Private sector lenders ICICI Bank and Kotak Mahindra Bank reported robust earnings for the June quarter (Q1FY24) on July 22. But let's analyse which lender was better at it and what brokerages make of their Q1 results:

ICICI Bank vs Kotak Mahindra Bank: Which lender reported better earnings in Q1?

TL;DR.

Private sector lenders ICICI Bank and Kotak Mahindra Bank reported robust earnings for the June quarter (Q1FY24) on July 22. But let's analyse which lender was better at it and what brokerages make of their Q1 results

While ICICI Bank posted a 40 percent jump in its net profit at ₹9,648 crore for the first quarter of FY24 versus ₹6,905 crore in the year-ago period, beating market expectations; Kotak's net profit also surged 50.62 percent to ₹4,150.19 crore in Q1FY24 driven by a sharp increase in net interest income and improved asset quality.

ICICI's Net interest income (NII) also rose 38 percent YoY ₹18,227 crore in Q1FY24 from ₹13,210 crore in the corresponding quarter last year while Kotak's NII in Q1 surged 33 percent to ₹6,234 crore.

The net interest margin (NIM) of ICICI bank came at 4.78 percent in the quarter compared to 4.01 percent in the same quarter last year, whereas the NIM of Kotak rose 65 bps to 5.57 percent in Q1FY24.

ICICI bank's asset quality improved as the gross non-performing assets (GNPAs) declined to 2.76 percent from 3.4 percent in the year-ago period. The net non-performing assets (NNPA) fell to 0.48 percent from 0.70 percent in the year-ago quarter.

While Kotak also saw an improvement in asset quality the June, with gross non-performing assets (NPAs) declining to 1.75 percent from 2.27 percent in the year-ago period. Net NPA also fell to 0.43 percent against 0.69 percent in a year-ago period.

ICICI Bank

Stock price trend

In the last one year, ICICI Bank has jumped 25 percent while Kotak has underperformed, rising just 6 percent. Meanwhile, in 2023 YTD as well, Kotak is up just 4 percent as against an over 12 percent gain in ICICI.

ICICI has been positive in 5 of the 7 months of the current calendar year whereas Kotak has been in the green in 4. ICICI has surged the most in July so far, up 6.7 percent and shed the most in Jan, down 6.6 percent. Meanwhile, Kotak rose the most in April, up almost 12 percent and fell the most in June, down 8.3 percent.

Even in the long term - 3 years- Kotak has advanced just 44 percent against multibagger returns by ICICI, which surged almost 162 percent in this period.

Kotak Mahindra bank

What brokerages say?

While both private sector lenders have posted strong results for Q1FY24, beating analysts' expectations, brokerages are more bullish on ICICI than Kotak. Brokerages see up to 33 percent upside for ICICI while they see limited, up to 17 percent upside for Kotak. However, they raised earnings estimates for both banks.

Axis Securities: The brokerage has a buy call on both stocks but raised its target price to ₹2,300 (from ₹2,180) for Kotak and maintained TP at ₹1,205 for ICICI, implying upside potentials of almost 17 percent and 21 percent, respectively.

Axis expects KMB’s business growth to remain buoyant over the medium term. Even as margins contract (though remain well above 5 percent) on the back of a sharp increase in the cost of funds (CoF) and credit costs gravitate to normalised levels, it believed improving cost ratios should support the bank to deliver a consistent RoA of 2.4 percent and RoE of 14-14.5 percent over FY24-25E. It also estimates KMB to report healthy credit/deposit growth of 17-18 percent CAGR over FY24-25E. Even as margins moderate, it sees them remaining healthy at 5.3 percent over the medium term, driving NII growth of 17 percent CAGR over FY23-25E. Axis maintains its estimates for FY24E and marginally tweak our FY25E NII/PAT estimates upwards by 2 percent/3 percent respectively.

Meanwhile, for ICICI, Axis said that it continues to like the lender for its (1) Strong retail-focused liability franchise, (2) Buoyant growth prospects, (3) Stable asset quality along with adequate provision buffers, (4) Adequate capitalization and (5) Potential to deliver robust return ratios. ICICIB has been consistently outperforming over the past few quarters. The bank has entered FY24 on a strong footing and Axis expects the momentum to continue. No major asset quality challenges are visible and the benign credit cost trajectory should continue. Additionally, the bank continues to hold adequate provision buffers, which is comforting. Despite margin pressures and higher Opex growth, it estimates ICICIB to deliver a healthy PPOP/Earnings growth of 15/16 percent CAGR over FY23-25E and a consistent RoA/RoE of 2-2.2 percent/17-18 percent over FY24-25E.

JM Financial: The brokerage has buy calls on both the lenders with a target of ₹1,155 for ICICI (16 percent upside) and ₹2,205 for Kotak (12 percent upside).

