The Reserve Bank of India's (RBI) monetary policy committee (MPC) is set to announce the first bi-monthly policy for the new financial year 2023-24 (FY24) on Thursday, April 6 concluding a 3-day meet. Reserve Bank governor Shaktikanta Das-headed MPC met on April 3, 5, and 6 for this review.

RBI Policy: Repo rate likely to be hiked by 25 bps to 6.75%, highest in 7 years; 4 key trends to follow

TL;DR.

In its continued effort to rein in persistently elevated inflation, most experts expect the RBI to raise the key interest rate yet again by 25 bps on April 6, 2023.

In its continued effort to rein in persistently elevated inflation, most experts expect the RBI is expected to raise key interest rates yet again by 25 bps on April 6, 2023. This would take the repo rate to 6.75 percent which would be the highest rate in 7 years, since March 2016.

This is most probably the last hike in the current monetary tightening cycle that began in May 2022. The Central Bank has already increased the repo rate by a total of 250 basis points since May in a bid to contain inflation, though it has continued to remain above the RBI's comfort zone of 6 percent most of the time.

"The MPC will likely deliver a 25 bps hike, with the decision possibly getting more divided in the form of a vote split. The policy tone will likely be balanced with the move to a neutral stance. But the policymakers would still justify the hike by stating recent inflation surprises, the stickiness of core and the still-elusive 4 percent medium-term target – in a bid to maintain their inflation-fighting credibility as a central bank, especially as they still view growth impulses as stable. We see FY24 average headline/core inflation at 5.2 percent/5 percent, respectively," said Madhavi Arora, Lead Economist, Emkay Global Financial Services. In our view a “hawkish pause” serves less purpose* in sending clearer forward guidance while a ”hawkish hike” makes even lesser sense from the policy perspective amid limited macro levers, Arora added.

Domestic brokerage Nuvama has also forecasted a 25 bps rate hike in the upcoming monetary policy.

The brokerage noted that the MPC’s policy outcome would be presented against the backdrop of unexpectedly high domestic CPI inflation recorded in the last two months (above 6 percent in Jan-Feb’23), continued rate hikes by key global central banks (Fed, BoE, and ECB), volatility in the global financial markets and persistent underlying inflationary pressures.

Alongside the rate action, the commentary and guidance on the course of monetary policy action would be closely watched, it stated, adding that monetary policy action would be contingent on the evolving inflation trajectory.

"The monetary policies of systemically important central banks would also have an indirect bearing on the RBI monetary policy. Even though there is growing expectation of a pause in the rate hike cycle to evaluate the (lagged) impact of the increase thus far (from 4 percent in May’22), the RBI faces constraints on this front with price pressures being unrelenting as evidenced from the firm core inflation (over 6 percent since May’21). To add to this fresh concerns over price levels have emerged with the recent unseasonal rains that have impacted the rabi crop harvest across regions, the risk of subnormal monsoons and the recently announced crude oil output cut by OPEC+ that could push up energy prices. These factors could prolong the RBI monetary policy tightening beyond April 2023," explained Nuvama. As such, it expects the MPC to retain its stance of withdrawal of accommodation.

Aditya Damani, Founder and CEO of Credit Fair also believes that as the retail inflation is above the RBI’s upper tolerance level of 6 percent, the scenario sets the context for another rate hike. Since controlling inflation is the priority of the RBI, a pause in the rake hike is unlikely, however, he expects the RBI to alter its stance from the withdrawal of accommodation to neutral to boost the growth outlook of all the key sectors.

Meanwhile, Ravi Subramanian, MD & CEO of Shriram Housing Finance said, "As the central banks of the developed economies such as the US Fed, European Central Bank and Bank of England have continued with hiking rates, we expect the MPC to follow with a hike of 25bps or lesser this week. consumer prices and core inflation have remained high and are a cause of concern. As the prevailing economic scenario calls for higher rates, we expect the policymakers to take note of the impact of stretched EMIs and loan tenures on the home loan and home-buying demand. Home loan growth for the industry has been in the mid-teens and in the affordable segment demand has been higher and we expect that momentum to sustain despite higher rates.”

Key trends to look out for going ahead:

Inflation: The jump in India’s headline CPI inflation in January 2023 and its persistence in February 2023 has been a huge negative surprise and a cause of concern for the RBI. At 6.4 percent-6.5 percent YoY, it not only reversed the moderation seen in retail inflation over the months of Nov’22 and Dec’22 but once again breached RBI’s upper tolerance of inflation targeting band, noted Nuvama.

Going forward, the brokerage expects the headline inflation to see some moderation in the coming months aided by the base effect, moderation in domestic demand along with the continued easing of supply chain pressures. However, the lagged pass-through of the rise in input costs could keep core inflation firm. Another upside risk could emerge from the recent cut in crude oil production by OPEC+, an early indication of a below-normal Southwest monsoon along with the re-opening of the Chinese economy that could stoke some inflationary pressures for key global commodities, especially that of fuel, food, and industrial metals, it added.

Credit Growth: According to the brokerage, bank credit offtake has registered a strong resurgence in FY23 despite the hike in interest rates. Furthermore, the improvements have been broad-based across segments, reflecting the resilience of the economy and the ability of consumers to withstand higher rates, believes Nuvama. In terms of growth, the incremental (over March 2022) credit offtake growth during 1 April 2022-10 March’23 has been 13.9 percent, while the comparable deposit growth stood at 8 percent, it informed.

Liquidity: In a sharp reversal from the situation of ample surplus liquidity for over 3 years at a stretch, the domestic banking system liquidity has tightened, warned Nuvama. The liquidity surplus since the start of FY23 has registered a notable decline, down from an average of ₹6.5 lakh crore in April 2022 to a deficit of ₹0.4 lakh crore in March 2023.

