Shares of Tata Motors have significantly underperformed the BSE Auto index and equity benchmark Sensex in the last one year.

But now, brokerage firm Motilal Oswal Financial Services believes the day ahead will be favourable for the stock.

As reported by Mint, in the December quarter of the financial year 2022-23, Tata Motors witnessed its first quarterly profit in two years on rising demand for passenger cars as well as medium and heavy commercial vehicles.

Tata Motors reported a consolidated net profit of ₹2,957.71 crore for the third quarter ending December (Q3FY23).

Consolidated revenue from operations at ₹88,488.59 crore, up 22.5 percent as against ₹72,229 crore from the year-ago period.

Tata Motors stock is down 12 percent in the last one year against an over 15 percent gain in the BSE Auto index.

Brokerage firm Motilal Oswal has turned positive about the prospects of Tata Motors' stock. It has retained a buy call on the stock with a target price of ₹540, implying a 17 percent upside potential in the stock.

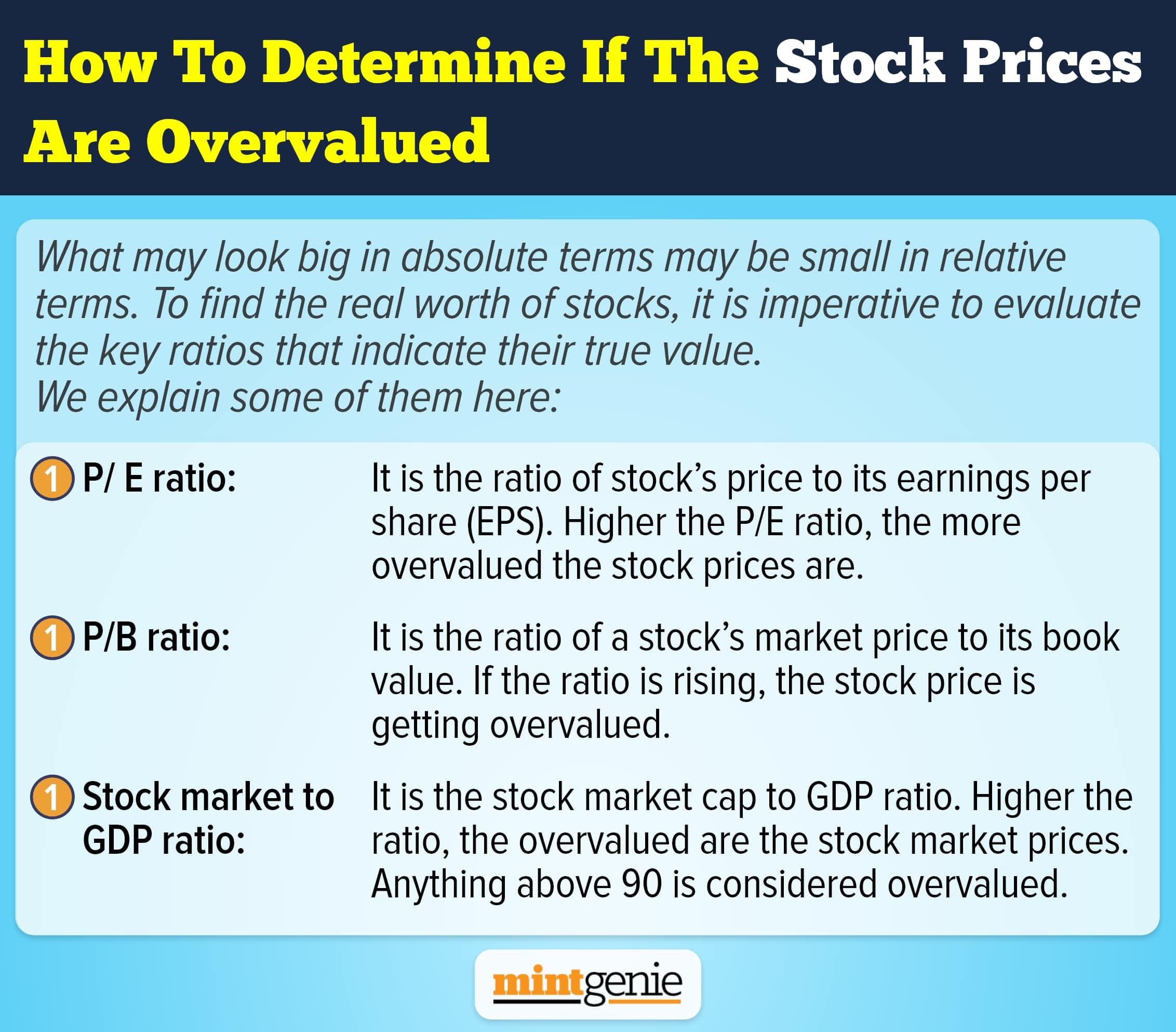

As per the brokerage, the stock trades at 16.2 times FY24 and 13.2 times FY25 consolidated price-to-earnings ratio and 4.1 times and 4.1 times FY24 and 3.4 times FY25 enterprise-value/EBITDA.

Motilal Oswal highlighted improving scenarios for JLR (Jaguar Land Rover) which will underpin Tata Motors. "Improving chip supplies globally, along with a very strong order book, should bode well for JLR," Motilal Oswal said.

JLR, as Tata Group claims, is Britain's largest automotive manufacturer which designs, manufactures and sells some of the world's best-known premium cars. Clearly, a healthy performance of JLR is extremely important for Tata Motors.

While chip supplies have been gradually improving over the last few months, Motilal Oswal underscored that demand for passenger vehicles (PVs) in general and JLR products, in particular, remain strong in key markets globally, even though the macro environment is not supportive.

"JLR is witnessing the benefit of full upgrades of its most important and profitable products, including Range Rover (RR), Range Rover Sport (RRS), and Defender, leading to a substantial increase in the order book," said Motilal Oswal.