The brokerage believes Kotak’s valuation premium vs other private sector peers has meaningfully compressed over the last couple of years. While leadership change has been a key overhang, it sees any incremental clarity w.r.t the same acting as a positive trigger. Meanwhile, Kotak has accelerated growth and continues to report best-in-class RoAs. It also believes clarity in leadership transition will be key trigger and inorganic growth opportunities with complementary products/geographies could add further upside thus offering compelling risk-reward. It raised earnings estimates to factor in strong NIMs, it said. It expects Kotak to grow loans/deposits both at 18 percent CAGR over FY23-25 while forecasting an NII CAGR of 20 percent over the period. It believes Kotak offers a best-in-class risk-adjusted margin profile, strong balance sheet and now healthy growth (Kotak has the highest 2 yr-CAGR in loans over FY21-23 amongst larger pvt banks).

For ICICI Bank, the brokerage stated that its 1QFY24 results were another strong show of growth and profitability despite rising funding costs. As per JM Financial, ICICI Bank is clocking strong RoAs of 2.4 percent for the last couple of quarters and the ability to sustain 2 percent+ RoAs while maneuvering NIMs will ensure continued outperformance of the stock. ICICI Bank’s share of unsecured products is 13 percent (vs 16.5 percent for HDFC Bank) and it expects a further rise in the share of these products to offset the cost of funds impact on NIMs. It also estimates ICICI Bank to deliver RoAs of 2.27 percent/2.22 percent in FY24/FY25.

Emkay: The brokerage has a buy call on ICICI but a hold call on Kotak. It has a target price of ₹1,330 for ICICI, indicating an over 33 percent upside, however for Kotak, its target price of ₹2,000 implies just a 1.5 percent upside.

Despite the sharp fall in NIM (by 18bps QoQ), Kotak Mahindra Bank (KMB) reported a beat on earnings mainly due to higher ‘other income’ including treasury gains/dividend income. It believes the sharper NIM contraction was due to moderate retail growth and higher CoF. It raised earnings by 2-4 percent for FY24-26E, building in higher other income, but expect KMB’s RoA/RoE to normalize to 2.1 percent/13 percent from the high of 2.4 percent/14 percent in FY23 due to margin normalization.

For ICICI, it said that the lender continues to report strong profitability led by system-beating credit growth YoY and NII growth. It expects NIMs to moderate QoQ as costs catch up but should be still up 15-20 bps for a full year in FY24E, as the pace of fall should be slower vs the rise in FY23. Factoring in the healthy NIMs, coupled with fees/lower LLP, it revises earnings for FY24-26E by 3-7 percent and expects Bank to deliver superior RoA of 2.2-2.3 percent and RoE of 18 percent over the same period. It takes comfort from the strong leadership back-up at ICICIB and is hopeful that the bank remains adaptive to limit the unwarranted attrition/business dislocation, as it aspires to build up into a “sustainable & profitable bank” in the long run. ICICIB remains Emkay's top pick in the banking space, given its superior returns profile, top-Management credibility and strong capital/provision buffers.

Motilal Oswal: The brokerage has a neutral call on Kotak and buy call on ICICI post their June quarter earnings. It has a target of ₹2,170 for Kotak, implying a 10 percent upside, whereas for ICICI, it has a TP of ₹1,150, indicating a 15 percent upside.

"KMB delivered a healthy quarter with steady revenue growth and stable asset quality. NIM contracted due to the rising cost of deposits but was on expected lines. Asset quality remained steady, aided by healthy recoveries, while the restructured book moderated to 20bp of loans. KMB carries additional Covid-related provisions of ₹340 crore (10bp of loans). We raise our earnings estimates by 7 percent/5 percent for FY24/25 and expect KMB to deliver RoA/RoE of 2.4 percent/14.3 percent in FY25," it said for Kotak.

For ICICI, the brokerage stated, "ICICIBC reported another steady quarter, driven by healthy NII/Core PPoP growth and controlled provisions underpinned by stable asset quality. The stable mix of the high-yielding portfolio and a low-cost liability franchise drove steady NII growth. The bank is seeing a strong recovery across segments, while asset quality trends remain healthy with PCR at 83 percent. We estimate ICICBC to deliver RoA/RoE of 2.2 percent/17.9 percent in FY25. After a strong outperformance backed by robust earnings growth (3yr CAGR of 60 percent), we estimate earnings growth to moderate to an 18 percent CAGR over FY23-25, affected largely by a decline in margins and limited levers available on the opex/credit cost front. We expect stock returns to be more moderate for ICICIBC and many other large-cap banking stocks."

HDFC Securities: The brokerage has a buy call on ICICI Bank and an add call on Kotak Mahindra Bank. It has a target price of ₹1,200 for ICICI and ₹2,205 for Kotak, indicating upside potentials of over 20 percent and 12 percent, respectively.