"The tightness in the liquidity conditions can in large be attributed to fiscal year-end tax outflows from the system and redemption of LTROs towards the end of FY23. The higher pace of credit growth as compared to the deposits has also added pressure on liquidity. The constrained liquidity situation in some segments of the banking sector has also pushed up the call money market rates," stated the brokerage.

Growth: India’s economic activity has continued to remain stable and it is positioned relatively better than most of the economies despite the prevailing global uncertainties, noted Nuvama. The stability in India’s growth momentum can be validated by certain high-frequency indicators namely GST collections, automobile sales, fuel consumption, PMI manufacturing & services, etc., that have not only recorded higher annualized growth rates but have also been registering sequential improvements, it pointed out.

The growth so far has been supported by healthy private consumption amid pent-up demand, alongside a faster resumption in contact-intensive services sectors and the government’s continued thrust on capital expenditure. While this momentum is expected to sustain, the gradual waning of the pent-up demand, the sluggish pace of private capex recovery, unfavourable weather ahead of the rabi harvest season along with continued financial tightening could serve as potential risk factors from the domestic perspective, cautioned the brokerage.

Globally, while bouts of high volatility persist, overall growth prospects have turned out to be stronger than earlier anticipated. Nevertheless, Nuvama believes that still elevated inflationary pressures and expectations of higher interest rates for longer could impact global growth and thereby weighing down India’s growth trajectory.

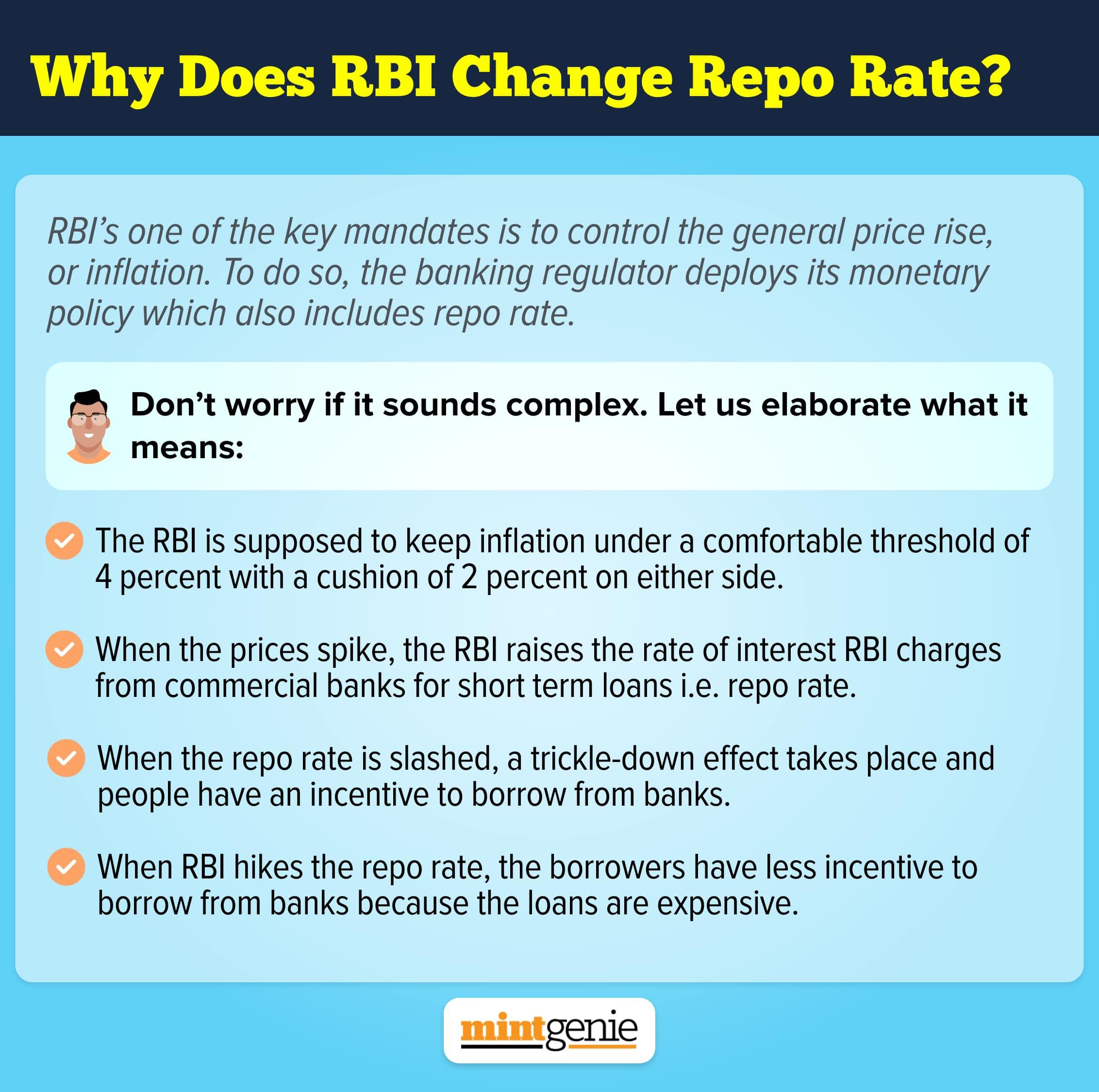

Why does RBI change repo rate?

First Published: 05 Apr 2023, 12:57 PM IST

Related Stories

personal finance

How RBI repo rate hikes impact your home loan EMIs? Here’s all you need to know

Nishant Batra

Explain Like I am 5

personal finance

RBI's Monetary Policy: How does interest rate hike make owning things expensive?

Team MintGenie