Shares of Tata Consultancy Services (TCS) fell nearly 2 percent on Thursday to ₹3,181.10 in intra-day deals after the IT major's March quarter results (Q4FY23) missed Street expectations as clients reduced tech spending after the recent banking crisis in US and Europe and other macro concerns.

TCS Q4 Review: Brokerages remain mixed on the IT stock; near term outlook uncertain

TL;DR.

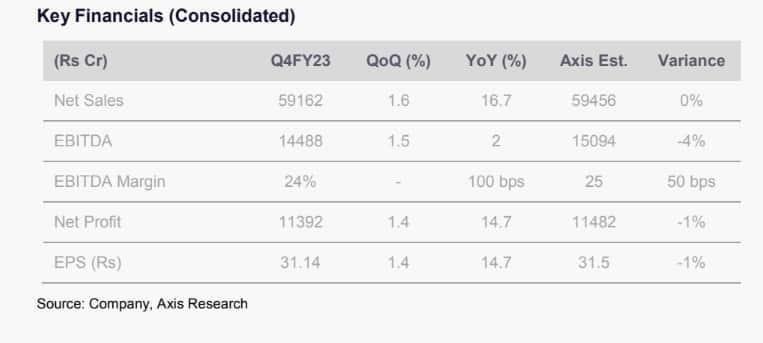

TCS reported a 14.8 percent year-on-year (YoY) rise in its consolidated net profit at ₹11,392 crore for the fourth quarter of FY23 against ₹9,959 crore in the year-ago period.

TCS reported a 14.8 percent year-on-year (YoY) rise in its consolidated net profit at ₹11,392 crore for the fourth quarter of FY23 against ₹9,959 crore in the year-ago period. Its revenue rose 16.9 percent YoY to ₹59,162 crore during the reporting season from ₹50,591 crore a year ago. In constant currency (cc) terms, its revenue rose 10.7 percent YoY. Revenue growth was affected by a slowdown in the BFSI vertical in the second half of the quarter. TCS indicated a demand slowdown in key verticals, primarily in discretionary spends, while cost-efficiency spends remained robust.

The company's operating margins came in at 24.5 percent in the fourth quarter against 24.1 percent in the year-ago period. TCS also declared a final dividend of ₹24 per equity share for the fiscal year.

Brokerages had mixed reviews on the IT major after its subdued results in the March quarter. Let's take a look at what they had to say:

Nirmal Bang: The brokerage has a 'sell' call on the stock with a target price of ₹2,638, indicating a downside of 19 percent for the stock. After holding out an optimistic view on demand for North America, three months back, TCS’ Q4FY23 results (both revenue and margin) fell short of both internal as well as Street expectations as clients pushed back discretionary spending across sectors in that geography after their financial health deteriorated, said the brokerage.

The management did not indicate when it expects growth to pick up and whether it will be front-loaded or backloaded in FY24. The brokerage believes the growth will be broadly weak across all quarters and possibly turn weaker in H2FY24 since the adverse impact of a weak macro is ahead of us and not behind us. This is against general industry commentary before the 4QFY23 results season that demand should start improving from the Sept’23 quarter after two quarters of weakness in March’23 and June’23, it noted.

"While pricing seems stable currently, we see push-back by clients as we move into FY24 when macro conditions will be much more challenging than in FY23. Overall, we believe that revenue growth will likely be in the 3-5 percent region for TCS against a consensus expectation of high single-digit growth, with margins modestly moving up as Utilization tightens and pyramid benefits kick in. We have an explicit view of a shallow recession in the US in CY23 and hence our near-term cautious vie," it said.

Motilal Oswal: The brokerage has a ‘buy’ call on the stock with a target price of ₹3,860, indicating an upside of 19 percent.

"The increase in interest rates, slow economic growth and elevated geo-political tensions have adversely affected the macro environment and raised concerns over IT spends. Given TCS’s size, order book and exposure to long-duration orders and portfolio, it is well positioned to withstand the weakening macro environment and ride on the anticipated industry growth. Owing to its steadfast market leadership position and best-in-class execution, the company has been able to maintain its industry-leading margin and demonstrate superior return ratios. We maintain our positive stance on TCS," it said.

Management commentary on near-term demand was among its weakest in recent history (excluding the initial months of the pandemic). Management indicated weakness in the US on account of deferrals in discretionary spending from clients, with the BFS vertical being the most affected, it noted. "While we view it as concerning, the impact on our estimate for FY24 revenue growth is limited, as a near-term slowdown has been widely expected and partially factored in our estimates," it estimated.

Phillip Capital: The brokerage maintained its ‘buy’ call on the stock with a target price of ₹3,930, indicating an upside of 23 percent.

"TCS reported slightly weaker numbers than expected on both revenue growth and margins. Revenue growth was at 0.6 percent CC QoQ (vs 1.0 percent est), while margins remained flat QoQ at 24.5 percent. Miss on growth is primarily attributed to the delayed ramp-up of existing deals and the impact on discretionary spending led by macro weakness, especially in the US. Deal TCV however was robust at $10bn (up 28 percent QoQ, second highest) with TCS signing a higher proportion of $50-100 mn in FY23 vs FY22. Management commentary on demand was cautious in the near term due to the weak macro environment primarily in US led by recent events in the banking sector. Uncertainty is not fully resolved yet and it might have some impact on discretionary spending," said the brokerage.

In FY24, while H1 growth might be relatively softer than a normal year given the uncertainty, PC believes growth should bounce back in H2 helped by robust TCV wins with more short-duration deals won by company helping in faster revenue conversion. It said TCS will be one of the big beneficiaries of the digital transformation, cost takeout and vendor consolidation-led opportunities given its multiservice and multi-vertical offerings and also expects TCS to continue to command valuation premium to its peers, on the back of its strong diversified profile, superior return profile (ROE of 46 percent in FY23), management stability, strong margins, and market leadership position.

Emkay: The brokerage retained its ‘hold’ call with a target price of ₹3,300 per share, indicating an upside of just 2 percent. The brokerage said the management remains watchful in the near term, considering the heightened macro uncertainties; however, it reiterated confidence in accelerating revenue growth, once uncertainties abate. The brokerage also cut TCS' earnings estimate by 0-1.5 percent for FY24-25 post the Q4 performance. Healthy deal intake and moderation in attrition were key positives in Q4, it added.

Axis Securities: The brokerage has a ‘hold’ call on the stock with a target price of ₹3,350, indicating an upside of just 3 percent. In Q4FY23, TCS reported revenue growth of 1.6 percent QoQ in rupee terms, which was below expectations, said Axis. The management commentary on the verticals BFSI, Hi-tech Media, Life Sciences, and Retail was cautious and it expects the company to report moderated growth in the near term. Deal-wins for the quarter continued strong and remained high. Moreover, deal wins were spread across verticals and across geographies and stood at $10.1 Bn. However, TCS expects technology spending to remain resilient and expects the secular tailwinds to drive healthy growth over the medium term to long term, noted the brokerage.

"From a long-term perspective, we believe TCS has built a resilient business model by securing multiple long-term contracts with the world’s leading brands and has established robust capabilities to gain market share. However, rising concerns over uncertainties from large economies may create headwinds to the growth prospects of the company," it said.

/source: Axis Securities

First Published: 13 Apr 2023, 12:26 PM IST