FMCG majors Godrej Consumer Products and Britannia have both reported their earnings for the June quarter (Q1FY24). While the profit of both firms missed Street estimates, Britannia's revenue in Q1 was better than expected. But let's analyse, overall, which consumer stock was better at it and what brokerages make of their Q1 results.

Godrej Consumer Products vs Britannia: Which FMCG major reported better earnings in Q1?

TL;DR.

While the profit of both firms missed Street estimates, Britannia's revenue in Q1 was better than expected. But let's analyse, overall, which consumer stock was better at it and what brokerages make of their Q1 results.

Godrej Consumer Products reported a 7.6 percent decline in its consolidated net profit to ₹318.82 crore in the June quarter versus ₹345.12 crore in the same quarter of the previous financial year. Britannia Industries, on the other hand, posted a 35 percent rise in its consolidated net profit at ₹455.45 crore in Q1FY24 from ₹335.74 crore posted a year back. However, sequentially Britannia reported an 18.3 percent fall in profit from ₹557.60 crore in the March quarter.

Meanwhile, Godrej's total revenue rose 10.36 percent to ₹3,448.91 crore in Q1FY24 versus ₹3,124.97 crore in the year-ago quarter. Britannia's revenue also increased 8.36 percent to ₹4,010.70 crore as against ₹3,700.96 crore a year ago.

For Godrej, earnings before interest, tax, depreciation and amortization (EBITDA) came in at ₹642.8 crore, up 23.4 percent while the EBITDA margin advanced 240 bps to 18.6 percent in Q1FY24. For Britannia, EBITDA rose 37.6 percent to ₹689 crore whereas EBITDA margin came in at 17.2 percent, up 370 bps YoY.

Britannia stock price trend

Management View

"This performance was broad-based with Home Care delivering double-digit volume growth and Personal Care in mid-single digits. Our value growth was lower than volume growth as we passed on the benefits of lower input costs to our consumers," said Sudhir Sitapati, Managing Director and CEO of Godrej Consumer.

“We come out of a very successful financial year that witnessed economic recovery amidst unprecedented inflationary conditions. As market leaders, we led pricing actions to offset inflation & maintain profitability. However, in this quarter, commodity prices marginally softened & hence, the local competition intensified. In view of that situation, certain price corrections were initiated to remain competitive & continue to drive topline while maintaining profitability." said Varun Berry, Executive Vice Chairman & Managing Director of Britannia.

Stock Price Trend

In the last one year, Britannia has jumped 27 percent while Godrej has underperformed, rising 15 percent. In comparison, the Nifty FMCG index is also up 21 percent in this period.

Meanwhile, in 2023 YTD, Godrej has outperformed, rising 15 percent as against a 7 percent gain in Britannia. In comparison, the Nifty FMCG index has advanced 17 percent in this period.

Godrej and Britannia, both have given positive returns in 5 of the 8 months of the current calendar year and negative in 3.

Even in the long term - 3 years- Godrej has advanced just 47 percent against just 17 percent returns by Britannia.

Godrej Consumer stock price trend

Which one did it better in Q1?

While both consumer companies have missed Street estimates in Q1FY24, brokerages have retained their bullish outlook more on Godrej Consumer than Britannia. They see up to 16 percent upside for Godrej while they see a limited, up to 10 percent upside, for Britannia.

Motilal Oswal

The brokerage has retained its ‘buy’ call on Godrej Consumer with a target price of ₹1,200, indicating an upside of 16 percent.

"GCPL has been on the right path toward improving India business sales growth in recent years. It delivered double-digit volume growth in 1QFY24 and is likely to deliver double-digit sales/EBITDA/PAT growth over FY24-25E. Disruptive innovations, access packs, and higher but concentrated ad spends should result in consistent healthy growth in this high-margin and high-ROCE domestic business. The profitability outlook is also gradually improving in the overseas business, evident in Q1 through double-digit growth in key geographies. Working capital enhancement, particularly in the international segment, is also progressing as planned," it explained. The brokerage said that it has made no material changes to our FY24/FY25 EPS estimates.

For Britannia, the brokerage has maintained its 'neutral' call with a target price of ₹4,600, indicating a downside of 1 percent.

"Our forecasts already factor in the highest ever annual EBITDA margin going forward (barring the unusually high margin during the Covid-led restrictions, which, as per the management, is unlikely to be replicated). BRIT’s valuations at ~52xFY24E P/E and ~45xFY25E P/E appear rich. Although we are optimistic about its potential in the Packaged Food space in the long run, as well as its remarkable progress in direct distribution and high RoE, we believe the current valuations are already priced in," said the brokerage. The brokerage added that it has made no material changes to FY24/FY25 EPS estimates.

JM Financial

The brokerage has reiterated its ‘buy’ call on Godrej but has raised its target price to ₹1,165 ( ₹1,100) earlier, implying an upside of 13 percent.

"GCPL’s Q1FY24 report was healthier on quality overall. To quote CEO Sudhir Sitapati, the EBITDA margin of the business is now slightly higher than the four-year-ago level even though the gross margin is relatively lower and ad-spends in the business are higher. GCPL’s domestic A&P of 12.5 percent of sales is now higher than any of its HPC peers including HUL – this speaks of the seriousness of its category development intent. On the flip side, the newly acquired Raymond FMCG is likely to stabilise only in 2H. Plus, the currency issue in Nigeria would create some headwinds in FY24 financials. Be that as it may, we believe the execution machinery being put in place is yielding good results with improvement in underlying metrics across geographies alongside higher cash generation. GCPL remains a favoured pick," said JM.

