ICICI Bank and HDFC Bank are two major private sector lenders, both of which have been top choices for investors and analysts alike. But have you ever questioned if one is better than the other, let's find out?

ICICI Bank vs HDFC Bank: Which banking stock to choose for long-term investment? 7 analysts have this unanimous choice

TL;DR.

ICICI Bank and HDFC Bank are two major private sector lenders, both of which have been top choices for investors and analysts alike. But have you ever questioned if one is better than the other, let's find out?

Stock prices

On the basis of only stock market returns, ICICI Bank seems to have an upper hand over HDFC Bank. ICICI Bank has given multibagger returns in the last 3 years, up 127 percent as against a 36 percent rise in HDFC Bank. In 2022 YTD as well, ICICI Bank has added 23 percent versus a 2 percent rise in HDFC Bank. And in the last 1 year, ICICI Bank is up 26 percent as compared to a 5 percent fall in HDFC Bank.

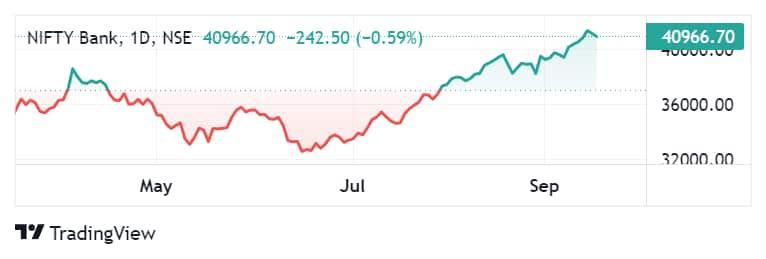

In comparison, the Nifty Bank has risen 9 percent in the last 1 year and 15 percent in 2022 so far.

Since July, ICICI Bank has advanced nearly 25 percent while HDFC Bank has added around 10 percent post their robust June quarter earnings.

About the firms

ICICI Bank provides various banking products and financial services in India and internationally. It operates through Retail Banking, Wholesale Banking, Treasury, Other Banking, Life Insurance, General Insurance, and Other segments. As of June 30, 2022, it had a network of 5,534 branches and 13,379 ATMs. ICICI Bank Limited was founded in 1955 and is headquartered in Mumbai, India.

ICICI Bank stock price trend

HDFC Bank Limited provides banking and financial services to individuals and businesses in India, Bahrain, Hong Kong, and Dubai. It operates in Treasury, Retail Banking, Wholesale Banking, Other Banking Business, and Unallocated segments. The company operates 6,378 branches and 18,620 automated teller machines in 3,203 cities/towns. As of March 31, 2022, it had 21,683 banking outlets. The company was incorporated in 1994 and is based in Mumbai, India.

Earnings

In terms of financials, both banks delivered a strong set of earnings in the last quarter. India's second biggest private sector lender ICICI Bank logged a 50 percent year-on-year (YoY) rise in profit after tax (PAT) at ₹6,905 crore in the June quarter as against ₹4,616 crore in the corresponding quarter last year.

Net interest income (NII) rose 21 percent YoY to ₹13,210 crore and its net interest margin (NIM) for the June quarter stood at 4.92 percent versus ₹10,936 crore in the same quarter last year. Its total income during the Q1 FY23 also rose to ₹28,336.74 crore from ₹24,379.27 crore in Q1 FY22.

On the other hand, India's largest lender HDFC Bank's net profit increased 19 percent to ₹9,195.99 crore in the June quarter from ₹7,729.64 crore in the year-ago period but was down from ₹10,055.18 crore in the preceding March quarter. Its total income rose to ₹41,560 crore on a standalone basis, as compared to ₹36,771 crore in the year-ago period.

The private lender's net interest income (NII) rose 14.5 percent YoY to ₹19,481.4 crore from ₹17,009 crore in the same quarter last year.

HDFC Bank's net profit has grown at a CAGR of 15.5 percent over the last five years as compared to ICICI Bank's net profit growth of 27.3 percent. Despite higher provisions, ICICI Bank's net profit growth is higher than HDFC Bank, indicating operational efficiency.

HDFC Bank stock price trend

Which is better?

Last month, Jefferies, in a note, pointed out the fact that ICICI Bank offers the best risk-reward mix among all global banks. It said the lender would report superior returns on assets on a consistent basis and has enough firepower to participate in India’s credit recovery without accidents of bad loans.

Sunil Damania, Chief Investment Officer, MarketsMojo also agrees.