"Order backlog for JLR in Europe (including the UK) and RoW (rest of world) markets have surged to 2,15,000 units (as of December 2022). Given the supply-constrained environment, JLR has focused more on production than marketing, as reflected in a sharp reduction in variable marketing expenses (VME) to 0.6 percent in Q3FY23 against more than 5 percent earlier. As supplies improve, it has the lever of increasing VME to 2-2.5 percent to boost volumes, if required," said the brokerage firm.

The brokerage firm highlighted that Land Rover’s mix in overall JLR volumes improved to nearly 83 percent in FY22 from nearly 70 percent in FY19. As a result, blended realizations have registered a nearly 9 percent CAGR over FY19-22, driven by a richer mix of LR than Jaguar as well as lower variable marketing expenses for Land Rover.

"Variable marketing expenses have reduced to 0.6 percent in Q3FY23 from 1.8 percent in FY22 and 7.6 percent in FY20. Further, the mix within Land Rover has also strengthened, driven by upgrades of its three most iconic products, i.e., Range Rover, Range Rover Sport and Defender. As a result, the share of these three models has consistently increased to 65 percent in Q3FY23 from 47 percent in FY22 and 27 percent in FY20. This would further increase as 74 percent of the order book (as of December 2022) is made up of these three models," said Motilal Oswal.

With the visibility of supplies improving gradually, further improvement in the mix and favourable forex, Motilal Oswal expects a sharp improvement in financial performance in JLR at profitability, cash flow, and debt level.

Motilal Oswal believes Tata Motors should witness a gradual recovery as supply-side issues ease for JLR and commodity headwinds stabilise (for the India business).

"Tata Motors will benefit from (a) a macro recovery in India, (b) company-specific volume and margin drivers, and (c) a sharp improvement in free cash flow (FCF) and leverage in both JLR as well as the India business," said Motilal Oswal.

According to a MintGenie poll, an average of 31 analysts have a ‘strong buy’ call on the stock.

Disclaimer: The views and recommendations given in this article are those of the broking firm. These do not represent the views of MintGenie.