With the RBI pausing rates for the second straight time in the June meeting and investors now hoping for a rate cut in the near future, global brokerage house CLSA cautioned that while investors are excited over prospects of rate cuts translating into lower cost of funds for NBFCs, the reality is not so sweet.

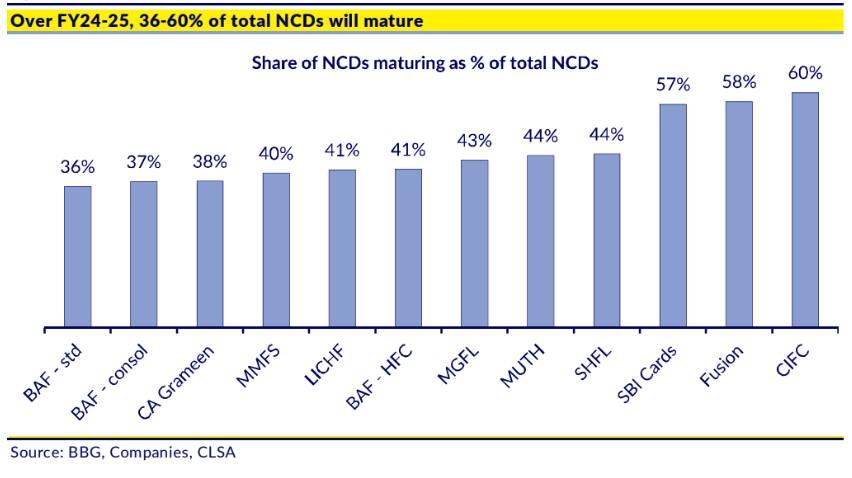

In a recent note, the brokerage informed that less than 50 percent of borrowings for most large NBFCs are at floating rates, the transmission of which happens with a lag of 1-12 months. It further pointed out that 20 percent of NBFCs’ non-convertible debentures (NCDs) are maturing in FY24 in FY25 each – these NCDs bear coupon rates much below current levels, implying a refinancing hit.

Also, the incremental cost of NCDs is unlikely to come off with repo rate cuts, as bond yields are already factoring in repo rate cuts, CLSA added.

So who will be the winners and losers in a rate-cut cycle?

As per the brokerage, the winner, looking at the cost of funds, in a rate-cut environment would be SBI Card. This is because 65 percent of its loans are at floating rates and at short repricing tenures. The asset book is at fixed rates. On the other hand, the most negatively impacted NBFC in a rate-cut cycle would be LIC Housing Finance, notes CLSO. This is because 60-65 percent of its borrowings are at fixed rates while 95 percent of assets are at floating rates.

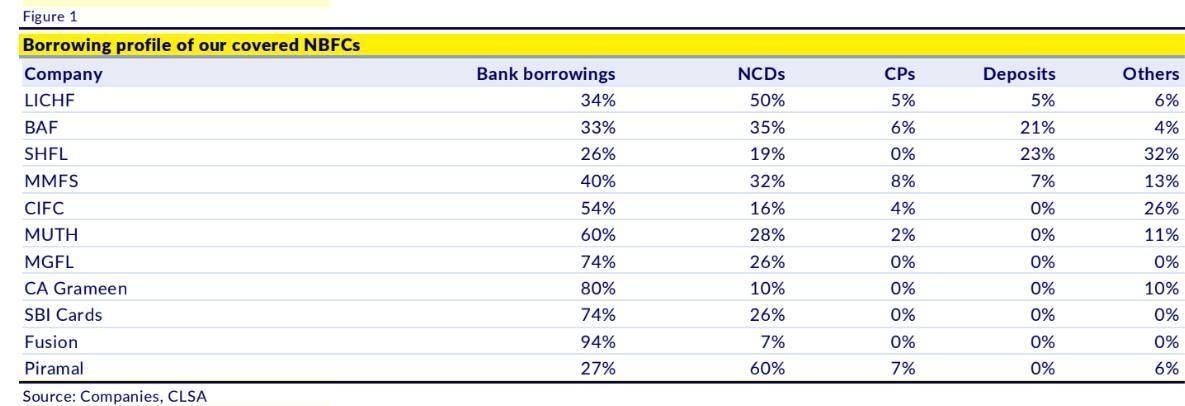

CLSA noted that smaller NBFCs typically rely on bank borrowings for funding, as they are unable to access debt capital markets, due to lack of a strong credit rating. But as companies grow and achieve strong credit ratings, they typically diversify into capital market borrowings as those are usually cheaper than bank borrowings.

The cost of NCDs to rise in FY24

As per the brokerage, most large NBFCs typically have 35-50 percent of borrowings at fixed rates from NCDs for an average of 3 years. It pointed out that the NCDs issued post-Covid (in FY21/22) at very low-interest rates will come up for repayment in FY24/25 and these will be refinanced at almost 100 bps higher rates. It also noted that around 40 percent of the outstanding NCDs will mature in the next two years.

"Simply put, refinancing these NCD borrowings by other NCD borrowings will result in a higher refinancing cost. Can NBFCs then refinance the maturing NCDs by bank borrowings? Yes, they could, but the refinancing cost would be even higher in that case," it said.

Major NBFCs like Bajaj Finance, SBI Card and LIC Housing Finance are likely to see NCDs with below-7 percent rate maturing in FY24, informed the brokerage.

It also highlighted that over the past 10/20 years, the 10-year GSec yield has traded 100-120bp above the repo rate. Today, it trades only 50-60bp above the repo rate, which effectively, means that the bond market has priced in repo rate cuts.

Bank borrowings

The brokerage further mentioned that the bank borrowing costs are also likely to fall but with a lag. The brokerage informed that smaller NBFCs typically borrow mostly from banks as they find it difficult to raise money from debt capital markets, however, as they grow and get better credit ratings, they diversify their borrowing mix. Typically, the cost of NCDs from debt capital markets is lower than that of bank borrowings.

It noted that bank borrowings by NBFCs are linked to both MCLR as well as external benchmarks (mostly repo rate and T-Bills). While repo-linked borrowings would reprice immediately with a repo cut, MCLR-borrowings reprice with a lag (1-12 months). Additionally, the quantum of MCLR cuts is lower than that of repo cuts, said CLSA.

"For example, borrowings pegged to 3-month MCLR reprice every 3 months, while borrowings linked to 1Y MCLR reprice every year. If an NBFC had taken a loan at 1Y MCLR in Sep ’22 when SBI’s MCLR was 7.7 percent, it would continue to pay that rate until Sep ’23, even though the MCLR was hiked to 8.5 percent over the next few months. In such a scenario, the bank borrowing cost in 4QFY23 still reflects the lower locked-in rate (i.e. pegged to 7.7 percent rather than 8.5 percent).

Hence, we believe that the cost of bank borrowings for most NBFCs will reprice upwards in 1HFY24, then remain stable for a couple of quarters. The decline will largely be witnessed in 1HFY25, assuming that RBI starts cutting rates in 3QFY24," CLSA explained.

It also observed that large NBFCs like Bajaj Finance, LIC Housing Finance, M&M Financial, and Shriram Transport have less than 40 percent share of bank borrowings and the only large NBFCs that have a high share of bank borrowings are SBI Cards, Muthoot Finance and Cholamandalam Investment.