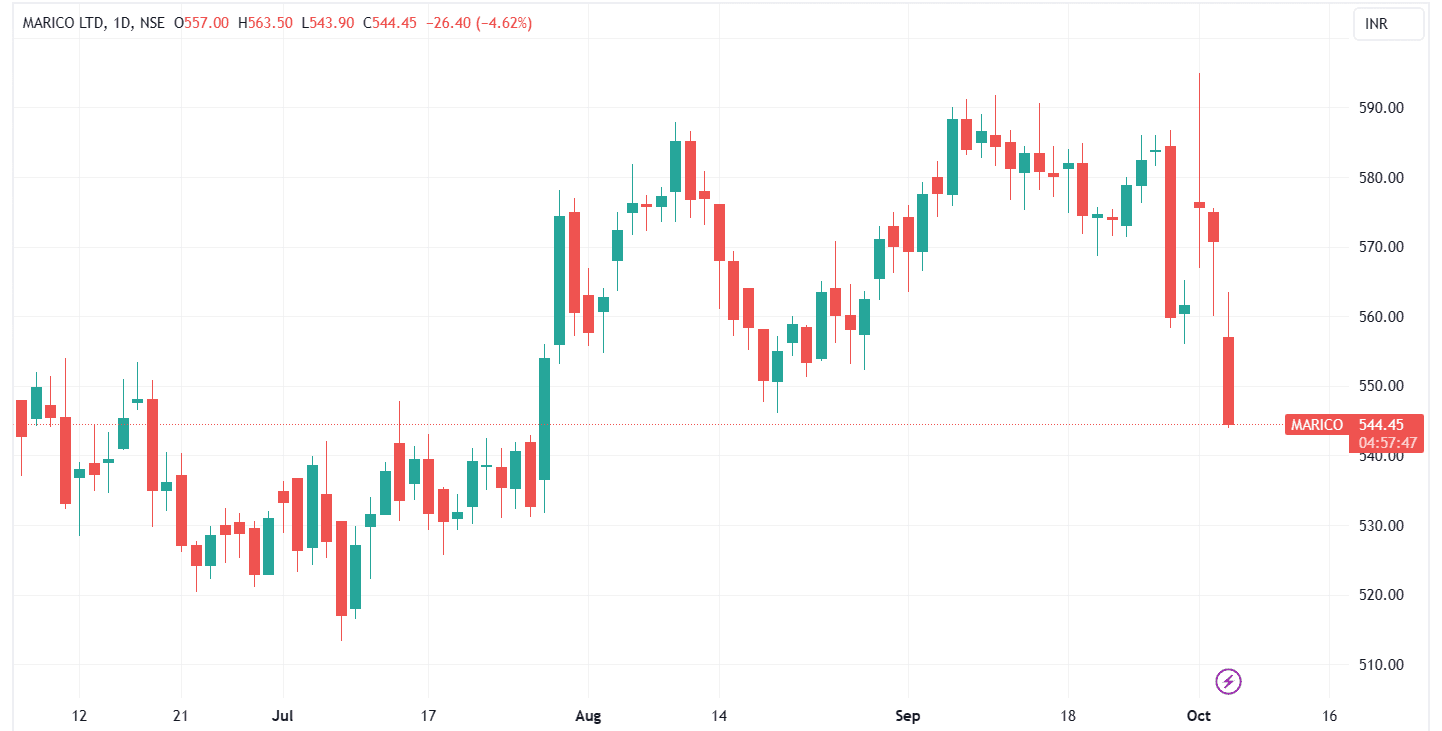

Shares of Marico, one of India’s leading consumer products companies in the global beauty and wellness space, slumped 4.7% to ₹543.90 apiece in Thursday's trade following the company's weak Q2FY24 update.

The company's domestic volumes in Q2FY24 grew in low single digits on a year-on-year basis, with low single-digit volume growth in Parachute Coconut Oil and Saffola Edible Oils, along with low single-digit value growth in Value Added Hair Oils.

"During the quarter, demand trends largely mirrored the trends observed in the preceding quarter. Instances of rising food prices and below-normal rainfall distribution in some regions seemed to impede the anticipated recovery in rural demand," the company said in an exchange filing.

However, the company continued to witness healthy trends in offtakes, market share and penetration across key franchises.

Its consolidated revenue was marginally lower on a year-on-year basis in Q2FY24, dragged by pricing corrections in key domestic portfolios over the last 12 months. Marico expects these pricing corrections to gradually factor into the base in the coming periods.

Additionally, currency depreciation in some of the overseas markets also affected the reported INR growth in international business, it added.

Marico anticipates robust gross margin expansion on a year-on-year basis. It significantly increased advertising and promotion (A&P) spending to strategically strengthen its core and new product categories. It expects healthy operating profit margin expansion, leading to low double-digit operating profit growth.

Looking ahead, Marico expects to maintain an improving trend across key performance parameters in H2, supported by a gradual pickup in volume and topline growth in the domestic business and healthy momentum in the international business.

The company maintains its aspiration of delivering sustainable and profitable volume-led growth over the medium term, enabled by the strengthening brand equity of its core franchises and the scale-up of new engines of growth.

For the June-ending quarter (Q1FY24), the company reported a 15.64% rise in its consolidated net profit to ₹436 crore, led by a one-time gain from the sale of fixed assets. However, its revenue from operations dropped 3.16% YoY to ₹2,477 crore in Q1FY24.

The company's revenue from the domestic market slipped 4.89% YoY to ₹1,827 crore, while revenue from the international business increased by 2% to ₹650 crore against ₹637 crore a year ago.

38 analysts polled by MintGenie on average have a 'buy' call on the stock.

Disclaimer: We advise investors to check with certified experts before taking any investment decisions.