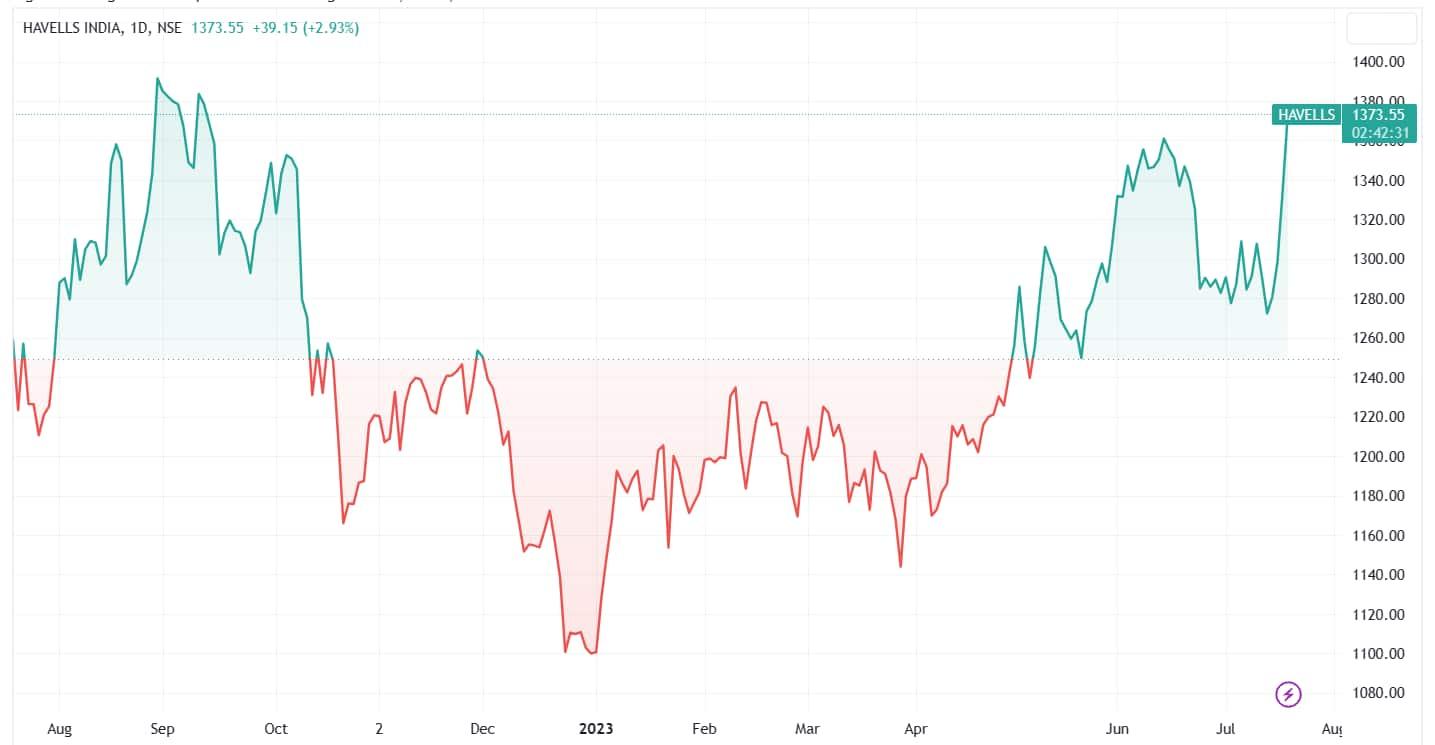

Havells India's shares continued their winning streak for the fourth consecutive trading day, surging 3.8% to reach ₹1,385 apiece, in Wednesday's session. The stock is now only 2.35% below its 52-week high of ₹1,405 and 9% away from its all-time high of ₹1,501, achieved in October 2021.

Looking ahead, brokerage firm Motilal Oswal expects the stock to continue its upward trajectory and likely record a new all-time high.

The brokerage has reinitiated coverage on Havells India with a 'buy'' rating and a price target of ₹1,580 based on 55x FY25E EPS. The brokerage believes that Havells has the potential to maintain premium valuations given the earnings CAGR of 29% over FY23–25E and strong return ratios.

The total addressable market (TAM) of Havells stands at ₹2.2 trillion, the largest among its listed peers in the Indian Appliances and Consumer Electronic Industry, which was estimated to be worth ₹2.4 trillion in FY22 and is expected to achieve a 10% CAGR over the next five years.

The brokerage foresees Havells benefiting from the anticipated growth in the white goods segment, along with continued expansion in its core portfolio, which encompasses cables and wires, switchgear, lighting, and other segments. This expansion will be fueled by the strong momentum of the real estate industry, providing Havells with a conducive environment for further growth and market penetration, it added.

The acquisition of Lloyd has facilitated Havell's entry into the lucrative large home appliances segment. Its product portfolio now consists of 20 products across categories, as compared to 9 and 15 in FY10 and FY17, respectively.

Lloyd has achieved a market share of over 10% in room air conditioners (RAC), compared to 8% a few years ago, solidifying its position among the top three players in this segment. Leveraging the success of its AC products, Lloyd is well-positioned to drive growth in other offerings, such as washing machines and refrigerators.

In FY23, Lloyd contributed 20% to Havells revenue. Thus, the brokerage estimates Lloyd’s revenue share to rise to 22.2% and 23.5% in FY24 and FY25, respectively.

To strengthen its brand affinity, Havells has made strategic investments through various channels, such as national advertising, regional brand ambassador associations, celebrity engagement, digital campaigns, brand shops, in-shop advertising, and participation in trade shows, said the brokerage.

Furthermore, Havells' commitment to research and development (R&D) allows it to offer differentiated products. In FY23, the company's R&D spending increased by 48% YoY to ₹1.6 billion, with 1% of its revenue allocated towards R&D (compared to 0.8% in FY22).

Havells applied for 38 new patents and 213 new design registrations in FY23, bringing the tally to 150 patents.

On the earnings front, the company's gross margin was under significant pressure (the lowest in a decade) in FY23 due to higher commodity prices, as it was not able to pass on the entire cost increase to consumers.

However, Motilal Oswal believes the company's profitability will improve, driven by softening commodity inflation, a rise in premium product mix, operating leverage, and a rising share of in-house manufacturing.

Motilal Oswal projects a revenue CAGR of 13% over FY23–25, with an estimated EBITDA/PAT CAGR of 27% and 29% in the same period. EBITDA margin is expected to reach 10.6% and 12.1% in FY24E and FY25E, respectively, compared to 9.5% in FY23, according to the brokerage.

Motilal also anticipates an improvement in Return on Equity (RoE), Return on Capital Employed (RoCE), and Return on Invested Capital (RoIC) to 21%, 20%, and 30% in FY25, respectively.

41 analysts polled by MintGenie on average have a 'buy' call on the stock.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.