Between the two, ICICI Bank is a better investment. "The reason is straightforward - growth is higher with ICICI Bank. The bank's new CEO is taking proper steps and strategies to ensure ICICI Bank remains ahead of the curve. On the other hand, HDFC Bank is still grappling as it's unable to fix its digital strategy," he said.

Further, while Siddarth Bhamre, Head of Research, Religare Broking believes both lenders are good buys, he predicts ICICI Bank will outperform, even though not by a wide margin.

"Historically ICICI Bank on P/ABV basis always traded at discount to HDFC Bank as the latter had consistency and higher growth visibility. In the last couple of years, we have witnessed higher and consistent growth visibility in ICICI as its product mix changed with the weightage of the retail portfolio moving higher which has lesser delinquency issues. HDFC Bank had an issue related to its card business and was witnessing slower growth than before.

Now ICICI Bank trades at a slightly higher P/ABV than HDFCBANK as its stock outperformed from March 2022 till date by a wide margin. Going forward we believe ICICI Bank may continue to outperform though not by a very wide margin and hence both stocks are a good buy from a long-term perspective," explained Bhamre.

Another one in favour of ICICI Bank is Vinit Bolinjkar of Ventura Securities. He believes that ICICI Bank is better placed than HDFC Bank due to its recent business performance and improvement in its operating metrics.

ICICI Bank's strongest performance point has been its NII growth in Q1FY23, which was higher than HDFC Bank's, he noted. He also pointed out that ICICI Bank's loan book has witnessed significant changes in its overall mix. Post the pandemic, ICICI's book has turned retail heavy while HDFC Bank has ventured into big wholesale lending, he said.

"If one goes by valuation, ICICI Bank is trading at FY25 P/B of 2.2x compared to 2.6x of HDFC Bank. So, ICICI Bank, which has witnessed significant improvement in its metrics is available at a cheaper valuation. Earlier this gap was larger but has been recently bridged largely because of HDFC Bank's valuation erosion over the past couple of years owing to concerns over uncertainty surrounding its merger with HDFC and a management change," explained Bolinjkar.

Axis Securities also noted that both ICICI Bank and HDFC Bank have been performing well operationally. However, in the near term, it believes ICICI Bank will continue to outperform its peers, backed by sustained momentum in credit growth, NIM expansion, benign credit costs, and strong asset quality.

"HDFC Bank has been a steady performer in terms of credit growth, stable asset quality, and superior return ratios across credit cycles. However, the concerns around the merger are an overhang and are likely to overshadow the business performance, thereby potentially weighing on the stock’s performance. However, over the longer term, we believe the merger will be value accretive. Over the medium to long term, we like both ICICI Bank and HDFC Bank," stated the brokerage.

Vinod Nair, Head of Research at Geojit Financial Services also believes HDFC Bank will underperform in the near term. "Pre-pandemic, HDFC Bank used to enjoy a significant premium compared to ICICI Bank given its consistent performance, superior asset quality, and stronger parentage. However, the valuation premium declined facing multiple headwinds like technology concerns, RBI restrictions and merger overhang, while ICICI Bank witnessed a recovery in its business performance. Post the pandemic, HDFC Bank has been focusing more on wholesale lending, which has put pressure on margins. We are positive on both the banks, but HDFC Bank is a better bet in the long term as it is expected to overcome these near-term headwinds and is available at discounted valuations. However, in the near term HDFC Bank can continue to underperform," he said.

Meanwhile, Pranjal Kamra - CEO, Finology Ventures stated that though ICICI is expected to outperform in the near term, we believe both of these are well placed to ride on the credit cycle in the medium to long-term perspective.

"When comparing the two largest Private lenders: HDFC Bank and ICICI, the former has consistently dominated the market in terms of valuation up until recently. But with strong growth metrics, improving asset quality & ROE expansion, ICICI took a lead with a trailing P/BV of 3.5x Vs HDFC’s 3.43x. HDFC Bank has consistently reported reduced and steady NPAs across interest cycles, while ICICI Bank's credit quality has fluctuated significantly but has seen a drastic improvement in recent times. The concern related to technology and uncertainty around the mega-merger with HDFC is the primary reason for the underperformance of HDFC Bank, but we believe that these factors are already priced in," he said.

Outlook

The banking sector is expected to outperform on account of improving economic outlook and credit growth recovery. Another factor that outweighs the segment is strong buying by FIIs. Due to the low cost of funds and scale advantages, large-sized banks will benefit the most from this trend, say experts.

Nifty Bank stock price trend

First Published: 18 Sep 2022, 09:54 AM IST