The hotel industry witnessed a strong December quarter of FY23 (Q3FY23) aided by an increase in the average room rate (ARR), which led to higher revenue per available room (RevPAR) despite lower occupancy versus pre-Covid levels, noted a report by Motilal Oswal.

As per HVS Anarock, the occupancy rate (OR) stood at 65 percent in Q3FY23, a little lower than pre-Covid levels (down 170 bps v/s Q3FY20). OR was affected by a drop in business travel in Oct’22 because of the festival season, but it bounced back in Nov’22 and Dec’22 to 69 percent each from 57 percent in Oct’22, reported MOSL.

Meanwhile, the ARR kept on rising to ₹7,233 (up 16 percent v/s Q3FY20), informed the brokerage.

Going ahead, the brokerage believes OR is expected to again surpass the pre-Covid levels in the coming quarters on the back of strong demand drivers such as the wedding season, G20 Summit meetings, the ICC ODI Cricket World Cup and the resumption of foreign inbound travel. ARR should continue to inch higher, thereby boosting RevPAR.

Earnings Review

Overall In 3QFY23, the brokerage informed that the aggregate revenue for the hospitality basket grew 56 percent YoY, 34 percent QoQ and 20 percent v/s 3QFY20 to ₹3630 crore as the hotel industry has returned to normalcy. ITC led the pack with 29 percent growth (v/s 3QFY20), followed by Indian Hotels (24 percent), aided by higher ARR.

Meanwhile, the brokerage added that the EBITDA for the basket came in at ₹1300 crore in 3QFY23, higher by 2x YoY, 74 percent QoQ and 34 percent v/s 3QFY20.

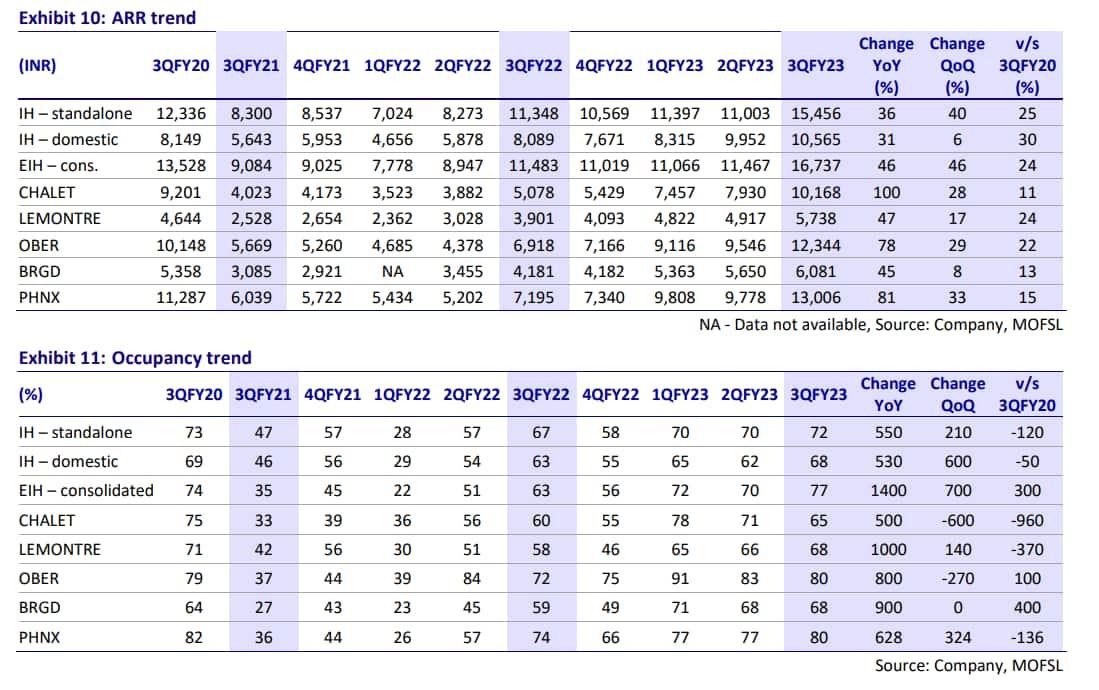

LEMON TREE registered the highest EBITDA growth of 56 percent v/s 3QFY20, followed by ITC and Indian Hotels at 45 percent and 40 percent, respectively. Sequentially, EBITDA margins across the hotels expanded by 830bp, mainly due to the seasonality factor, it stated.

Adjusted net profit of the hospitality basket stood at ₹610 crore in 3QFY23 v/s ₹190 crore in the September quarter and ₹350 crore in Q3FY20, mentioned MOSL.

Compared to pre-Covid levels, LEMONTREE reported the highest flow-through in Q3FY23 at 133 percent, followed by EIH and IH standalone at 72 percent and 59 percent, respectively. Meanwhile, ITC, Oberoi and Chalet Hotels posted a flow-through of 43 percent, 14 percent and 1 percent, respectively, said the brokerage.

Operating Performance

Hotels registered a better-than-expected operating performance in Q3FY23. All players witnessed QoQ growth in RevPAR, with EIH registering the maximum increase of 61 percent QoQ, followed by IH standalone at 45 percent, as per the brokerage.

Compared to pre-Covid levels, RevPAR grew for all the players (except CHALET), aided by higher ARR, while OR was a mixed bag. EIH/IH domestic network RevPAR recorded the highest growth at 29 percent each versus Q3FY20, followed by IH standalone/OBEROI at 23 percent each, it further mentioned.

Also, MOSL pointed out that RevPAR for IH domestic network and standalone operations was led by ARR growth of 30 percent and 25 percent, respectively in Q3FY23, with a 50bp and 120bp decline in OR v/s 3QFY20.

Meanwhile, RevPAR for EIH domestic network hotel (including management contracts) rose 29 percent to ₹12,887 in 3QFY23 v/s 3QFY20, led by a 300 bp improvement in OR to 77 percent. ARR improved 24 percent v/s 3QFY20, it added.

LEMONTREE’s RevPAR grew 17 percent in Q3FY23 v/s 3QFY20, led by a 24 percent rise in ARR to ₹5,738, while OR was down 370 bps, noted MOSL.

Finally, CHALET’s RevPAR was down 3 percent in 3QFY23 v/s 3QFY20 and ARR grew 11 percent to ₹10,168. OR declined significantly by 960bp v/s 3QFY20, it added.

Valuation and View

As per the brokerage, OR is expected to improve from pre-Covid levels on the back of strong demand drivers such as the wedding season, G20 Summit meetings, the ICC ODI Cricket World Cup and the resumption of foreign inbound travel. ARR should continue to inch higher, thereby boosting RevPAR.

It anticipates robust growth to remain intact across hotels in FY24, aided by: 1) an increase in ARR across hotels on improved occupancy, 2) operating leverage, and 3) a favorable demand-supply scenario.

It reiterated a BUY rating on IH with a target price of ₹410 for FY25 and BUY on LEMONTREE with a target of ₹115 for Dec’24.