Domestic brokerage house Edelweiss Securities has cut target multiples of all IT stocks in its coverage post the below estimated June quarter earnings.

"While we remain confident of our estimates on both growth and margins but with interest rate going up, the discounted cash flow (DCF) value of the companies go down, implying a discount on implied multiples, even if the earnings remain the same," noted the brokerage.

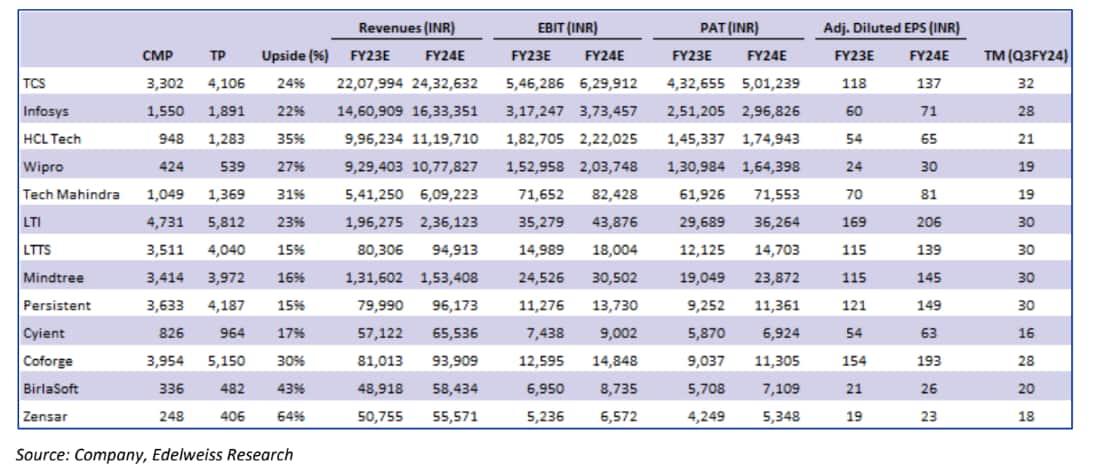

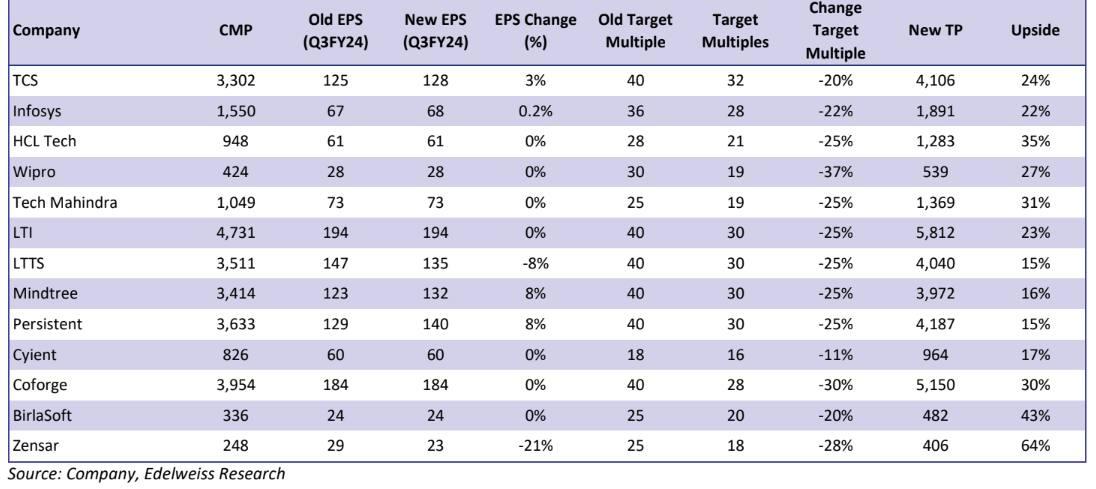

Edelweiss has cut its target multiples by 11-37 percent for the IT stocks in its coverage and posted that the new upsides estimated in the stocks are between 15-64 percent. It has also revised earnings estimates for all these stocks under review.

A plausible US recession, sporadic instances of guidance cut by US tech majors, rate hikes and severe talent crunch – is an ensemble that has managed to breed a sense of fear for IT scrips, explained the brokerage.

