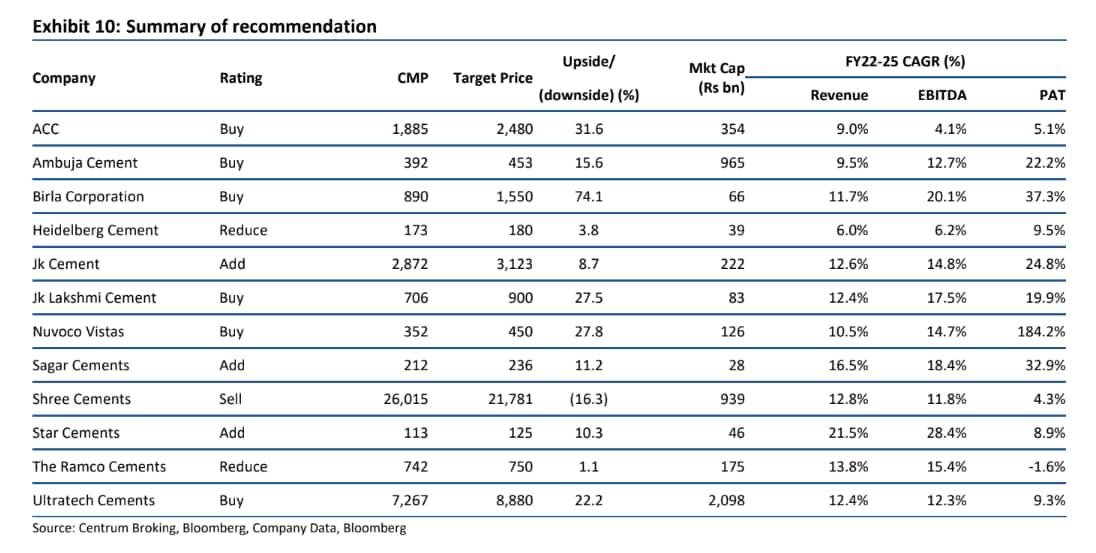

Cement stock Birla Corporation is Centrum Broking's top pick in the cement space. The brokerage has initiated coverage on the stock with a ‘buy’ call with a target price of ₹1,550, indicating an upside of nearly 79 percent from its current market price (CMP) of ₹867.85 (as on March 13, 2023).

The brokerage believes that Birla Corporation is a potential rerating candidate due to consistent addition in capacity leading to higher than industry volume growth, modernisation and upgradation of plants through continuous investments leading to further improvement in cost structure, expansion of return ratios and substantial deleveraging over FY22‐25.

"The company ticks most boxes of our filters for stock selection like growth, return ratios, and size, we believe that as earnings improve, there is a good chance of rerating of the stock. Weak pricing in central and eastern regions due to higher supply and delay in the next phase of capex are key downside risks to our call," said the brokerage.

It expects the company to double its EBITDA to ₹1900 crore in FY25E from ₹840 crore expected in FY23E, driven by higher volumes and lower costs. It also believes that the consensus is underestimating the earnings potential of the company given the accretion of sizeable incentives from FY24E and the increased share of domestic coal from captive mines.

In the December quarter (Q3FY23), the company reported a consolidated net loss of ₹49.91 crore as against a profit of ₹60.45 crore in the corresponding quarter a year ago.

Total revenue at ₹2,024 crore, including sales from the Mukutban unit (of a subsidiary, RCCPL), which started commercial operations in the current financial year, was higher by 15.2 percent. On a comparable basis, Birla Corporation said, consolidated revenue was up by 9 percent year-on-year (YoY).

The company said that although the Mukutban project has been ahead of its plans and the adverse impact on the bottom line had been contained, extraordinary cost pressure on the cement industry pulled down the overall financial performance.

To mitigate cost pressure, the company said, it had optimised its fuel consumption mix, the full benefits of which would be realised in the March quarter. Fuel prices have declined which is likely to improve profitability. The focus of the company in the coming months is to ramp up the Mukutban operations, said Birla Corp.

