Domestic brokerage house Prabhudas Lilladher (PL) expects benchmark Nifty to rise over 21 percent to 20,936 by September 2023. The brokerage estimates Nifty EPS (earnings per share) at 855.2 and 963.4 and introduces FY25 EPS at 1069.2. This shows a growth of 2.1 percent, 12.7 percent, and 11 percent for FY23, FY24 and FY25, respectively, noted PL.

It is important to note that Nifty is currently trading at 19x one-year forward PE which is a 7.8 percent discount to the 10-year average of 20.5.

In the Bull Case, the brokerage values Nifty at a 10 percent premium to the 10-year average PE (21.5x) and raise Nifty's Sept 2023 target to 22,918 from 22,063 earlier. Whereas in the Bear Case, it values Nifty at a 20 percent discount to the 10-year average and cut Nifty's Sept 2023 target to 15,800 from 16,046 earlier.

Navigate through near-term headwinds

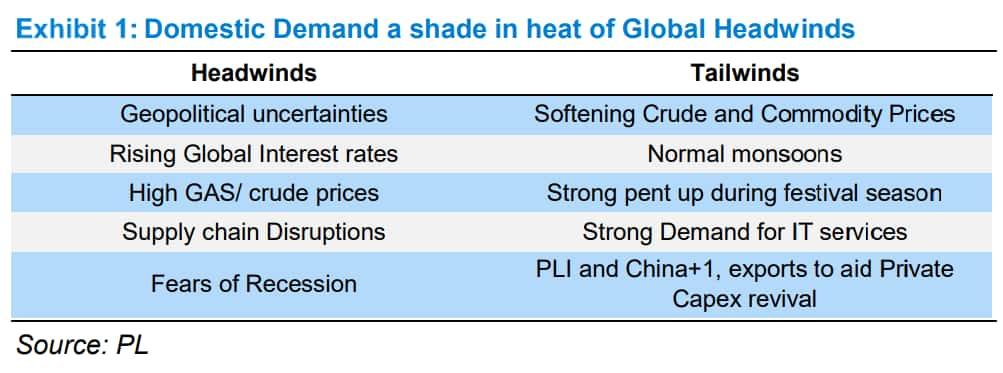

As per the brokerage, the Indian markets are currently having a roller coaster ride as global headwinds continue to drag the strong domestic fundamentals. Rising Gas prices and disruption in global supply chains (Russia-Ukraine war) are driving inflation to a 15-20 year high in developed markets, it noted.

Further, the hawkish stance by FED and other central banks is likely to push interest even higher in the coming quarters, forecasts the brokerage, adding that shortage of gas and rising interest rates are likely to impact demand with rising fears of a recession in the US and Europe. It expects the global macroeconomic situation to remain volatile in the coming 3-6 months unless there is an end to Russia Ukraine war.

Meanwhile, back home, the brokerage noted that the RBI has been raising interest rates in India in line with US rates, however, the gap between 10-year T Bills in India and US has dipped to a 13-year low. It believes that slowing global growth and volatility can result in further downward pressure on the rupee.

Commenting on domestic inflation, PL said that even though domestic demand remains firm in discretionary segments, rural demand has not shown any uptick. Although RBI expects inflation to soften in another couple of quarters, it is cautious given global headwinds and liquidity pressures.

"Our channel checks suggest strong pent-up demand in the first normal festival season after 2 years. We believe a strong festival season will set the stage for strong growth in the second half of FY23," predicted the brokerage.

Sectors and stocks

PL continues to believe that structurally story led by IT services with strong global demand, expected gains from China+1 supply chain realignment in Pharma, Chemicals, Textiles, etc. and rising visibility of capex across Public Infra, PSU’s, PLI, Defense, Digitisation and Data Centres. It predicts that the current state of volatility to be temporary and recommends accumulating fundamentally strong stocks for medium to long-term gains.

The brokerage is overweight on Banks due to multi-higher credit growth and expected increase in NIM in rising interest rate scenario and retain overweight on all the front line banks like HDFC Bank, ICICI, Kotak, SBI and Axis Bank.

However, it remains underweight on NBFC and reduced weight on HDFC by 70bps but increase weightage on Bajaj Finance by 20bps. However, it believes that Bajaj Finance has the risk of P/BV de-rating if it is asked to get converted into a bank at a certain stage.

