In light of the Reserve Bank of India's (RBI) caution on NBFCs’ (non-banking finance companies) elevated reliance on bank funding and a further increase in yields, global brokerage house Nomura has analysed the different trends that will impact the sector going ahead and listed the stocks that will benefit from them.

Nomura's analysis of rates and liability mix of NBFCs shows that cost of funds (CoF) should peak out by the third quarter of FY24 (Q1FY24), after rising 30-40 bps from the first quarter of FY24. This quantum of increase is higher than the guidance given by most of the NBFCs. Further, the benefit of policy rate cuts, if any, on the cost of funds for NBFCs, should be visible only in H2FY25, noted the brokerage.

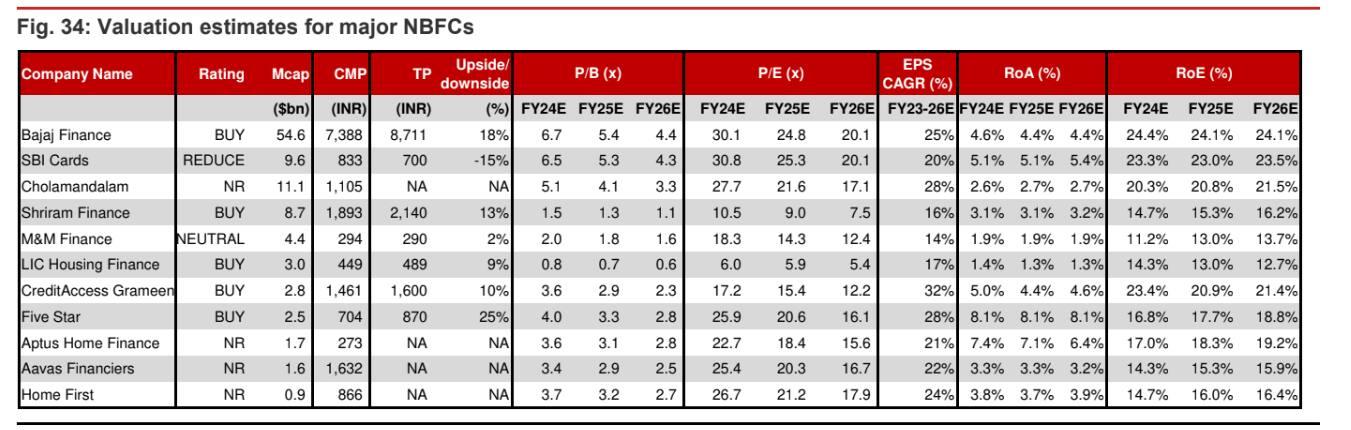

It believes SBI Cards, Five Star, and CreditAccess Grameen should benefit the most in a declining rate cycle but expects LIC Housing Finance to be negatively impacted the most.

Key trends to watch out for:

NBFCs’ reliance on bank funding remains at elevated levels: As of FY23, bank funding to NBFCs and HFCs (housing finance companies) constituted 57 percent and 44 percent of their total borrowings, said Nomura. Further, it noted that bank loans to NBFCs and HFCs have almost tripled to ₹13.7 lakh crore in July 2023 at a CAGR of 21 percent vs. 12 percent for overall bank credit, with PSU banks having 65 percent market share in it. It also pointed out that bank funding to NBFCs and HFCs reached 64 percent of their net worth in Q1FY24 vs 35 percent in FY17 and it expects NBFCs’ reliance on bank funding to come down in coming quarters, driven by a pickup in alternate sources of funding.

Increase in CoF for NBFCs has been lower than broader increase in interest rates: Nomura pointed out that during Q4FY22-Q1FY24, when repo/1Y T-bill/1Y Corp AAA yield inched up by 250 bps/242 bps/248 bps, most of the NBFCs/HFCs barring Cholamandalam Invest and SBI Cards, saw less than 100 bps increase in funding cost vs an over 100 bps increase for large banks. Compared to the CoF of Q3FY19, when the policy rate was at a similar level of 6.5 percent, the cost of funds for NBFCs is still lower by up to 200 bps, it informed. Hence, the brokerage believes it is quite evident that repricing of NBFC liabilities is still underway, as it happens with a lag both in the upward and downward rate cycles.

