Domestic brokerage house Kotak Institutional Equities (Kotak) believes India's largest life insurer Life Insurance Corporation (LIC), which got listed in May last year, is likely to surge over 35 percent in just 1 year.

The brokerage has a 'buy' call on the stock with a target price of ₹1000, indicating a potential upside of as much as 36 percent from the current market price.

Kotak is bullish on the stock on the back of unparalleled dominance in the life insurance sector, cheap valuations, high market share, multifold jump in September quarter earnings, etc.

"We initiate coverage on LIC with a BUY rating and an FV of ₹1,000, reflecting 1.3X core EV December 2024E (2.1X to 3.2X for private peers) and a 50 percent haircut on unrealized equity gains," said Kotak.

As per the brokerage, LIC's margin expansion, driven by the shifting of the product mix by its unparalleled agency force, should boost the value of new business (VNB) growth, even as overall medium-term Annualized premium equivalent (APE) growth will likely to be lower than private peers. The large unrealized equity gains (59 percent of FY2022 EV) should also support LIC’s EV but make it leveraged to capital market movements, it added.

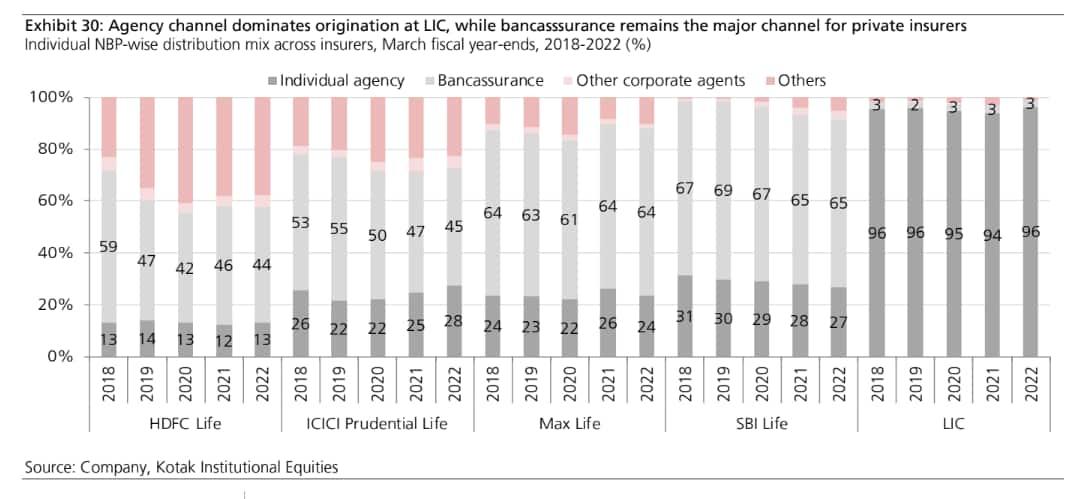

The brokerage further noted that LIC’s dominance is unparalleled in the Indian life insurance sector, with 37 percent APE market share in FY2022. The high productivity (15.4 policies/year per agent versus 0.9-4.2 policies/year of its private peers) of over 1.33 mn agents (54 percent of life insurance agents in India) remains the bedrock of LIC’s market dominance and cost leadership, it pointed out.

Kotak believes LIC’s valuations largely ignore its strengths.

Stock price trend

The stock performance of the life insurer was largely muted in the previous year. Since listing in May, the stock had given only 1.5 percent returns to its investors in 2022. The stock has been on a downward trend since listing. It lost 17 percent in June last year and has been volatile, swinging between gains and losses since then. However, the stock rose 5 percent in November and 7.5 percent in December 2022 after strong September quarter results. In January so far, the stock has also added 7 percent.

However, it is important to note that the stock has never once traded above its IPO price of ₹949.

Earnings

LIC reported a net profit of ₹15,952 crore for the quarter ended September (Q2FY23), a manifold increase from ₹1,433 crore in the corresponding period last year.

In the June quarter, the insurer reported a net profit of just ₹682.9 crore. First-year premium, an indication of business growth, came in at ₹9,124.7 crore for the quarter compared with ₹8,198.30 crore a year ago.

Net premium income was ₹1.32 lakh crore, compared with ₹1.04 lakh crore in the year-ago period.

Investment Rationale

Leader by a mile: As per the brokerage, LIC, despite ceding share to private players, has retained 37 percent market share in individual APE in FY2022. Its enormous agency franchise remains the cornerstone of its success, driving 96 percent of individual new business premium (NBP) in FY2022, Kotak highlighted. Moreover, the high productivity of its agency force, coupled with the benefits of scale, drives cost leadership, while listed private peers largely depend on banks to drive their business, it added. Kotak remains positive about LIC’s ability to steer the product mix to the high-margin, non-par segment from the large share of the participating business (29 percent of APE in FY2022).

Gradual margin expansion: Kotak expects LIC to deliver a VNB CAGR of 18 percent in FY2023-25E owing to an APE CAGR of 13 percent and 180 bps margin expansion. The bifurcation of funds led to a sharp increase in EV, a large part of which reflects unrealized gains in the equity book, thereby compressing RoEV (operating RoEV of 10 percent for FY2023-25E), noted Kotak.

Better economics for shareholders due to the 100 percent share in the non-par book and 10 percent (5 percent earlier) in the par book will likely support high growth in earnings ( ₹25800 crore in FY2025E versus ₹4100 crore in FY2022), it explained.

Key risks: Key risks to LIC’s business stem from competition from private players that have a more diversified product mix and sourcing. A correction in the equity market can pose a significant risk to EV because of its large equity investment book, especially in the non-participating segment, said the brokerage.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.