Global brokerage house Goldman Sachs believes while revenue growth for IT companies is likely to stay muted in the near term on the back of macro concerns, the market is underappreciating the recovery and upside from FY25.

IT sector: Market underappreciating recovery, says GS; initiates coverage on six top stocks including TCS

TL;DR.

Goldman Sachs believes that revenue growth for Indian IT companies may be muted in the near term due to macro concerns. However, the brokerage sees potential for recovery and upside from FY25 and has initiated coverage on six Indian IT stocks.

In a recent note, the brokerage initiated coverage on six Indian IT stocks and said it expects the sector to see growth amid tailwinds from Generative AI and pent-up demand.

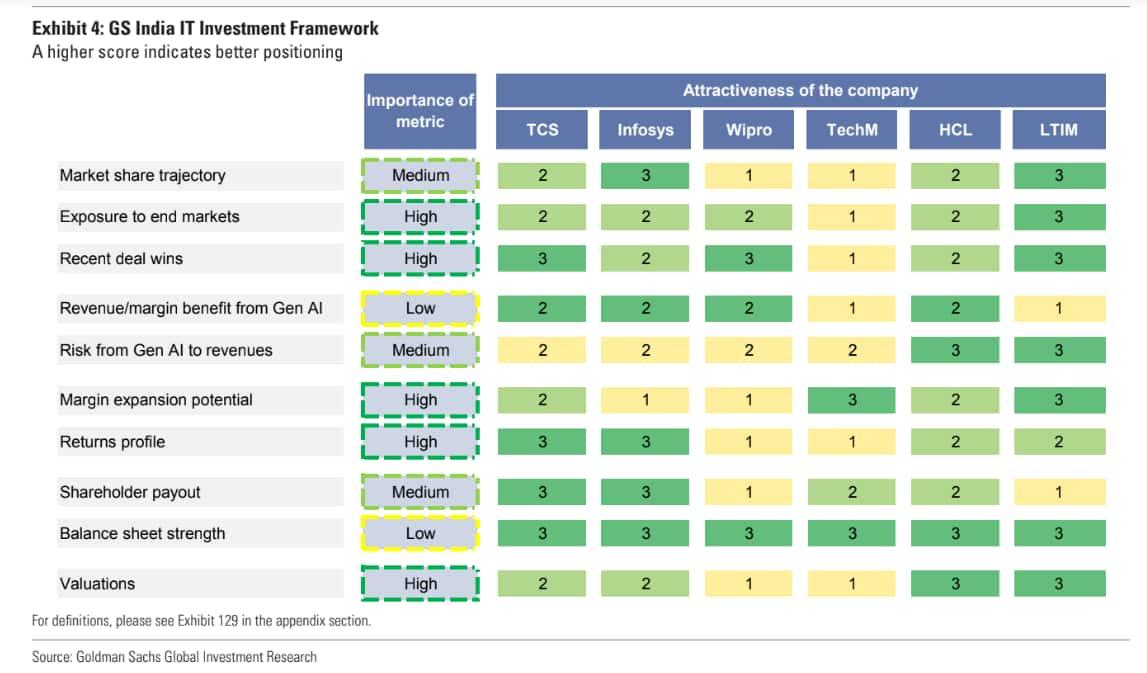

It has ‘buy’ calls on 3 stocks - Tata Consultancy Services (TCS), Infosys, and LTIMindtree, ‘sell’ ratings on 2 - Wipro and Tech Mahindra, and a ‘neutral’ rating on HCL Technologies.

After two years of strong revenue growth in FY21 and FY22, growth in recent quarters has slowed down for IT. Despite the recent correction, the brokerage noted that the valuations for IT services companies are at a premium compared to their last 10Y average, despite broadly similar growth outlook vs. history.