Cost of funds to likely peak out in Q3FY24: The brokerage expects CoF for NBFCs could rise another 30-40 bps from Q1FY24 before peaking out in Q3FY24. This increase would be driven by 1) another 10-15 bps increase in yields across buckets since Q1FY24; 2) a further increase in cost of NCDs, as coupon rates for maturing NCDs in remaining FY24/25 (25-50 percent of Q1FY24 outstanding NCDs) are 100-200bp lower than current yield; and 3) MCLR-linked bank loans are still getting repriced upwards due to a lag, explained Nomura. This CoF increase of 30-40 bps during Q1FY24-Q3FY24 is higher than the guidance given by most of the NBFCs and the average 20 bps increase is built into current estimates. Hence, there could be a 1-5 percent risk to FY24F EPS coming from pressure on CoF, Nomura warned.

Benefits of potential policy rate cut in H1FY25 to accrue only in H2FY25: The brokerage expects the benefit of any policy rate cut in 1HFY25 on the funding cost of NBFCs to accrue only in H2FY25. Bank funding forms over 50 percent of the NBFC liability side. While repo/T-bill linked bank borrowings will get repriced downward immediately, it will take time for MCLR-linked bank borrowings to reprice downward as well, it noted. Further, it estimates that 60 percent of a repo rate change gets transmitted into MCLR. On the bond side, NCDs maturing even in FY25 has lower coupon rate compared to the current yield which is already factoring in repo cuts, added Nomura.

Stocks

Only from funding cost and spread perspective keeping other things constant, SBI Cards (Reduce rating), Five Star (Buy rating) and CreditAccess Grameen (Buy rating) should benefit the most in a declining rate cycle as only 23 percent, 27 percent, and 40 percent of their borrowings, respectively, are fixed, while the entire loan book is fixed in nature. It also expects LIC HF (Buy rating) to be negatively impacted the most, as 43 percent of its borrowings and 99 percent of its loans are floating in nature. “Having said that, the cost of funds is only one of many factors we look at to arrive at our rating on various stocks,” it informed.

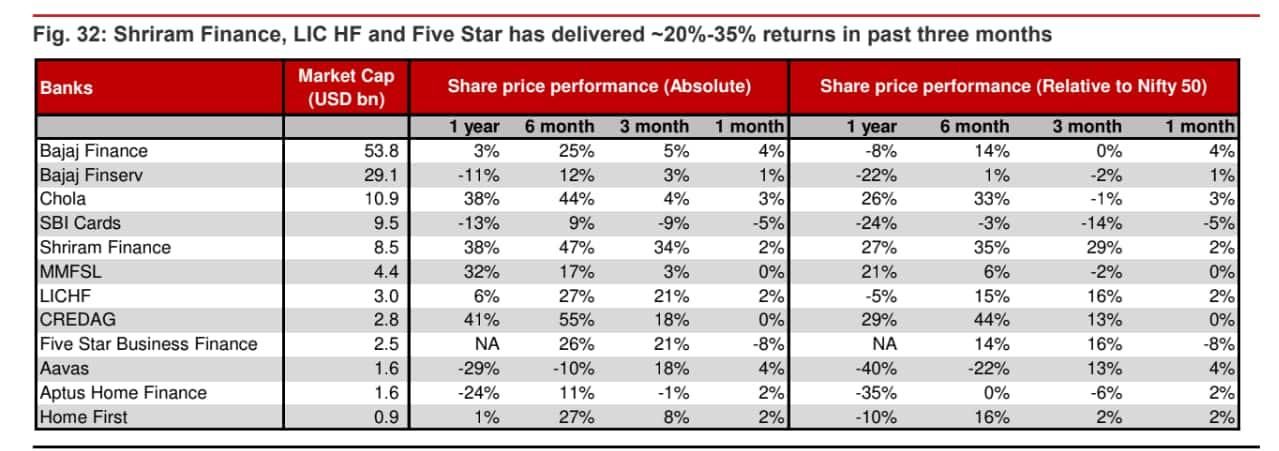

Among these 4 stocks, CreditAccess has surged the most in the last 6 months, 55 percent, followed by Five Star, up 26 percent and SBI Cards, up just 9 percent. LIC HF also jumped 27 percent in this period. Similarly in the last 1 year, CreditAccess has risen the most, up 41 percent, while LIC HF added 6 percent, however, SBI Cards shed 13 percent. Five Star, meanwhile, was not listed till a year ago.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie. We advise investors to check with certified experts before making any investment decisions.