal India and Tata Power are anticipated to experience sharp earnings decline due to the steep correction in coal prices. In contrast, NTPC and Power Grid are expected to report moderate growth in earnings, supported by modest growth in regulated equity.

Fashion Retailers: Earnings for fashion retailers are likely to be impacted by demand moderation due to subdued consumer sentiment and margin pressure from end-of-season sales (EOSS). A marginal 1% YoY earnings growth is expected in this sector, said the brokerage firm.

Based on forecasts, the brokerage estimated a target of 20,500 for the Nifty 50 index by March 2024, using a 19x multiple of the FY25 earnings per share of 1,061.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.