The brokerage sees three reasons why these higher valuations are justified: (1) the market now views tech/IT spends as a lot more resilient, and less susceptible to disruptions, as proven by IT services companies through various cycles, warranting a higher multiple vs. history; (2) payout ratio, as defined by total shareholder payout upon net income, has significantly improved for India IT over the last 10 years, from 30-40 percent earlier, to 90-100 percent now; and (3) overall index (Nifty 50) multiple has also gone up during this period, and the premium of IT services coverage vs. Nifty 50 is broadly in line with the historical average.

The brokerage has forecasted a 9-10 percent annual revenue growth for Indian IT coverage from FY25, which is a 2x multiplier of the 5 percent revenue growth for GS-covered global companies in CY24. “While our overall sector revenue growth is in line with consensus, it sees company-specific divergence and is ahead of consensus on Infosys and TCS,” said the brokerage.

"In our view, this growth will be aided by the pent-up demand (order book has remained robust), initial tailwinds from Generative AI (our differentiated analysis suggests IT Services companies playing a meaningful role in enterprise integration), and continued shift to cloud and managed services (cloud penetration is only 30 percent). Indian IT Services companies have doubled their market share in the last 10 years (to 6.2 percent of the global IT spending in CY22), and given the structural advantages of a large, skilled and low-cost workforce, coupled with a diversified geographical footprint, we expect Indian IT firms to continue gaining share," it explained.

The brokerage also expects the operating profit growth, at 12-15 percent over FY25-26E, to be faster than revenue growth, driven by the presence of multiple margin levers and forecasts an expansion in margins for all the companies within its coverage.

Let's see what it has to say about the 6 IT stocks it has initiated coverage on:

LTIMindtree: The brokerage has a ‘buy’ call on the stock with a target price of ₹6,310, indicating an upside of over 23 percent from its current market price (CMP) of ₹5,123.25. The stock has risen 19 percent in 2023 YTD and 15 percent in the last 1 year. In the long term, 3 years, it has given multibagger returns, surging 105 percent.

The brokerage is bullish on the stock as it has the fastest growth within the coverage driven by cross-selling to existing accounts and the highest margin expansion potential due to merger synergies. It expects a 17 percent and 15 percent FY23-25E EBIT and PAT CAGR and is 1-3 percent ahead of consensus on FY24-26E EBIT. The brokerage estimates revenues to grow 7.3 percent and 12.5 percent YoY in CC (constant currency) terms in FY24 and FY25. It also sees the margin improving by 175 bps over FY23-25, one of the highest within its coverage, driven by cost synergies, improving operational levers such as attrition, pyramid rationalisation, and operating leverage.

"We initiate with a Buy rating on LTIMindtree, as we believe the company is well-poised to deliver sector-leading growth, on account of (i) higher cross-selling/upselling opportunities from the recently concluded merger; and (ii) robust deal pipeline and execution capability. Key catalysts include large deal win announcements, higher client mining, improving near-term macro outlook (particularly in the US), realisation of cost synergies," it said.

Infosys: The brokerage has a ‘buy’ call on the stock with a target price of ₹1,600, implying a 12.6 percent upside from its CMP of ₹1,420.55. The stock has shed 6 percent and 3 percent, respectively, in 2023 YTD and in the last 1 year. Meanwhile, in the long term, 3 years, it has advanced 51 percent.

"Buy Infosys as even though we expect two more quarters of subdued revenue growth, a strong order book indicates sharp CY24 revenue recovery, which current valuations do not reflect; we are 2 percent/4 percent ahead of consensus on FY25/FY26 revenues/EBIT," it stated.

It sees Infosys as a beneficiary of recovery in discretionary spending starting CY24 leading to a sector-leading growth of 11 percent CC YoY in FY25. With expectations of improving growth in FY25, GS expects margins to expand, aided by operational levers such as improving utilisation, better employee pyramid structure, and lower subcontracting costs, among others. It forecasts 9 percent/9 percent FY23-25E EBIT/PAT CAGR.

TCS: The brokerage has a ‘buy’ call on the stock with a target price of ₹3,930, implying a 16 percent potential upside. The stock has risen 3.6 percent and 7.7 percent in 2023 YTD and in the last 1 year, respectively. Meanwhile, in the long run, 3 years, it has jumped 51 percent.

