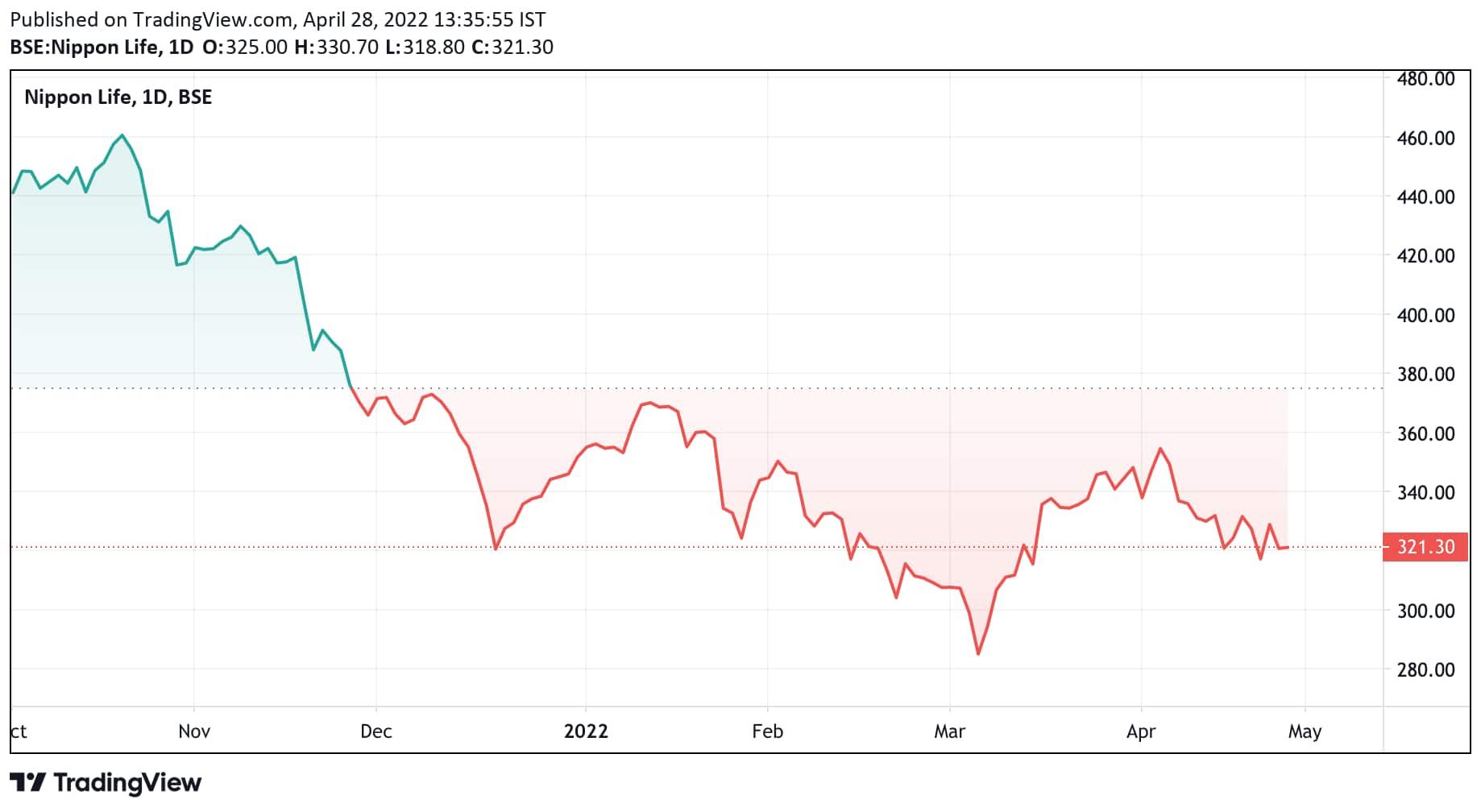

Shares of Nippon Life India Asset Management (Nippon Life India AMC) have been under pressure of late, falling about 33 percent from their 52-week high of ₹476.50 that it hit on October 19, 2021, on BSE.

The company released its March quarter scorecard after market hours on April 26 and the stock fell 2.46 percent in the next session on April 27 even as most brokerages have retained their positive views on the stock. On April 28, the stock closed 0.03 percent lower at ₹320.85.

The company's Q4FY22 consolidated PAT came at ₹174.85 crore, up 5 percent year-on-year (YoY), against ₹166.51 crore in the corresponding quarter of the previous financial year.

Revenue from operations for the March quarter of FY22 came at ₹337.97 crore, up 12 percent from ₹301.90 crore reported for Q4FY21.

Brokerages upbeat

Global brokerage firm CLSA has maintained its 'buy' rating on the stock with a target price of ₹460, implying a 40 percent upside, and underscored that the company beat its operating profit estimate by more than 5 percent as revenue was flat quarter-on-quarter (QoQ) despite fewer days (2-3 percent impact). Net profit was in-line with estimates due to lower than expected other income.

CLSA added that the company's management guided for opex to remain largely sustainable at current levels but indicated it had enough cost flexibility given the high operating leverage of the business.

Nippon AMC declared a dividend of ₹11 per share for FY22 including a ₹3.5 per share interim dividend and a final dividend of ₹7.5 per share implying a 96 percent overall payout for FY22, which is higher than the 75-77 percent dividend payout of the last two-three years, CLSA observed.

The global brokerage firm highlighted that the company's management will endeavour to keep the dividend payout at nearly 100 percent, against its earlier assumption of a 75 percent payout for FY23/24CL, which implies an attractive dividend yield of 4-4.5 percent for FY23-24CL.

"Our positive stance on Nippon AMC is premised on: stabilising market share, industry tailwinds with steady SIP flows, its improving equity scheme performance and inexpensive valuation. We now also highlight an attractive dividend yield of 4-4.5 percent. We largely retain our estimates but take up our dividend payout assumption to be in line with management’s guidance," said CLSA.

Brokerage firm Phillip Capital also has maintained a 'buy' call on the stock with a target price of ₹450. The brokerage underscored with all the levers in its place such as improvement in fund performance, gaining incremental share in new folios, and strong retail presence, the management expects the market share in SIP and equity to also start increasing.

"As the company has witnessed strong recovery in AUM post rebranding, we see operating leverage to provide significant scope for RoE improvement. Improvement in funds’ performance should stabilise equity market share in the coming quarters. At the current price, the stock trades at a P/E of 26 times/22 times for FY23/FY24 earnings," said Phillip Capital.

Brokerage firm JM Financial has a 'buy' call on the stock with a target price of ₹435.

"We believe the stock’s price performance is contingent on: (a) company’s market share gains/losses, and (b) sustained improvement in core operating performance. We believe unless the industry witnesses further acceleration of outflows/cancellation of SIPs, there is a limited downside to the stock price and we remain constructive over the medium term," said JM Financial.

An average of 14 analysts polled by MintGenie have a ‘strong buy’ call on the stock.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of Mint Genie.