Among other sectors, it remains overweight on Healthcare and increase weightage on Cipla. It said that it is structurally positive on leading Hospital chains, given rising insurance incidence and health awareness.

It is also overweight on IT even as it cut the sector's weights by 100bps. "We believe that order books remain healthy and there is no dent to long-term growth story in ERP, Data Analytics, Digital, Artificial intelligence, supply chain, etc. We believe near-term margin pressures are transitory and don’t expect any meaningful impact on the growth trajectory of Indian IT majors due to expected recession/slowdown in the USA," explained PL.

It also remains bullish (overweight) on Automobiles as it sees the current cyclic recovery to last for the next 2-3 years and believes positives like easing out of semiconductor issues, softening commodity prices and strong pent-up demand are key tailwinds. Revival in entry-level segments can further push growth rates, it added.

Meanwhile, it remains underweight on the consumer and oil and gas sectors.

Conviction pick changes

In October, the brokerage removed L&T from conviction picks even as it is not negative on the stock for the long term. However, it might underperform in the near term due to cloud over IT services, it said.

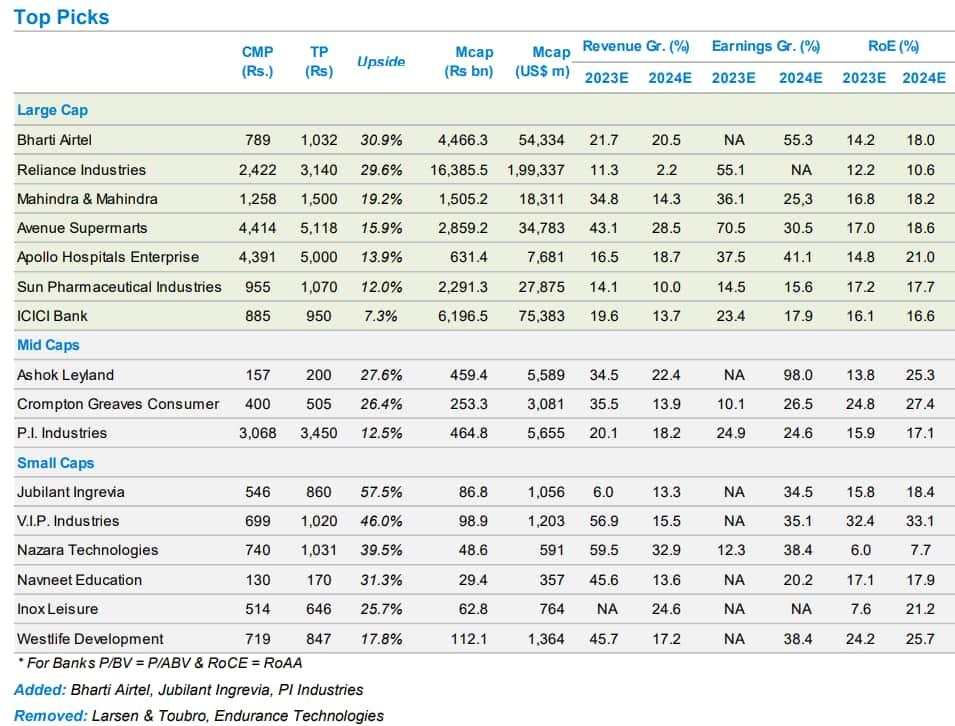

It added Bharti Airtel as a high conviction pick as it is a play on a strong recovery in the telecom sector led by consolidation, rising data usage, integration of Data and Ecom and the expected increase in ARPU with 5G adoption in coming years. PL believes a strong focus on premiumisation and customer-focused strategies will drive 21.8 percent CAGR EBIDTA growth over FY22-25.

It also added Jubilant Ingrevia to its top stock picks as it is well placed to capitalize on long-term growth opportunities given (1) 60 new products pipeline (2) strong traction in CDMO (3) import substitution (4) China+1 policy (5) commensurate capex outlay of ₹2,050 crore over FY22-25. EBITDA contribution from higher value segments is expected to increase to 67 percent by FY25E from 53 percent in FY22, it predicted. Strong balance sheet despite ₹1800 crore cash outflow on capex over FY23-25E, and earnings mix improvement will drive rerating in the stock, it added.