"We initiate with a Buy rating on TCS and view the company as a defensive play in a tough demand environment; we believe the company’s wide geographical presence and client base coupled with deep vertical expertise makes it well positioned for market share gains. While the Indian IT sector is seeing demand weakness on account of macro headwinds, TCS’ deal wins have remained strong, and we expect the company to benefit from vendor consolidation. We are 1 percent/2 percent ahead of consensus on FY26 revenues/EBIT," noted GS.

Tech Mahindra: The brokerage has initiated coverage on the stock with a ‘sell’ call and a target price of ₹1,010, indicating a 15 percent downside. The stock has gained over 17 percent both in 2023 YTD and in the last 1 year. It has also added 58 percent in the last 3 years.

"We initiate with a Sell rating on TechM given our expectation of the company continuing to lag India IT peers on both revenue growth and operating margins. We expect revenue growth to be weak (-1 percent in FY24E) given TechM’s relatively high exposure to the CME (Communication, Media and Entertainment) vertical, where we expect technology spending growth to remain muted. While we expect a gradual recovery in EBIT margins on the back of lower SG&A costs, subcontracting expenses, higher offshoring, and employee pyramid rationalization, our outer year estimates of 13 percent EBIT margin remain below medium/long-term management target of 14 percent and at the lower end of India IT peers, on the back of our lower than Street revenue estimates," it explained.

TechM is India’s fifth largest IT services company with $6.6 bn in revenues as of FY23, which GS expects to grow at 4 percent CAGR over FY23-FY25E. It also forecasts a 9 percent/7 percent FY23-25E EBIT/PAT CAGR.

Wipro: The brokerage has a ‘sell’ call on the stock with a target price of ₹385, indicating a 6 percent downside. The stock has added 4 percent in 2023 YTD and 1.2 percent in the last 1 year. Meanwhile, it has gained 50 percent in the past 3 years.

"We initiate with a Sell rating on Wipro as we believe its relatively high exposure to the consulting segment, which is seeing a greater impact of cuts in discretionary technology spend, coupled with sub-optimal execution, will lead to further market share erosion. We expect Wipro to grow at the slowest pace among India IT peers for the next 2 years, along with EBIT margins that remain below management’s medium/long-term target range and at the lower end of India IT peers. Wipro is trading in line with its 5-year historical valuation average and at about a 23 percent discount to the sector, marginally higher than its historical average. With weak near-term growth and margin profile, we expect the stock to underperform vs. peers," said GS.

HCL Tech: The brokerage has a ‘neutral’ recommendation on the stock with a target price of ₹1,160, implying a muted return going ahead.

"We initiate with a Neutral rating on HCL Tech as we expect macro headwinds in IT and business services segments, and a weak near-term demand outlook for ER&D (Engineering and R&D) to result in risk to near-term guidance. Further, we expect margin tailwinds (lower subcontracting expenses, and pyramid rationalization, among others) to be offset by the lower revenue growth, leading to a small margin contraction in FY24E, but improvement thereafter. Starting FY25, with the return of discretionary budgets, we expect to see a pick-up across both ER&D and IT Services business, with EBIT margins improving to 19 percent/19.2 percent in FY25/FY26E (18 percent in FY24), driving 11 percent FY23-25E EBIT CAGR. HCL’s FCF generation has also been strong, and we forecast FCF/Net Income of 110 percent over FY24E/FY25E, one of the highest within our India IT coverage," stated the brokerage.

HCL Tech is India’s third largest IT services company with US$12.6 bn in revenues as of FY23, which the brokerage expects to grow at 9 percent CAGR over FY23-FY25E. HCL Tech is currently trading at 19x 12m forward P/E, higher than its last 5-yr average of 17x; analysis suggests a balanced risk-reward, it added.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

Source: Goldman Sachs

First Published: 28 Aug 2023, 03:40 PM IST

Related Stories

markets

Wipro: This large-cap IT stock is down 43% from its all-time high; what lies ahead?

A Ksheerasagar