India is one of the most attractive and fastest growing alcohol markets in the world. The Indian alcohol market is mainly dominated by whiskey, followed by beer and wine, with the premium end of the Indian spirits market largely dominated by the top two global companies: Diageo and Pernod Ricard.

United Spirits vs Radico Khaitan vs United Breweries: Who rules the market?

TL;DR.

India's liquor industry is showing signs of recovery in margins, with mix improvement and price hikes driving growth. Brokerage house Nuvama analyses the performance of United Spirits (UNSP), Radico Khaitan, and United Breweries (UB).

In a recent report, brokerage house Nuvama analysed the performance of United Spirits (UNSP), Radico Khaitan, and United Breweries (UB).

Margins

After a tough FY23, the brokerage house noted that the liquor industry finally saw some green shoots in margins aided by mix improvement. However, competitive intensity remains high. Other key concerns are glass is still inflationary in Q1FY24 (likely to correct in Q4FY24), ENA prices could get impacted due to El Nino and ethanol mixing, it cautioned. Despite that, Nuvama noted that the worst of inflationary pressures is likely behind.

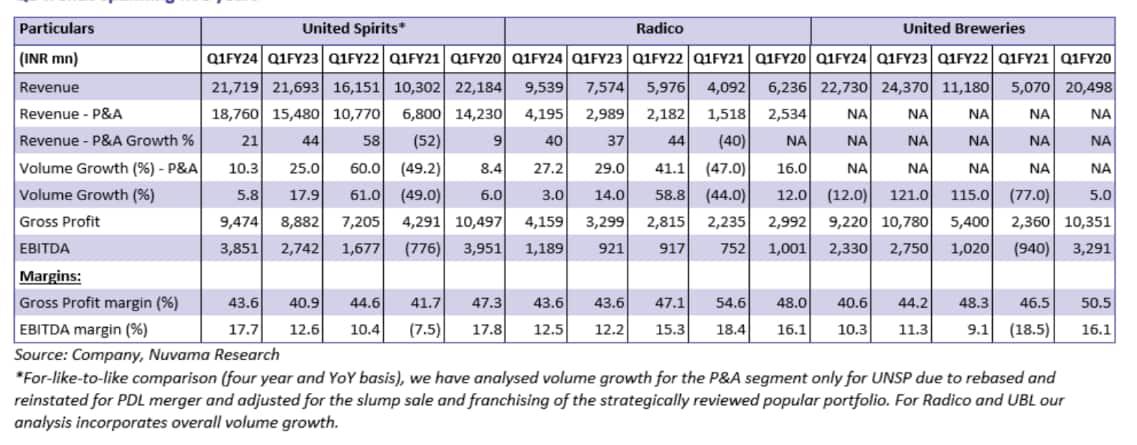

"Events and marriages are back to pre-covid levels and shall drive a spike in alcohol consumption. This could negate the urban slowdown, which is plaguing many other forms of discretionary consumption such as QSR, apparel, and footwear. In terms of gross margin, UNSP, and Radico topped at 43.6 percent, and UBL at the bottom at 40.6 percent," noted Nuvama. UNSP margins were aided by the comeback of BIO and mix changes, whereas for Radico price increases in Country Liquor and premiumisation in IMFL business helped.

It further pointed out that in terms of EBITDA margin, UNSP outpaced Radico and UBL. UNSP clocked an EBITDA margin of 17.7 percent aided by a sharp bump-up in IPL and mix improvement, followed by Radico at 12.5 percent while UBL had a mere 10.3 percent EBITDA margin.

Four-year comparison

On a four-year basis, all three companies still have a significant dip in gross margins, stated Nuvama. UNSP performed relatively better with a gross margin contraction of 370 bps while Radico saw a compression of 438 bps whereas UBL is at the bottom with 993 bps contraction in gross margin.

Similarly, analysing the EBITDA margin on a four-year basis, the brokerage informed that UNSP did well with its EBITDA margin staying flat. On the other hand, Radico witnessed an EBITDA margin contraction of 359 bps while UBL is at the bottom with its gross margin nosediving 580 bps.

Moving on to revenue growth on a four-year basis, Nuvama stated that Radico posted robust revenue growth of 53 percent in Q1FY24 (versus Q1FY20) followed by UBL at 11 percent. UNSP, on the other hand, posted an overall revenue decline of 2.1 percent due to sales of the lower end, it added.

Now, on the volume front, Radico posted volume growth of 5.6 percent in Q1FY24 (versus Q1FY20), followed by UNSP at 2.4 percent. UBL, on the other hand, posted a volume decline of 3.8 percent, observed Nuvama.

As per the brokerage, premiumisation marks the most important theme for these companies, transiting to a more value-led growth in the P&A segment. For instance, on a four-year basis, Radico posted robust revenue and volume growth in the P&A segment of 65.5 percent and 22.6 percent (versus Q1FY20), respectively, followed by UNSP at 31.8 percent and 12.1 percent P&A revenue and volume growth, respectively.