The stock has fallen 24 percent in the last 1 year and over 13 percent in 2023 YTD. In the current calendar year, the stock has been in the red in all 3 months (including March so far).

The stock has fallen 2.5 percent in March MTD, 4 percent in February and 7.5 percent in January 2023.

The stock has fallen nearly 30 percent from its 52-week high of ₹1,232, hit in April 2022. However, from its 52-week low of ₹822.80, hit in June 2022, the stock has advanced around 5 percent.

Investment Rationale

Profitable volume growth ahead: Birla Corp has commissioned a 3.9 mn mt modern plant at Mukutban in Maharashtra in FY22 and the brokerage expects this plant to drive a 9 percent volume CAGR for the company over FY22‐25E. The efficient plant along with captive power, WHRS and railway siding is likely to result in profitable growth for the company, it said. The plant is eligible for lucrative incentives from the state government which can contribute ₹200 crore annually as incentives from FY24E, noted Centrum.

Captive coal mines will offer insulation from volatile global fuel prices: The brokerage also pointed out that currently, Birla Corp has one operational coal mine which is contributing 20 percent of the total coal requirement of its central region assets. It has also received three more coal blocks through auction (all in Madhya Pradesh) which are expected to be operational in a phased manner till FY26E, noted Centrum. Out of this, one mine, Bikram coal, is expected to be operational by Q4FY23E. Once all mines are operational, more than 80 percent of the total coal requirement of the company is likely to be met through internal resources, forecasted the brokerage.

Leverage ratios to improve, cost of next capex to be lower: The brokerage further mentioned that Birla Corp has completed its large greenfield capex at Mukutban which resulted in a bump‐up in its debt/EBITDA ratios. Given the absence of large-scale greenfield expansion in near future, it expects the debt to come down sharply from ₹3,240 crore in FY22 to Rs16.2bn in FY24E. The next set of capex will be brownfield in nature and hence capex/mt will be much lower resulting in further improvement in return ratios, it added.

Peers

The brokerage also has ‘buy’ ratings on ACC (target price: ₹2480, upside: 32 percent), Ambuja Cement ( ₹378, 15.6 percent), Nuvoco Vistas ( ₹450, 28 percent), JK Lakshmi Cement ( ₹900, 27.5 percent), and UltraTech Cement ( ₹8,880, 22 percent).

Meanwhile, it has ‘add’ calls for JK Cement, Sagar Cement and Star Cement.

However, it has a ‘sell’ call on Shree Cement with a target of ₹21,781, indicating a downside of 16 percent. It also has 'reduce' calls on Heidelberg Cement (target: 180, upside: 4 percent) and Ramco Cements ( ₹750, 1.1 percent).

As per the brokerage, the cement sector in India is likely to witness the twin advantage of better demand and softening of operating costs, thereby leading to the recovery of margins. Over the past year, the industry had faced challenges related to surging operating costs i.e., coal and pet coke, and the brokerage believes that the sector has managed to balance the cost pressures and demand well.

Margin recovery has already started from Q3FY23 and it expects normalization of margins in FY24E given softening costs and better realizations. It sees cement demand growing at a healthy CAGR of 7.8 percent over FY22‐25E driven by pre‐election spending by the government and the affordable housing segment. Cement prices are likely to remain steady in FY23E with some improvement expected in Q1FY24E, forecasted Centrum.

"We are building in 11 percent/12 percent CAGR in revenue/EBITDA for our coverage universe over FY22‐25E and expect EBITDA/mt to reach FY21 levels by FY24E. Given the weak base of FY23E, growth in revenue/EBITDA over FY23‐25E is likely to be better at 6 percent/26 percent, respectively. UltraTech Cement, Ambuja Cement, Birla Corp, Nuvoco Vistas and JK Lakshmi Cement are our preferred picks in the sector," said the brokerage.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.