For Britannia, the brokerage has reiterated its ‘buy’ call but raised the target price to ₹5,270 ( ₹5,190 earlier), implying an upside of 10 percent.

"Britannia’s Jun-Q report was a tad better than we expected on topline but growth was entirely price-led and volumes stayed flattish yoy. Britannia’s initiatives on distribution and its sharper execution helped deliver growth in an otherwise weak market, with an additional issue of growing local competition in a softer-input-costs environment. Further, some price corrections were also implemented to counter the higher levels of local competition. Lower pricing should drive ‘volumes’ higher going forward but as it stands today, 2HFY24 looks challenging from topline as well as bottom line perspectives, unless volumes offset the hit from lower pricing. A more aggressive cost-efficiencies program may be needed to boost profitability. The stock could consolidate after the recent sharp run-up, especially since the 2H outlook is not looking all that easy at this point in time," it explained.

Morgan Stanley

The brokerage has an ‘overweight’ rating on Godrej Consumer with a target price of ₹1,072, indicating an upside of 4 percent. It said that Q1FY24 results missed estimates, however, were way ahead of the company’s performance. Improving trends in growth, margin and capacity investments are positives for the company, added the brokerage.

For Britannia as well, the brokerage has retained its ‘overweight’ rating but cut its price target to ₹5,013 (earlier ₹5,184), indicating an upside of 7.5 percent. The brokerage stated that the management's focus was on driving volume growth after a disappointing June quarter performance on this metric. It also noted that that the company was taking necessary actions to reverse the trend. The company is expected to maintain its EBITDA margins, going ahead, it added.

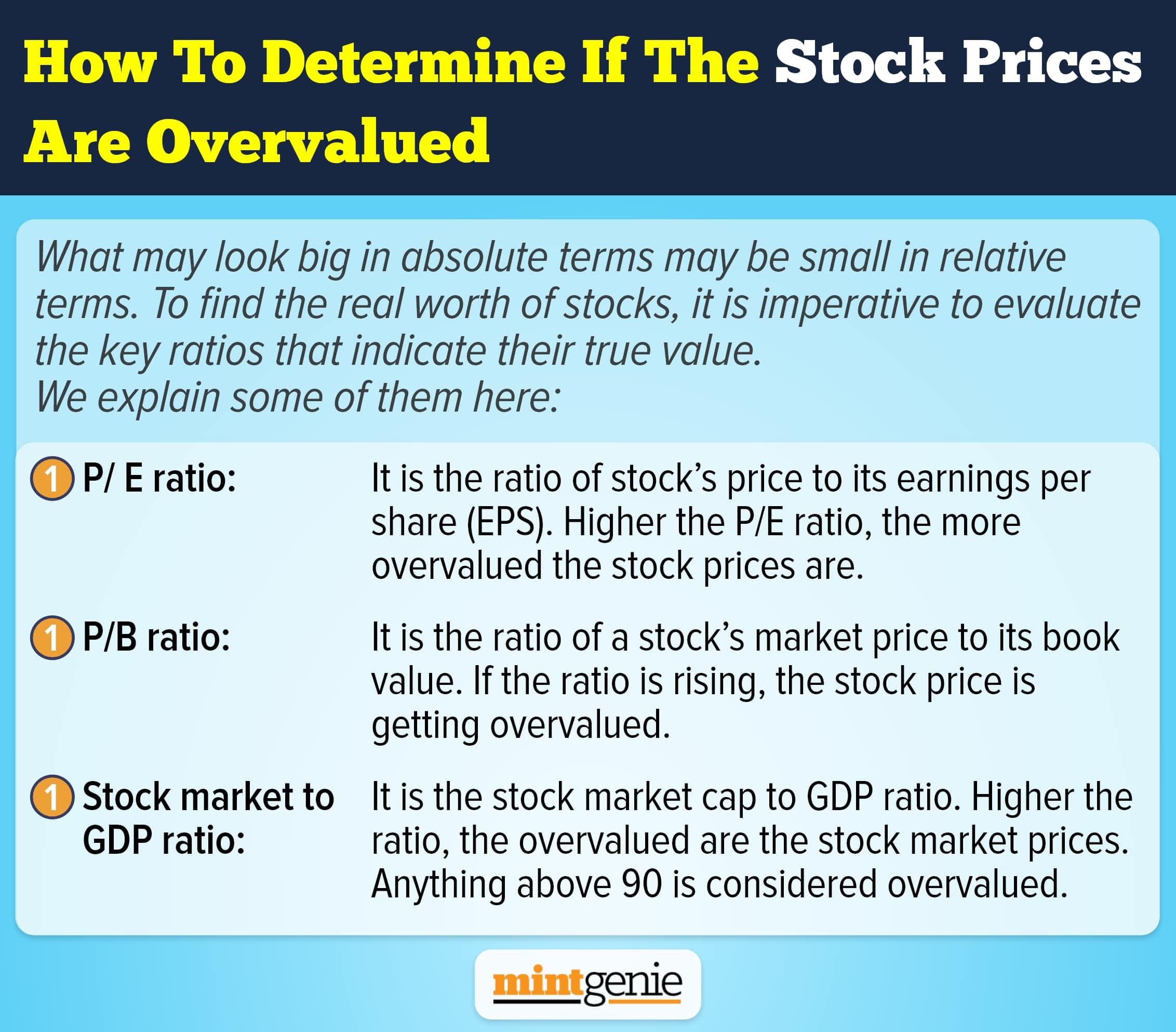

How to determine if the stock prices are overvalued.

First Published: 08 Aug 2023, 04:08 PM IST

Related Stories

Explain Like I am 5

markets

Growth vs Value investing: Which is the better approach to follow?

Prabhat Ranjan,Vijay Chauhan