Global brokerage house Morgan Stanley, in a recent report noted that Indian stock markets are likely to remain under pressure due to recovery in emerging markets (EMs) but it expects absolute returns to improve.

“We remain underweight India in an EM context given our view on improving conditions for some large EMs such as China, Korea and Taiwan. We believe EMs are benefiting from a relatively more benign world versus 2022, and India’s relative valuations imply that its recent underperformance may continue for a few more weeks. India’s relative fundamentals in terms of earnings growth remain strong,” Morgan Stanley said.

At the helm of India’s outperformance in 2022, the brokerage report noted was government policy, including a structural rise in the domestic equity saving pool, a boost to corporate profit share in the gross domestic product (GDP) and a focus on foreign direct investment (FDI) flows, which raised the share of FDI in the balance of payments (BoP), allowing India to run monetary policy that is less sensitive to the US Fed,and reduced the equity market’s sensitivity to US growth conditions and oil prices.

Not much of that has changed in 2023 and relative valuations, a sore point for India’s relative performance, are also correcting rapidly, highlighted MS.

Sensex targets

The brokerage has a Sensex target of 68,500 implying an upside potential of 13 percent to December 2023. This level suggests that the BSE Sensex will trade at a trailing P/E multiple of 20.5x, ahead of the 25-year average of 20x. The premium over the historical average reflects greater confidence in medium-term growth.

This is the base case scenario, which has a 50 percent probability, as per MS. In this case, it assumes no major up move in commodity prices, especially oil and fertilizer (either due to China reopening or the conflict in Ukraine), stable domestic growth as per forecasts, the US does not slip into a recession, RBI exits at 6.5 percent repo and government policy remains supportive via strong infrastructure spending. Sensex earnings compounded 22 percent annually through FY25E.

Meanwhile, in the bull case scenario, which has a 30 percent probability, the brokerage has a Sensex target of 80,000.

Assumptions: In addition to the above, India is included in the global bond indices, resulting in nearly $20 billion of inflows over the 12 months, the market starts pricing a majority government in 2024 and the equity limit for retirement funds is hiked to 25 percent. Earnings growth compounds 25 percent annually over F2022-25E.

Finally, in the bear case scenario, which has a probability of 20 percent, the brokerage has given a Sensex target of 52,000.

Assumptions: Commodity prices rise, and the RBI ends up taking the repo rate beyond 7 percent to protect macro stability, a protracted recession in the developed world drags down India’s growth, and the market starts believing that India will vote in a minority government in 2024 and a sharp drawdown in shares rattles domestic flows. Sensex earnings compound 18 percent annually over F2022-25E, but equity multiples de-rate to reflect poor macro conditions.

Key catalysts

As per the brokerage, the most important catalyst is the market’s view on the 2024 general election outcome, which will come into play in the second half of 2023.

The interest rate cycle both home (the peak is likely behind us) and abroad, the strength of the earnings cycle (India is 10 percent ahead of the consensus for F2024), the impact of China reopening, especially on input prices and energy costs, and the likely increase in the institutional bid on shares are some of the other key factors that will decide the markets' trajectory going ahead.

The brokerage believes that strong earnings growth going ahead is likely to be driven by improving capex and margins.

“Stock returns lead earnings growth and are suggesting over 20 percent EPS growth in the coming 12 months, similar to our estimates. Our FY24 earnings estimate is 10 percent ahead of consensus. A key risk is a larger-than-expected slowdown in global growth,” the report said.

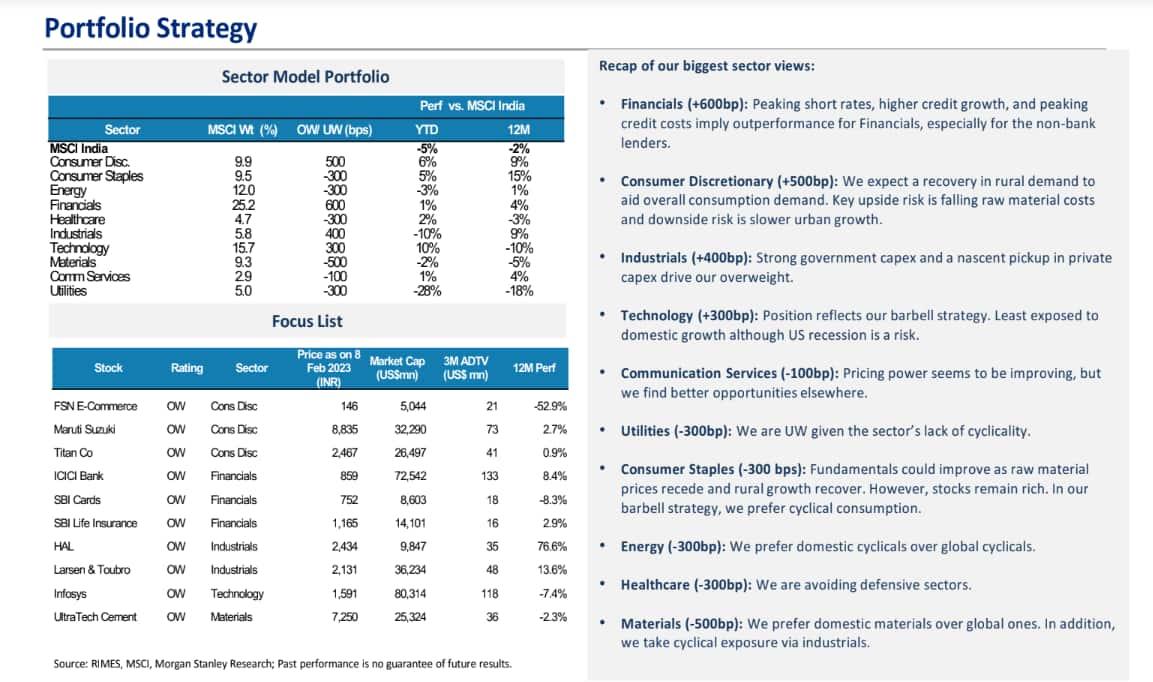

Portfolio Strategy

The brokerage said that its portfolio strategy includes barbell sector positions with a cyclical bias, a preference for the broad market and stock picking over large caps and macro investing.

"Stock picking > macro investing, Cyclicals > Defensives, SMID > Large-caps. Correlations across stocks are well off lows, so the market is transitioning to a stock pickers’ one," suggested MS.

It is overweight on Financials, Technology, Consumer Discretionary and Industrials and underweight on all other sectors.

Its top picks include Nykaa, Maruti Suzuki, Titan, ICICI Bank,SBI Cards, SBI Life, HAL, L&T, Infosys and Ultratech Cement.