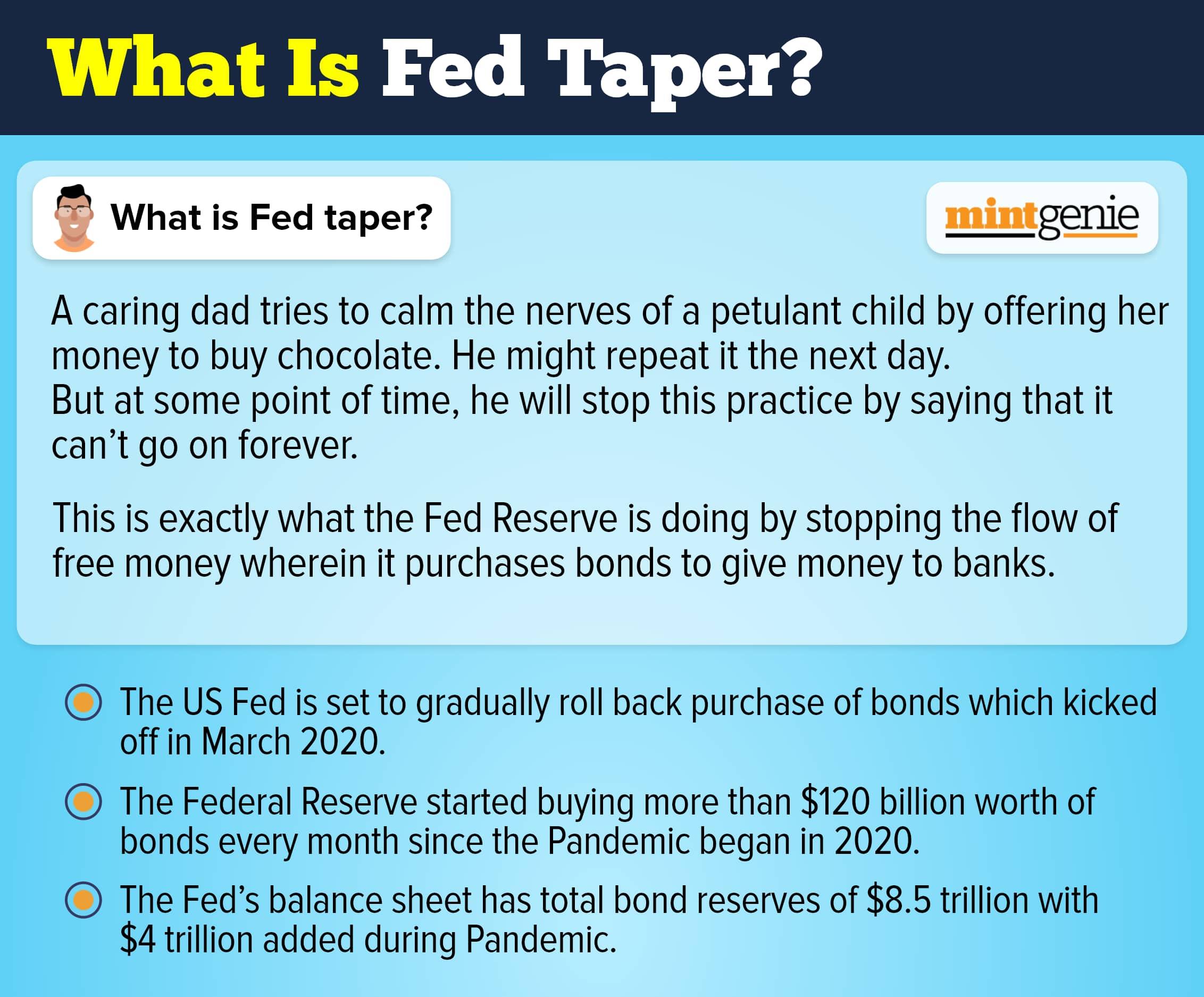

The FOMC meeting this week will ponder if ‘Peakflation’ may not, in fact, have peaked. While inflation continues to surprise consensus estimates to the upside, growth momentum has started surprising estimates on the downside.

As markets prepare for stagflation, they have begun to vociferously question how far the Fed can go to engineer a soft landing of this short but explosive business cycle.

The debate on this week’s FOMC policy is no longer about a 50bp or a 75bp rate hike going ahead, but about how high the policy terminal rate needs to be by mid-2023 to contain the Fed’s conundrums.

The pace and quantum of moves towards the terminal rate will possibly decide the fate of the so-called landing, be it a hard one, aka recession, or a soft one - more like a mid-cycle slump.

While there may be more pain in store for the Fed from the headline inflation numbers going forward, core inflation could be near its peak on a YoY basis (now 6 percent).

However, sequential gains are still running thrice as fast (0.6 percent month-on-month) against the healthy pace of 0.2 percent that the Fed intends to see.

This makes us believe that the supposedly hawkish Fed so far has, at least, not been aiming to crash growth meaningfully, if one sees their median forecasts for terminal rates and core inflation, and thereby the implied real policy rate.

Specifically, post the new-found hawkishness in Nov’21, and giving up on the “transitory” inflation narrative, the Dec’21 FOMC still forecasted the implied real terminal rate at an incredibly low 0.7 percent, even after upping their nominal terminal rate forecast by 60bps!

This posed credibility issues because a negative real policy rate would not have achieved the ‘slower growth-lower inflation’ aim without a miraculous supply side response.

This half-hearted narrative continued even in the Mar’22 FOMC forecasts, where, despite upping the nominal terminal rate target by another 120bps from 1.6 percent to 2.8 percent, the real rate forecast barely reached positive territory, at 0.2 percent.

Even adjusted for the impact of QT, tantamount to another 50bp of hikes, the implied real terminal policy rate of +0.7 percent would still be one of the lowest-ever real terminal rates in the hiking cycles, second only to the real terminal rate seen in the 2018 cycle.

Even the ‘highflationary’ 1970s and 1980s hikes saw deeply positive real terminal rates!

Does this imply, then, that not only is the Fed behind the curve, but even the projected hiking plans do not look concerted enough if one judges the Fed by the real rate terminus?

Does that mean, given economic overheating and sticky supply constraints, that the terminal real policy rate needs to be in the range of 1.5 percent to 2 percent (QT adjusted), in line with past hiking cycles?

If so, does it imply a much higher hike on Wednesday, June 15 (75bp) and a serious revision of the nominal terminal rate to the tune of, say 3.5 percent, in the FOMC’s new projections?

Well, the case for that looks plausible to us, given their need to credibly crush inflation amid a serious catch-up.

While we believe that money markets may have largely factored all this in, as we previously argued, the pain will likely linger for equity and credit markets, especially as the sharp growth and earnings revisions, due to possible stagflation/recession, bake into valuations when rates reach these higher levels in early 2023.

Our study also shows how equities and credit struggle historically well after rates peak. Thus, investors may need to brace for occasional bear market rallies in the coming months.

(Madhavi Arora is Lead – Economist, Emkay Global Financial Services)

Disclaimer: The views expressed in this article are those of the author and not of MintGenie.