Nifty IT Performance

Amid this backdrop, the Nifty IT Index has also corrected sharply, around 25 percent in 2022 so far as against a 1 percent decline in the Nifty Index. While historical data suggests a strong correlation between IT exports and US GDP growth rates, the current forecasts from economists and margin pressures (attrition) have been feeding the fear, noted Edelweiss.

In 2022 so far, all Nifty IT constituents have also given negative returns. Wipro has tanked the most, 40 percent followed by Tech Mahindra, down 39 percent and Coforge, down 35 percent. Meanwhile, HCL Tech, L&T Infotech, MindTree, and Mphasis has also shed between 23-35 percent each. TCS has lost around 10 percent and Infosys has fallen 15 percent in this period.

The brokerage has cut the target price for Wipro the most, down 37 percent to ₹539. Post this cut, the current upside seen in the stock is 27 percent. The second largest target cut was seen in Coforge to ₹5,150. Post this, the upside seen is 30 percent. It also has cut target multiples for TCS, Infosys, HCL Tech, Tech Mahindra, L&T Tech, L&T Infotech, MindTree, Persistent Systems, Birlasoft and Zensar Tech by over 20 percent each. Cyient is the only stock in its coverage with an 11 percent target cut.

The brokerage has changed estimates for TCS (FY24E by 3.8 percent), Infosys (FY24E by 0.7 percent), L&T Tech (FY23E/24E by -6.9 percent/-11.2 percent), Mindtree (FY23E/24E by 3.2 percent/5.2 percent), Persistent (FY23E/24E by 5.7 percent/7.6 percent) and Zensar (FY23E/24E by -27.1 percent/-20.6 percent).

Estimate Cuts

The brokerage said that it has cut the estimates for L&T Tech and Zensar where supply-side pressure has overridden our expectations. Persistent rate hikes had impacted our implied multiples which compelled the brokerage to revise its multiples lower by 11-37 percent across the board, implying a similar cut in target prices. Nonetheless, it added that it remains confident of demand and profitability going ahead.

Post the target cuts and changes in estimates, the brokerage prefers HCL, TechM and Infosys among the large-caps and Coforge, L&T -Mindtree and Persistent in mid-small caps.

"We have cut our multiples with a delay, basis our confidence on growth and earnings estimates and while assigning little value to the rate hike impact on the implied multiples. Our delay was on the back of the strong tech upcycle (which continues), price hikes (post a decade) and work-from-home savings. Our implied multiples are impacted due to sharp move in interest rates," it said.

It further noted that Street’s revenue estimates for FY23E/24E have been cut by an average of 3.3 percent/3.2 percent, which is in stark contrast to FY21/FY22 where the estimates increased multiple times over the course of the year as IT services companies continued to surprise on growth and margins.

It believes current estimates build in excessive pessimism led by past strong correlation versus economic cycle thereby completely ignoring the technology cycles.

The Future

"Currently, Street is building both growth slowdown and supply-side pressure, which we believe is an unlikely equation on a sustainable basis. The current scenario will reverse and lead to much higher earnings growth than anticipated by consensus," predicts Edelweiss.

It further noted that data suggests that while economic cycles do have a strong correlation with tech- spending, a stronger co-relation exists between tech spending and the technology cycle.

"We believe, the prevailing technology cycle is buoyant riding on a cloud, the building of omnichannel capabilities by enterprises and pent-up demand substantiated by impressive order-books. Moreover, the pent-up demand in sectors like travel and manufacturing will be additional triggers," it added.

It is confident that while the economic cycle is against us, the technology cycle is hugely buoyant. Moreover, previous drivers like efficiency/cost saving are now bolstered by digital being a revenue and profit enabler. These additional drivers have led to expeditious digital adoptions by global enterprises to defend revenue market share, it pointed out.

Key risks to profitability going ahead include 1) Substantial cut in US technology budgets, particularly in digital, 2) Adverse regulatory provisions, 3) Serious data breach in the global technology ecosystem (FAANGS), 4) Sharp depreciation of USD vis-à-vis INR and other currencies and 5) Visa restrictions, cautioned Edelweiss.

"We believe attrition has peaked, which will lead to improvement in margin going forward. We are confident in our estimates and believe that street is building too much pessimism," it said.

It further highlighted that just like global tech majors, pessimism has spilled over onto Indian IT services companies, which is unwarranted as their valuations carry even more conviction now. With this, it believes, the Indian tech industry is marching into its best phase – in fact, it has witnessed price hikes being taken almost after a decade.