Nifty IT has outperformed Nifty in 2023 YTD, underperforming by ~30 percent in 2022. The IT index has advanced over 14 percent this year so far as against an 8.6 percent jump in benchmark Nifty. Meanwhile, in the last 1 month as well, the Nifty IT index has risen 5.5 percent versus a 2 percent gain in Nifty.

Nirmal Bang ‘underweight’ on IT sector but upgrades Tech Mahindra; here's why

TL;DR.

Nifty IT has outperformed Nifty in 2023 YTD but brokerage house Nirmal Bang remains ‘underweight’ on the Indian IT sector. It has upgraded Tech Mahindra to 'Accumulate' due to expected margin expansion in FY26.

Despite the recent outperformance, brokerage house Nirmal Bang remains 'underweight' on the Indian IT. It has also cut FY25 estimates for this space.

"We believe the market is taking the view that the worst is over and that revenue/earnings will accelerate sharply in FY25. We have a non-consensus view that FY25 growth is going to be only a tad faster than FY24 with risks that it could be as bad or weaker. While the US macro has surprised positively in 2023 so far, deterioration is likely ahead in 2024. Demand is likely to be slower for longer," said the brokerage.

Stocks

While the brokerage has a SELL recommendation on most IT stocks in its our coverage, it has upgraded Tech Mahindra to ‘Accumulate’ as it believes margin expansion in FY26 may surprise on the upside under a new management.

"While TML will see continued weakness in revenue and margins in the remaining quarters of FY24, it will also be impacted by the shallow US recession we are expecting in 2024. From the current extremely low levels, we believe that its EBIT margin could expand a lot faster than current consensus expectations. From 10.2 percent EBIT margin in FY24E, we are expecting the same to expand to 15.4 percent in FY26. We do not think this by any means is an aggressive target as this was already achieved in FY19. For FY24, we have raised our EBIT margin estimate by 60bps. For FY25, as has been the case with other companies under our coverage, we have cut our USD revenue estimate by ~300bps while raising our EBIT margin estimate by 30bps. It is for FY26 that we have raised our EBIT margin estimate substantially by 210bps to 15.4% while keeping USD revenue constant," it explained.

Having upgraded TML numbers, it believes this situation is going to likely play out over the next 18 months plus and not immediately. The brokerage sees weak numbers from the company (especially margins which are going to be significantly below peers) in the coming quarters too.

In terms of PE multiples, TCS continues to be its sector benchmark as it has the strongest position in the industry due to: (1) Breadth and depth in service lines, geographies, and verticals (2) the ability to stitch together integrated offerings (3) Significant lead in automation skills (4) Strong and stable base of experienced employees with contextual knowledge (5) Strong product, platform and agile delivery capabilities and (6) Industry-best margins and return ratios. It expects TCS to gain market share in the medium to long term, driven by its strong capabilities, although its pace of market share gain will slow due to its size.

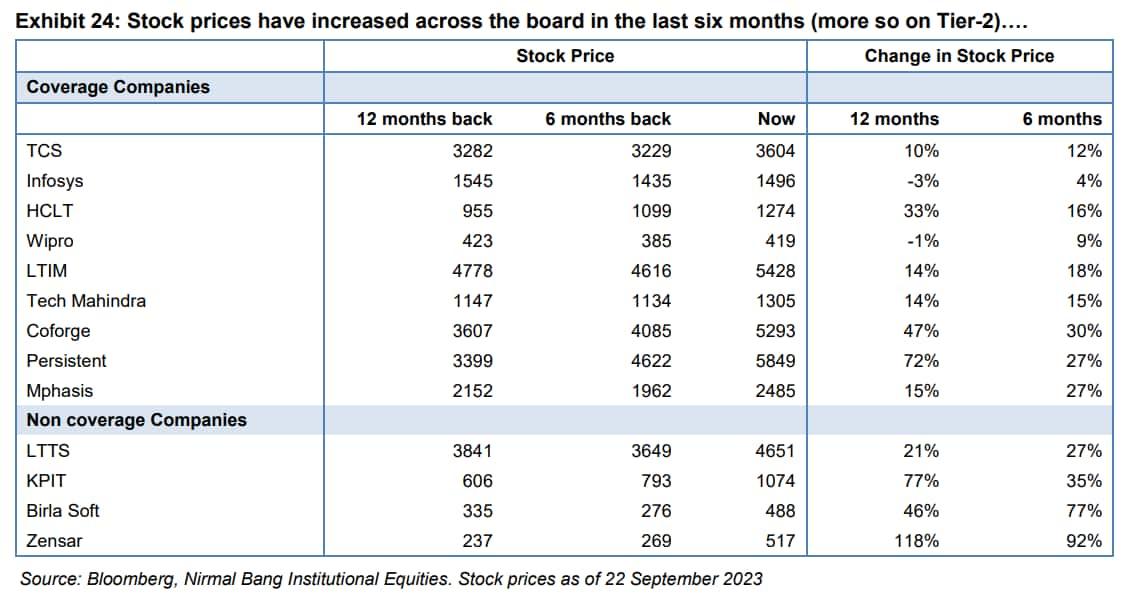

Tier 2 valuations

After a sharp dip in stock prices in 2022, a sharp rebound has been seen in Tier-2 stocks, especially in the last six months with multiples almost back to the peaks seen in 2H2021.