Source: Nuvama

YoY Comparison

In terms of YoY sales growth, Radico topped with growth at 25.9 percent, followed by UNSP at flat and UBL at a decline of 6.7 percent, informed Nuvama. It also noted that in terms of volume growth YoY, Radico’s P&A did the best at 27.2 percent while UNSP saw 10.3 percent growth and UBL disappointed with a 12 percent decline.

Analysing margins, Nuvama observed that UNSP saw good gross/EBITDA margin expansions. UBL was the only one that saw a contraction in gross/EBITDA of 367bp/103bp. Radico’s gross margin remained flat YoY, but its EBITDA margin expanded by 30 bps. Meanwhile, UNSP’s gross/EBITDA margin expanded by 268bp/509bp YoY, aided by the comeback of the BIO portfolio and IPL revenue, it said.

Stocks

United Spirits: The brokerage pointed out that the company did well in the P&A space with revenue growth of 31.8 percent (versus Q1FY20), indicating UNSP’s efforts on renovation, innovations in its portfolio and consumer preference migrating towards P&A.

On the margins front, gross margin expanded sequentially but is still below pre-Covid levels. However, the gap has now narrowed indicating prudent raw material cost measures and efficient inventory management. EBITDA margin expanded sequentially and on a 2-year basis and is now in sync with Q1FY20 (pre-covid) levels, mainly on account of the re-shaping of UNSP’s portfolio, it added.

The stock has risen over 23 percent in the last 1 year and 15 percent in 2023 YTD, giving positive returns in 5 of the 8 months so far in the current calendar year. The stock snapped 5 straight months of gains between March and July to fall around a percent in August so far.

Between March and July, it had advanced over 37 percent.

Radico Khaitan: As per the brokerage, Radico Khaitan has seen robust sales growth on a YoY basis, with P&A outpacing the regular segment. In terms of YoY volume growth for the P&A segment, Radico outpaced UNSP on account of strong efforts to drive premium value growth, it noted.

On the margin front, gross margins witnessed a sharp contraction across years, but on a YoY basis remain flat. This was mainly due to high inflation in ENA and glass prices. The company has incurred ₹680 crore on the Rampur Dual Feed and Sitapur greenfield projects since inception, leading to an increase in its net debt, stated the brokerage.

The stock has gained over 21 percent in the last 1 year and 24 percent in 2023 YTD, giving positive returns in 6 of the 8 months so far in the current calendar year. The stock snapped 3 straight months of gains between May and July to fall over 13 percent in August so far.

Between May and July, it had advanced over 29 percent.

United Breweries: "UBL’s Q1FY24 was weak on account of a negative state mix and inflationary pressure. Volume growth was impacted by RTM (root to market) changes, supply challenges and lower inter-state sales. Karnataka sharply increased prices post-elections. We see a risk in other state elections leading to higher stimulus programs driving sharp price hikes in the liquor industry, glass inflation (capacity constraints) and high ENA (extra neutral alcohol) prices," stated the brokerage.

It further analysed that the company's value/volume growth compressed on a YoY basis and gross margins were also impacted and deteriorated across the years, it added.

Going forward, the company continues to build on category growth while driving the share of premium in its portfolio. The company remains optimistic about the long-term growth potential of the industry, it stated.

The stock has lost over 6 percent in the last 1 year and 10 percent in 2023 YTD, giving negative returns in 5 of the 8 months so far in the current calendar year. Just in the first 3 months of 2023, it shed over 16 percent.

Outlook

The brokerage noted that the liquor industry is finally witnessing some recovery in margins after tepid three quarters led by mix improvement, price hikes and some deflation in raw material costs. The worst is likely behind but ENA remains a concern, it added.

According to Nuvama, the prestige segment, also known as the deluxe segment, is the largest segment in the whisky market at 50 percent by volume in India and is projected to reach 53 percent by FY25. The popular segment, or mass premium segment, makes up 37 percent by volume in India’s whisky market. Together, the value segment (popular + prestige) account for a market share of 87 percent, it informed.

ndian Made Foreign Liquor (IMFL) sales by value were estimated at ₹1.74 lakh crore in FY22 and are projected to reach ₹2.4 lakh crore by FY25. From FY22 to FY25, IMFL sales value/volume are expected to clock a CAGR of 11.3 percent/6.2 percent, it added.

Also, the Indian whisky market, valued at $14.9 bn in FY20, is projected to touch $22.4 bn by FY25 on the back of demographic trends, new customers, and premiumisation. The market is set to drive value growth with strong premiumisation trends leading to up-trading within the category as well as an increasing preference for high-value products across price segments, it predicted.

Going ahead, the brokerage believes the government's control in almost all states in terms of pricing/distribution, sudden excise duty issues cropping up, high competitive intensity and high ENA (extra neutral alcohol) prices are key risks to this space.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

How India likes its alcohol

First Published: 29 Aug 2023, 02:10 PM IST