On the back of the listing of demerged entity of Reliance Industries, Jio Financial Services (JFS), shares of NBFC major Bajaj Finance (BAF) have given flat but negative returns in August so far, snapping gains after 4 straight months.

The stock has shed a little over half a percent in August so far after rallying 30 percent in 4 months between April and July. It has gained a little over 10 percent in 2023 YTD and is up 2.5 percent in the last 1 year.

However, despite a volatile August, global brokerage house Nomura has maintained its bullish view on the stock. It has initiated coverage with a ‘buy’ recommendation and a target price of ₹8,700, indicating an upside of 20 percent.

The brokerage believes that the concerns regarding JFS are overdone. The setting up of a successful unsecured business is relatively difficult for an NBFC, given low ticket size and inferior customer quality and JFS’s execution capabilities would only be clear in the medium term, it noted.

"Historically, BAF has always traded at a higher valuation than bank/NBFCs due to its consistent outperformance over the industry in terms of overall business growth and profitability. BAF’s 1QFY24 numbers are strong on all parameters. Despite this, its stock has corrected by 6 percent in last one month, vs the Nifty 50's 1 percent decline over the same period, mainly due to fear of Jio Financials putting a dent on the core segments of BAF. As a result, BAF is currently trading at 5.2x/23.9x on FY25F BVPS/EPS. We find fears due to Jio Financials overdone at this point of time," it said.

After a decent debut, shares of JFS consistently hit 5 percent lower circuit for 4 straight sessions from August 21-24 on the back of profit booking. However, post that it rose a little. The stock listed at ₹265 on the BSE and ₹262 on the NSE, just a little higher than its discovered price of ₹261.85 after the special pre-open session held on July 20, 2023. Since listing, the stock has shed over 17 percent.

Estimates

Nomura expects BAF to deliver an AUM CAGR of 27 percent over FY23-26F, assuming an average NIM (net interest margin) of 10 percent and average credit cost of 1.6 percent, driving CAGRs of 25 percent for EPS (earnings per share), 4.5 percent for RoA (return on assets) and 24 percent for RoE (return on equity) over FY23-26F.

Investment Rationale

Consistently delivering strong numbers: The brokerage noted that Bajaj Finance continues to deliver strong numbers across the parameters. New product launches, maintaining a balance between secured and unsecured loans, and extensive usage of tech are a few of the key reasons for its sustained performance, it stated. BAF recently introduced new products, and plans to further expand its product lines including microfinance, and new car and tractor and gold loan financing. Nomura believes that these will provide support to its growth aspirations.

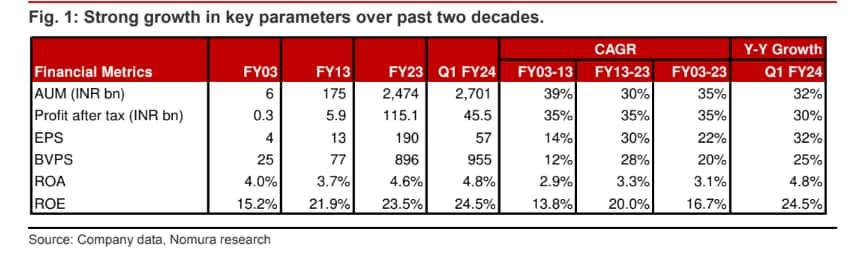

Golden past: BAF delivered AUM, PAT, EPS and BVPS CAGRs of 35 percent, 35 percent, 22 percent, and 20 percent, respectively, in the past two decades (FY03-23). Over FY13-23, the corresponding numbers were 30 percent, 35 percent, 30 percent, and 28 percent, informed Nomura.

"Despite maintaining such high growth, BAF’s asset quality has remained pristine except during the global financial crisis (GFC) when its gross non-performing assets (GNPA) reached as high as 16 percent in FY09 and credit cost reached 8 percent in FY10. After the shock, however, BAF has maintained all three key variables at consistent performance — high growth, high margins and lower credit cost which led to an average RoA/RoE of 3.3 percent/20 percent in the past decade (FY13-23). The lender has weathered multiple crises like the taper tantrum in FY13, demonetization in FY16, the infrastructure leasing and financial services (IL&FS) crisis in FY18, COVID-19 in FY21/22, etc. with much ease compared to other lenders in India," explained Nomura.

Well-diversified liabilities; exit of HDFC Limited (HDFC) positive for BAF: The brokerage pointed out that BAF has a well-diversified liability franchise, which, coupled with its AAA rating, strong parentage, prudent Asset and liability management (ALM) and robust track record, has led to declines in the gap of funding cost with large banks over the past few years. Further, after the exit of HDFC, all the exposure of HDFC to the financial system has been moved out of the non-banking financial companies/housing finance companies (NBFC/HFC) classification. This is a big positive for BAF and Bajaj Housing Finance (BHFL) from a liability-garnering and finer-pricing perspective, given the various regulatory caps on various liabilities streams for NBFCs/HFCs, it observed.

Risks: While the brokerage is bullish on BAF, its potential conversion into a bank due to size constraints is a key risk, as it would lead to declines in RoA/RoE along with a capped promoter stake and tenure of MD and CEO, it said. Also, the inability to scale-up new businesses such as MFI and new car/tractor financing, remain the key risk from a growth perspective, added Nomura.

Bajaj Finance has a diversified lending portfolio across retail, SMEs and commercial customers, with a significant presence in both rural and urban India. It accepts public and corporate deposits and offers a variety of financial services products to its customers.