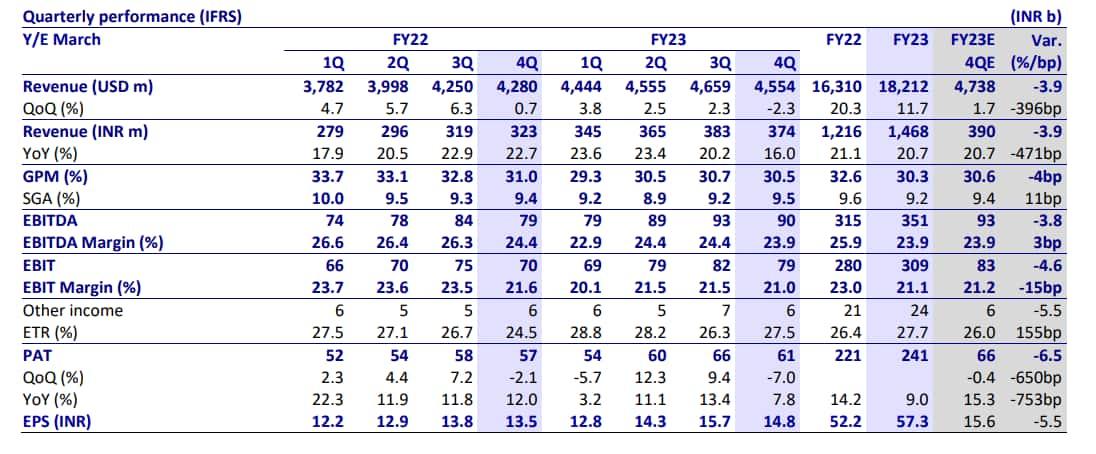

Infosys delivered weak March quarter (Q4FY23) results with the revenue of the company down 3.2 percent sequentially. EBIT margin at 21 percent also undershot Street’s expectations of 21.5 percent, while, FY24 revenue growth guidance of 4–7 percent and margins of 20–22 percent are also disappointing.

Infosys Q4 Review: Most brokerages downgrade stock, cut targets; here's when they see it recovering

TL;DR.

After the March quarter results, many brokerages downgraded the stock and almost all cut their target prices and earnings estimates for FY24 and FY25.

The management talked about delayed decision-making and an uncertain environment compounded by the recent banking crisis.

Post the March quarter results, many brokerages downgraded the stock and almost all cut their target prices and earnings estimates for FY24 and FY25. They believe any recovery in the firm is unlikely before FY24, and only if the macro situation improves.

Let's take a look at what various brokerages have to say about the IT major post its March quarter results:

Sharekhan

The brokerage downgraded Infosys to ‘hold’ after its Q4 results. It has a target price of ₹1500 on the stock, indicating an upside of just 8 percent. Infosys delivered a surprisingly weak Q4, with a 3.2 percent QoQ decline in its CC revenue, missing estimates on account of unplanned project ramp downs and owing to one-time revenue impact due to cancellations and specific client issues, said the brokerage. Given the weak quarterly numbers and uncertain macro backdrop, it expects the stock to underperform in the near term. Sharekhan sees muted 3.7 percent and 5.4 percent sales and PAT CAGR, respectively over FY23-25E

"After continued financial outperformance among its peers for major portion of FY23, the surprisingly weak Q4FY23 numbers from Infosys highlights the vulnerability from deteriorating macros despite robust deals win and deal pipeline. FY24 guidance seems to be modest, lagging behind our expectations both in terms of revenues and margins. Further, the quarterly ask rate of 1.7-2.8 percent for FY24 CC revenue guidance of 4-7 percent, appears steep given the tough near-term macro environment, also peer TCS in its recent commentary hinted that growth is likely to be back-ended due to near-term uncertainty. Given the weak quarterly numbers and uncertain macro backdrop, we expect the stock to underperform," explained the brokerage.

HDFC Securities

The brokerage downgraded the stock to ‘add’ from ‘buy’ call earlier. It has also reduced the target price of the stock by around 20 percent to ₹1,470 ( ₹1,830 earlier), indicating an upside of just 6 percent. It has also cut earnings estimates for the IT major by 4-5 percent for FY24-25.

"The near-inevitable happened, but Infosys’ Q4 can pass on as an aberration even as macro headwinds persist. The low probability sequential decline was due to a combination of deal cancellations and deferrals largely centric in North America. So the cut in estimates is a bigger function of the FY23 exit rate rather than the guidance provided (4-7 percent CC). We reckon that there’s a high probability of Infosys delivering the mid-point of its guidance band and improving its growth trajectory beyond. We also believe that there’s a low probability of structural risk to the margin. However, recent senior-level exits and the possibility of continued stress from large accounts are risks to growth," warned the brokerage.

Reliance Research

In view of rising concern on the global slowdown and delayed decision-making in the US, the brokerage remains cautious on the stock. Due to lower earnings growth and valuation, it downgraded Infosys to ‘sell’ from ‘buy’ with a revised TP of ₹1,350 (vs earlier ₹1,750).

