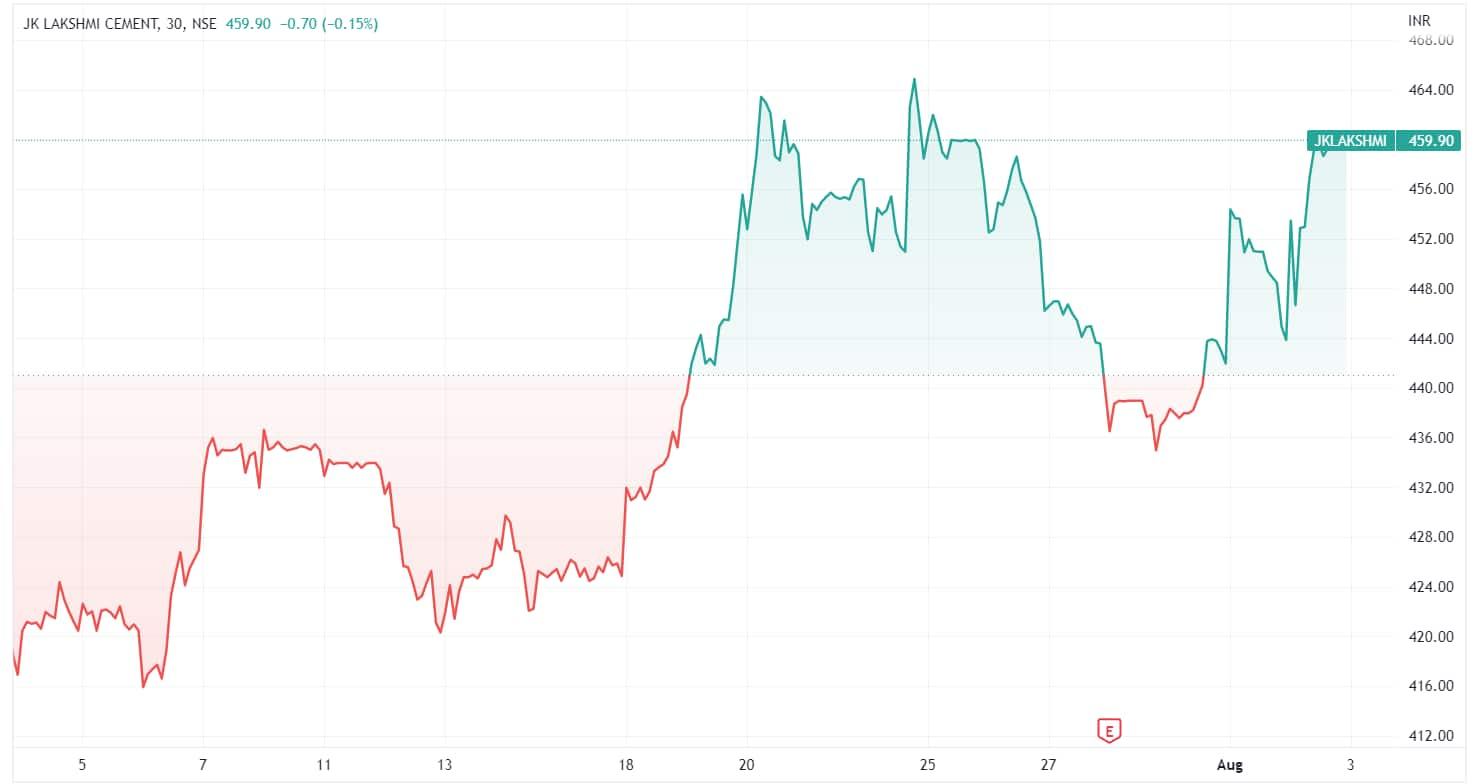

Shares of JK Lakshmi Cement fell 0.61 per cent in Wednesday's trade.

Since its Q1 result announcement on July 27, the stock has gone from ₹441.70 to ₹460 levels, delivering a return of over 4.30%.

The stock is currently trading 25.40% higher than its 52-week low of ₹366.25 and 38.55% lower than its 52-week high of ₹747.60.

Cement companies have been under pressure for the last few months due to a rise in raw material costs. The rising input costs of fuel, petcoke, and coal prices have impacted the gross margins of cement companies in the June quarter. Furthermore, higher oil prices have also resulted in higher fuel prices, resulting in increased freight expenses.

The price of pet coke hit a high between March and April on the back of geopolitical tensions. Petcoke is widely used by the cement industry. Any sharp rise in this commodity may increase the operating expenses of cement players.

JK Lakshmi Cement Ltd. reported a 15.49 per cent decline in its consolidated net profit of ₹115.07 for the first quarter ended June, as against a profit of ₹136.17 crore in the April-June period a year ago.

The company's total expenses stood at ₹1,489.10 crore, up 28.6 per cent in Q1FY23 compared to ₹1,157.88 crore. Revenue from operations increased by 24.78 per cent to ₹1,654.14 crore in Q1, compared to ₹1,325.58 crore the previous year.

Further, the company’s EBITDA fell marginally to ₹256.9 crore in Q1FY23 as against ₹258.3 crore in the corresponding quarter of last year.

The company said its operating profit margin in the June ending quarter was impacted due to cost pressure.

Over the last 3 years, the stock has given decent returns to its shareholders, with 40% gains, and in the last month, it rallied 10% and 2.49% in a week.

Domestic brokerage firm HDFC Securities is bullish on the stock after Q1 numbers. The brokerage firm has a target price of ₹680/share on JKL, which hints toward an upside of 48 per cent from its latest close.

According to the brokerage firm, JK Lakshmi's healthy cash flow will support its Udaipur expansion without straining its balance sheet.

Its net debt on books remained flat QoQ, despite the fact that its Udaipur plant expansion has accelerated, it said.

An average of 18 analysts polled by MintGenie have a 'buy' call on the stock.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.