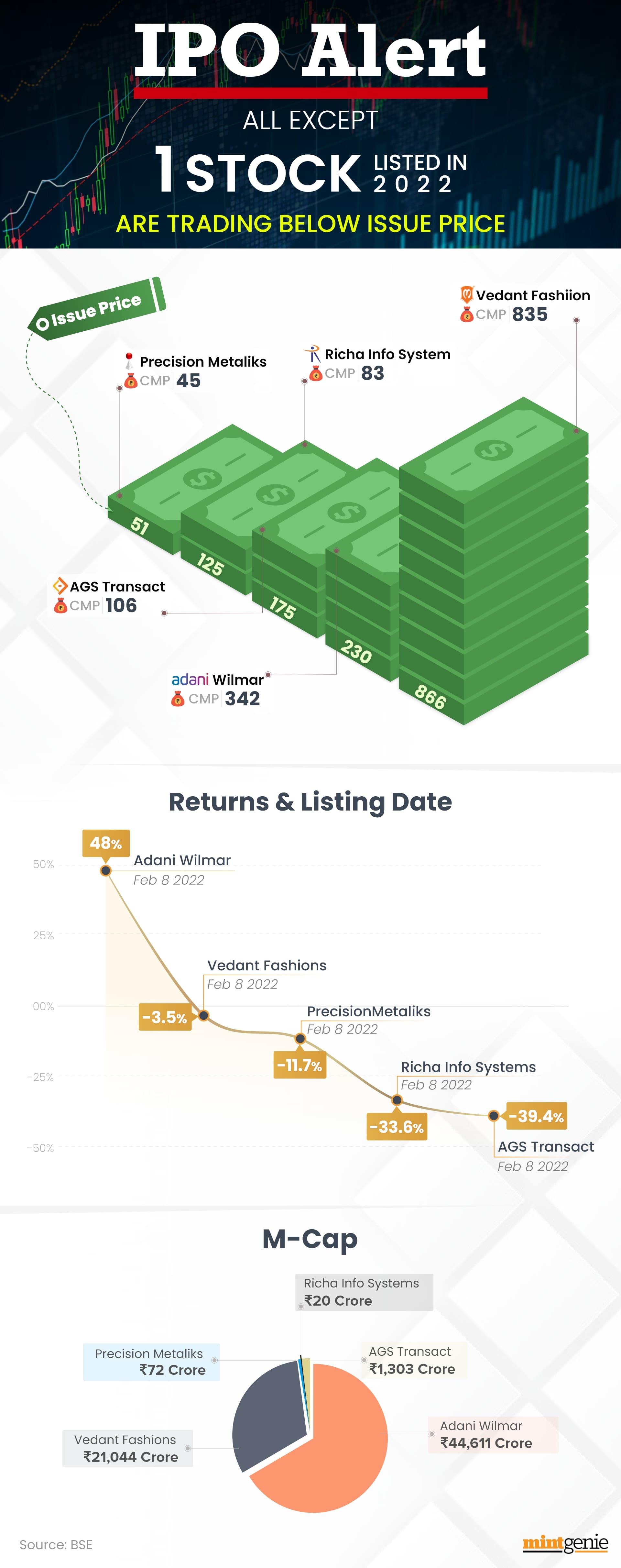

After falling around 23 percent from its listing price, global brokerage house Jefferies has now initiated coverage on FSN E-Commerce Ventures (Nykaa) with a 'buy' call and a base target price of ₹1,650.

In a bull case scenario, the brokerage expects Nykaa to jump to ₹2,300, implying a 48 percent upside. However, in a bear case scenario, the target price by Jefferies is ₹900, indicating a downside of 42 percent.

After listing at ₹2,018, a nearly 80 percent premium to its issue price ( ₹1,125), Nykaa has fallen as much as 40 percent to hit its record low of ₹1,219 on February 22, 2022. However, since then, the stock has seen steady gains, rising around 27 percent to around ₹1,550 currently.

Founded in 2012 by former investment banker Falguni Nayar, FSN E-Commerce Ventures Ltd is an online marketplace for beauty and wellness products. It has its own manufactured brand products under its two business verticals - Nykaa and Nykaa Fashion. The stock made its market debut in November 2021.

The stock lost over 20 percent each in January as well as February of the current calendar year 2022 but has gained 17 percent in March so far.

As per Jefferies, India's Internet opportunity is attracting players across categories and growth is mostly at the cost of profitability.

"Nykaa enjoys a leadership position in the online beauty space, and its positive EBITDA margin is a key differentiation. Product assortment, discovery & authenticity drive high repeats and the content ecosystem is engaging. Fashion is growing rapidly but the right to win is yet to be proven," it said in the note.

It added that the platform has been able to carve out a niche in beauty and personal care (BPC) products, which differentiates it from horizontals like Flipkart/Amazon.

The brokerage further pointed out that consumer stocks in India enjoy a significant premium given the growth runway and this should likely continue for Nykaa.

However, competition in the core beauty and personal care category, late entry into fashion and pull-back in tech valuations are key risks for the stock.

In the base case scenario, the brokerage build-in strong over 25 percent CAGR order growth for Nykaa (beauty and personal care category) over FY22-26E, which will be led by new customer additions. Order frequency is also expected to see a gradual growth as customer cohorts mature.

Meanwhile, in the bull case scenario, Jefferies build-in a very strong ~30 percent CAGR order growth for Nykaa BPC over FY22-26E. Order frequency is lso expected to see a gradual growth as customer cohorts mature while BPC gross merchandise value (GMV) is expected to grow strong at 30 percent CAGR over FY22-26E.

Now, in the bear case scenario, Jefferies build-in 20 percent CAGR order growth for Nykaa BPC over FY22-26E. Order frequency is estimated to

stay flat in the medium term on account of the potential dilution from new customers. BPC GMV is expected to grow strong at 20 percent CAGR over FY22-26E.

"Nykaa has been able to carve out a niche for itself through its focus on BPC. The recent years have seen a surge in transacting customers for the

Company. Nykaa should benefit from the increasing order frequencies and basket values, as the newer customer cohorts mature. We expect Nykaa to remain in a hyper-growth phase in the medium-term as the online BPC and fashion penetration ramps up," highlighted the brokerage.

For the December quarter, Nykaa also reported a weak set of numbers. Its net profit fell 59 percent YoY to ₹29 crore, hit by a jump in expenses and subdued demand for personal care and fashion products. Revenue from operations of the company grew 36 percent YoY at ₹1,098 crore.

11 analysts polled by Mintgenie also have a ‘buy’ call on the stock.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.