IT services have started witnessing the impact of worsening global macros in terms of economic slowdown and cut on spending, which the brokerage expects to continue in FY24E. Single-digit revenue growth, limited margin improvement and lower earnings growth closer to the pre-Covid era would lead to a valuation multiple contractions to the pre-Covid level, it noted. It expects the company’s revenue/EBIT/PAT to clock 9 percent/13 percent/13 percent CAGR over FY23-FY25E.

"We believe that situation deterioration just started in Feb-Mar’23, which would escalate further in 1HFY24, before bottoming out. Thus, uncertainty in US and EU regions coupled with pricing pressure would lead to a challenging FY24. FY24 would see a sizable impact of the slowdown and adverse macros, which is also reflected in major revenue and margin miss. Worsening macros, lower revenue and earnings growth would lead to valuation de-rating to pre-Covid levels," said the brokerage.

Nirmal Bang

The brokerage has retained its ‘sell’ call on the stock with a target price of ₹1,202, indicating a downside of 13.5 percent. Whether there will be a ‘V-shaped’ recovery in IT industry revenue is entirely dependent on whether inflation in the US falls to 2 percent or below and we go into another round of quantitative easing, said the brokerage. In the longer term, concern with Infosys remains on its margins, cautioned Nirmal Bang.

"While the Infosys stock is going to see pressure in the immediate term, we would not want to rush in to buy. As stated earlier, we believe the worst on the US macro front is ahead of us. We expect volume and pricing pressure (even if it is modest) to play out, which could lead to further cuts in consensus estimates. We think there could be further multiple compression too. As things stand today, we think that the right time would come sometime in 2H2023 or in 1H2024," recommended the brokerage.

Nuvama

While the brokerage has retained its ‘buy’ call on the stock, it has cut the IT major's target price by 15 percent to ₹1,610 from ₹1,900 earlier. The new target indicated a potential upside of 16 percent for the stock. The brokerage also reduced Infosys' FY24/25E EPS by 6 percent/7 percent on lower growth and margins.

A lower FY23 exit rate and weak deal flow led to Infosys guiding for FY24 CC revenue growth of 4–7 percent, noted the brokerage. A lower and broader range of guidance represents the uncertainty that the company is facing. Infosys now requires 1.7 percent to 2.8 percent CQGR (compounded quarter growth rate) over the next four quarters to meet its guidance—the top end appears to be a rather tall ask, it highlighted. FY24E EBIT margin guidance has been also trimmed to 20–22 percent (from 21–22 percent in FY23). The mid-point of the guidance will be the same as the FY23 exit margin—indicating significant cost pressures the company expects from wage hikes and lower growth, noted Nuvama.

"While Q4 results are disappointing, we view it and the lower FY24 guidance as a manifestation of the overall weak macros, which might keep Infosys – and other IT stocks – under pressure in the near term. Over the medium-to-long term though, we expect Infosys to benefit from the strong demand environment," it said.

Phillip Capital

The brokerage also maintained its ‘buy’ call on the stock with a target price of ₹1,590, indicating an upside of 14 percent. Post initial reaction, we believe the risk-reward will become favorable given Infosys has underperformed Nifty IT by 7 percent in the last three months and valuations are below its five-year median 1-year forward PE (22x), noted the brokerage.

"Considering weak exit to FY23, the ask rate for FY24 is at +1.6 percent to +2.7 percent CQGR for the next four quarters, implying pickup in growth from Q1. Given the uncertain environment in the near term, growth can be back-ended for Infosys, in our view. We believe the stock can remain under pressure in the near term until clarity emerges on growth," it stated.

The brokerage cut its FY24/25 PAT estimates by 5-6 percent on a sharp miss in Q4. It is now forecasting dollar revenue growth of 6/11 percent with 21.5 percent/21.5 percent EBIT Margins in FY24/25, respectively.

Motilal Oswal

The brokerage has also maintained its ‘buy’ call but cut Infosys' target and estimates post its Q4 results. Its new target of ₹1,520 indicates a potential upside of 10 percent. Meanwhile, MOSL lowered its FY24/FY25 EPS estimates by 4/5 percent to factor in the Q4 miss and FY24 guidance.

"We expect the big revenue miss and elevated uncertainty to adversely impact the stock’s short-term performance, resulting in a negative reaction from high single to low double-digit, on account of the disappointment. The weak topline performance should prevent the company from benefitting from the easing supply environment, and we expect FY24 EBIT margins at 21.1 percent, flat YoY. This in turn should result in FY24 rupee PAT growth in single digits at 9.3 percent YoY, despite tailwinds from cross-currency and INR depreciation," it predicted.

MOSL expects FY24 revenue growth to be around 5.2 percent YoY in CC terms, which is near the lower end of the guidance band, as it takes time for the mega deal opportunities to convert into orders and revenues. The delay in revenue growth will likely push the recovery for Infosys to FY25, once the demand environment becomes more favorable.

Source: MOSL

First Published: 17 Apr 2023, 02:04 PM IST