"We are surprised by the kind of expansion in the multiples the market has accorded to these companies. While we have always stated that well-managed Tier-2 companies will outgrow Tier-1 set, we have also stated that the big earnings gap that existed during FY21-FY23 between the two in favor of Tier-2 is unlikely to remain the same. We think the revenue growth gap will contract and margins at best will remain flat," said the brokerage.

Nirmal Bang fears that the Indian Tier-2 set would suffer more because of vendor consolidation under the pressured profit picture for customers, a less diversified revenue mix, which could throw up negative growth surprises and a larger exposure to non-Global 1000 clientele, whose profits are more vulnerable in the current macro environment. Indian Tier-2 IT set is now at a PE premium of 38 percent to Tier-1 (peak of 60 percent in November 2021 and recent low of 10 percent in January 2023). It traded at a discount of 14 percent on 1st January 2020, informed the brokerage.

The high PE multiples are also a reflection of the market’s view that some Tier-2 IT companies will become US$5-10bn enterprises in the next 10-20 years. Once the ‘Digital’ high tide recedes, it remains to be seen which of the current Tier-2 set will continue to show promise. In the initial phase of any new tech cycle, customers tend to be open to new vendors, but as the cycle matures (post FY23 in our view), vendors that have scale – Tier-1 - tend to do better. “We think customers are looking for revolutionary transformation, which Tier-1 companies with multi-vertical exposure and deeper domain/technology skills are best placed to deliver,” it stated.

Source: Nirmal Bang

Reasons for ‘underweight’ stance

- The brokerage noted that while the IT sector has seen PE multiple expansion (especially for Tier-2) in the last 6/12 months, there have been no meaningful earnings upgrades.

- Further, post two successive quarters of weak results (in aggregate), it believes that Q2FY24 and Q3FY24 may see QoQ growth for its coverage universe, but the next couple of quarters’ performance will not herald the beginning of a sustained pick-up.

- Also, macro uncertainty has led to weak spending by customers. That uncertainty, it believes, has accentuated over 2023 if one looks at broader data points than just the US real GDP growth. The US’ resilience has been driven by consumers and a higher fiscal deficit. Europe and China seem to be in a soft patch of their own, the brokerage stated.

- Over the last 12 months, while order pipeline/inflow has been good, growth has been weak due to weak discretionary spend, weak revenue conversion of TCV won, and compression of the existing book of business (with low visibility to the external world). Nirmal Bang believes the next phase of weakness in 2024 will likely see pipeline/TCV compression with more generalised pricing pressure.

- A look at enterprise health across both the US as well as Europe points to improvement, especially since June 2023. It sees a mixed picture at the sub-indices level, but believes that consensus will cut estimates in 2024 as it did in 2022/2023

- Downward guidance revisions by multiple players (some despite a robust 1H2023) in the last three months imply a weak 2H2023 in aggregate. There has not been much commentary on 2024, although a few are hopeful of an upturn.

- On margins, the brokerage disagrees with the consensus that they will improve over FY24-FY26. The mega deals are fiercely competed (‘priced to win’) and are dilutive not only in initial years but are dependent on the extraction of significant productivity gains and operational efficiencies, where companies may fall short, noted the brokerage.

Outlook

Beyond FY23, the brokerage sees customers shifting from the current democratic ‘skills/capability’ focused vendor model to a more discriminating one based on ‘ability-to-deliver’ (1) cost takeouts and (2) business model changes - in that order. It is here that one will see a divergence in growth and valuation. Incrementally, risks are to the downside from both valuation as well as fundamental perspectives. It favours Tier-1 IT companies vs. Tier-2.

“We persist with our 18-month-old ‘UW’ stance. This is because (1) we believe that a conclusive Fed pivot is likely only when US core inflation falls to 2 percent, which we think is unlikely in the next six months. Financial stress/accident-related stopping/easing of current hawkish monetary policy could induce a short-term rally that may not be sustainable (2) consensus earnings estimates for FY25 continue to be too high and seem to implicitly assume a soft/no landing for the US economy. We are explicitly pricing in a shallow recession sometime in 2024. (3) even if one were to ignore the next 12–18 months’ risks around recession and take a 5-year view, we believe that starting valuations are expensive and can at best deliver mid to high single-digit total stock returns for TCS/Infosys,” explained the brokerage. It added that structural revenue/earnings growth is being overestimated by the street.

It also believes that USD revenue growth over a 5-year period (FY23-FY28) for Tier-1 set in aggregate will at best be at par with the FY15-FY20 period (7 percent) whereas peers believe it will be 300-500bps higher. “We also expect margins for most companies to remain in a narrow band at around FY24 levels and not see a material expansion,” added the brokerage.

The brokerage expects that the big pent-up demand-driven spike will be in FY26 and not in FY25. Hence, the expectation of double-digit growth in FY26 for Tier-1. Post that spike, it estimates that Tier-1 players will likely settle into a 7-8 percent CAGR for the foreseeable future.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie. We advise investors to check with certified experts before taking any investment decisions.

source: Nirmal Bang

First Published: 28 Sep 2023, 09:11 AM IST

Related Stories

markets

Wipro: This large-cap IT stock is down 43% from its all-time high; what lies ahead?

A Ksheerasagarmarkets

10 small cap IT stocks returned up to 150% in the last six months; do you own any?

A Ksheerasagar