For Kotak Mahindra Bank, the brokerage noted that it has delivered a strong beat, driven by healthy loan growth and trading gains, partly offset by marginally higher credit costs. Loan growth was broad-based across segments, with continued traction in unsecured retail in line with KMB’s efforts to improve its share of high-yield products. Deposit mobilisation also picked up pace primarily from the active money pool, addressing an immediate concern around the elevated loan-to-deposit ratio even as the CASA ratio witnessed a sharp 400 bps QoQ moderation. While KMB’s move to chase better yields through a higher mix of unsecured has merit, The brokerages see challenges around elevated funding costs. It has tweaked its FY24/FY25 estimates to factor in higher opex and credit costs, offset by slightly better NIMs from a change in the mix

For ICICI Bank, it noted that the lender reported yet another impressive quarter on the back of strong loan growth, treasury gains, and continued robust asset quality. As a result, credit costs were further moderated given healthy PCR and contingent provisions, translating into record standalone RoAs of 2.4 percent. ICICIBC improved its pace of deposit mobilisation mainly from retail TDs, reflecting in moderation in NIMs, due to lagged deposit repricing in line with peers. The brokerage also tweaked its FY24E/FY25E forecasts to factor in higher opex offset by lower credit costs.

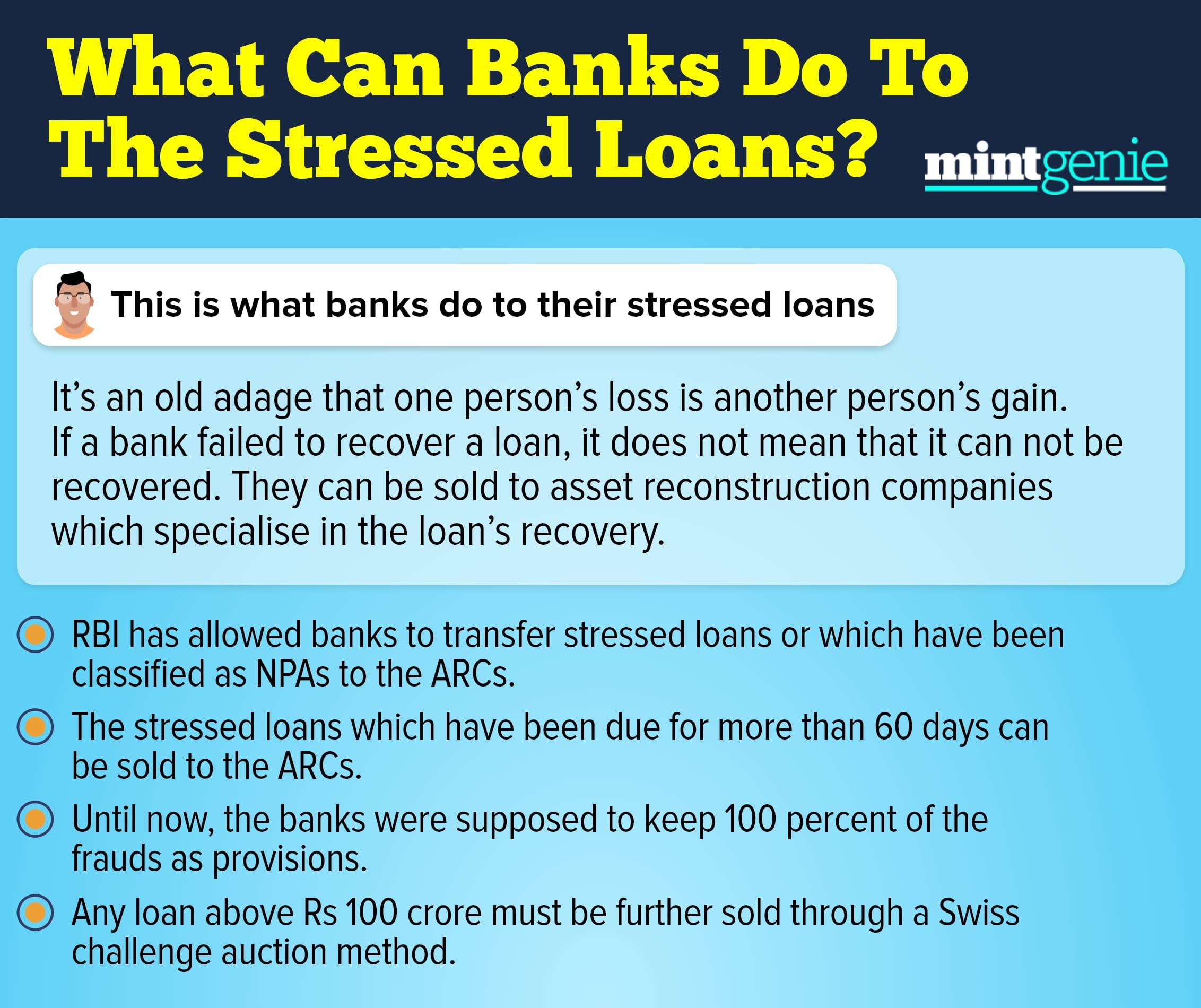

This is what banks can do to the stressed loans.

First Published: 24 Jul 2023, 02:38 PM IST

Related Stories

Explain Like I am 5

markets

What are the investing mistakes retail investors make and how to avoid them?

Manik Kumar Malakar