Food delivery major Zomato has bounced back strongly in the current year after a weak show last year in 2022. The stock has exhibited a remarkable recovery in 2023 so far, jumping almost 68 percent. The stock lost 57 percent of its investor wealth in 2022.

Zomato: After a 68% rise in 2023 YTD, Equirus Securities sees another 36% jump – here's why

TL;DR.

Zomato's stock has bounced back in 2023, jumping almost 68% after losing 57% in 2022. Domestic brokerage house Equirus Securities expects the stock to rise further, initiating coverage with a 'long' rating and a target price of ₹135. Equirus forecasts strong revenue and EBITDA growth for Zomato.

Post the incredible recovery this year, domestic brokerage house Equirus Securities expects the stock to rise further going ahead. It has initiated coverage on the stock with a ‘long’ rating with a target price of ₹135, indicating an upside of around 36 percent in 12 months.

"Zomato, one of India's leading online food service platforms, offers food delivery, Quick-commerce (Q-commerce), B2B supplies, and dine-out services. Its dominance in the underpenetrated food delivery space should drive a robust 31 percent sales CAGR over FY23-FY28E, making it one of the fastest-growing players in India’s internet landscape. An asset-light balance sheet and ₹11,500 crore of cash balance would facilitate Zomato’s entry into adjacencies, enabling further value creation – a case in point being the Blinkit acquisition and subsequently accelerated strides towards profitability," explained the brokerage.

Currently trading at around ₹99.46, the stock is still over 41 percent away from its record high of ₹169, hit on November 16, 2021. After starting its downward trend in June 2022, the stock re-hit its IPO price a year later in June this year. It has risen over 30 percent from its IPO price of ₹76.

Meanwhile, the stock rallied over 124 percent from its 52-week low of ₹44.35, hit in January this year. Meanwhile, in the last one year as well, the stock has advanced nearly 59 percent.

Zomato stock

Earnings

In the June quarter (Q1FY24), the food aggregator reported its first-ever consolidated net profit of ₹2 crore as against a net loss of ₹186 crore in the year-ago period. The revenue from operations during the quarter came in at ₹2,416 crore versus ₹1,414 crore in the year-ago period.

The company said its food delivery business posted adjusted revenue of ₹1,742 crore in the first quarter as compared to ₹1,470 crore in the year-ago period. The gross order value (GOV) for the food delivery business showed strong growth, rising by 11.4 percent QoQ to reach ₹7,318 crore in Q1, compared to ₹6,569 crore in the preceding March quarter. Furthermore, Blinkit, the grocery delivery service, also performed well, with revenue reaching ₹384 crore in Q1, a significant increase from ₹164 crore in the year-ago quarter. The GOV for Blinkit grew by 5 percent QoQ, reaching ₹2,140 crore.

Overall, the company's EBITDA loss narrowed sharply to ₹48 crore in Q1 from ₹307 crore in the year-ago quarter.

Commenting on the Q1 performance, Zomato Chief Financial Officer Akshant Goyal said, "Realistically speaking, we were expecting to hit this milestone in the September quarter, and we were being conservative in our earlier guidance. However, some critical parts of the team across our businesses out-executed our expectations/plans, and some of our initiatives delivered better outcomes than we had expected."

“We expect our business to remain profitable going forward, and knowing what we know today, we believe we will continue to deliver 40 percent-plus YoY topline (adjusted revenue) growth for at least the next couple of years,” Goyal said.

Investment Rationale:

Recent additions/acquisitions: Zomato has consistently pursued strategic acquisitions to enhance its offerings. Notable among these acquisitions is the integration of UberEats in FY21, which marked a significant milestone. Building upon this momentum, Zomato has continued to expand its portfolio through further acquisitions and the introduction of innovative new products. Zomato announced the complete acquisition of Blinkit (erstwhile Grofers), a quick commerce player, via preferential share issuance and cash, valuing the latter at $750 mn. Moreover, Zomato's investments in Magicpin and Shiprocket have strategically positioned the company to tap into the potential benefits arising from the ONDC initiative, stated the brokerage.

Food delivery growth: Zomato's food delivery business thrives on three growth levers: (a) user base (MTU), (b) ordering frequency, and (c) average order value (AOV).

Growth in monthly transacting customers will be driven by both new customer additions and higher repeat rates of existing customers. Currently, only 8-9 percent of internet users in India utilise online food services. Therefore, acquiring new users remains a key growth driver for Zomato, noted the brokerage. It further pointed out that in CY22, a mere 2.7mn customers accounted for 33 percent of total order volumes, representing only 4.7 percent of Zomato's unique annual customer base. This suggests the remaining 95.3 percent of customers place orders only 8 times a year, or once every 1.5 months. By tapping this segment, Zomato can unlock immense potential for MTU growth. It anticipates MTUs to experience a robust 15 percent CAGR over FY23-FY28E, reaching 34 mn by FY28E. Equirus also expects AOVs to stabilize at current levels and grow at 3-4 percent p.a., slightly below inflation.

Gross Order Value: The brokerage also noted that Zomato's delivery business GOV (Gross Order Value) is poised to achieve a compelling CAGR of 23 percent over FY23-28E and is expected to reach ₹74000 crore by FY28. The GOV build-up model, outlined in the Exhibit below, takes into account the growth levers contributing to this substantial increase, it said.

Blinkit: Zomato acquired Blinkit (formerly Grofers) on 10 Aug’22, making it a wholly-owned subsidiary. The brokerage believes Blinkit – specialising in rapid grocery and essentials delivery (average delivery time of <15 minutes in May’22) – is currently the most cost-efficient and largest Q-Commerce business in India. The company operates through a network of dark stores and third-party warehouses. Having fully embraced the Q-Commerce model in Jan’22, Blinkit started with a premium positioning; the service is expected to become more mass-oriented over time. Currently, Blinkit serves 19 cities and is expanding operations within these cities, it added.

"In Feb’22, Zomato had capped its Q-commerce investment at $400 mn in CY22/CY23, mostly for covering Blinkit’s losses in this period. But in August’22, it lowered this limit to $320 mn. Blinkit has turned contribution-positive as of June’23 and would likely attain adj. EBITDA breakeven by 2QFY25, with cumulative cash investment below $320 mn envisaged earlier. Profitability led by growth: We expect Blinkit to achieve an adj. EBITDA of ~5.4 percent of GOV, with contribution margin (% of GOV) of 8.3 percent by FY28E. For context, DMart achieves store-level margins of 9-10 percent," noted the brokerage.

Zomato vs Swiggy: The competition between Zomato and Swiggy in the food delivery market remains intense as both companies strive to retain their respective market shares. Recent data released by Prosus stated that Zomato’s reported metrics reveal that it held a substantial lead with a food delivery market share of 55 percent in CY22 versus the 45 percent market share of Swiggy. Despite Swiggy's efforts, including higher discounts and its flagship program 'Swiggy One,' Zomato's market share has been robust.

"The ongoing tug of war between Zomato and Swiggy persists, with both companies fiercely competing to retain their market shares in the food delivery business and enhance profitability. The re-launch of the Gold loyalty program in January 2023 is anticipated to support Zomato in extending its market share lead in the first half of CY23. It's important to recognize that the online food delivery market in India is far from being an absolute monopoly, as both companies emphasise profitability over aggressive market share expansion," it explained.

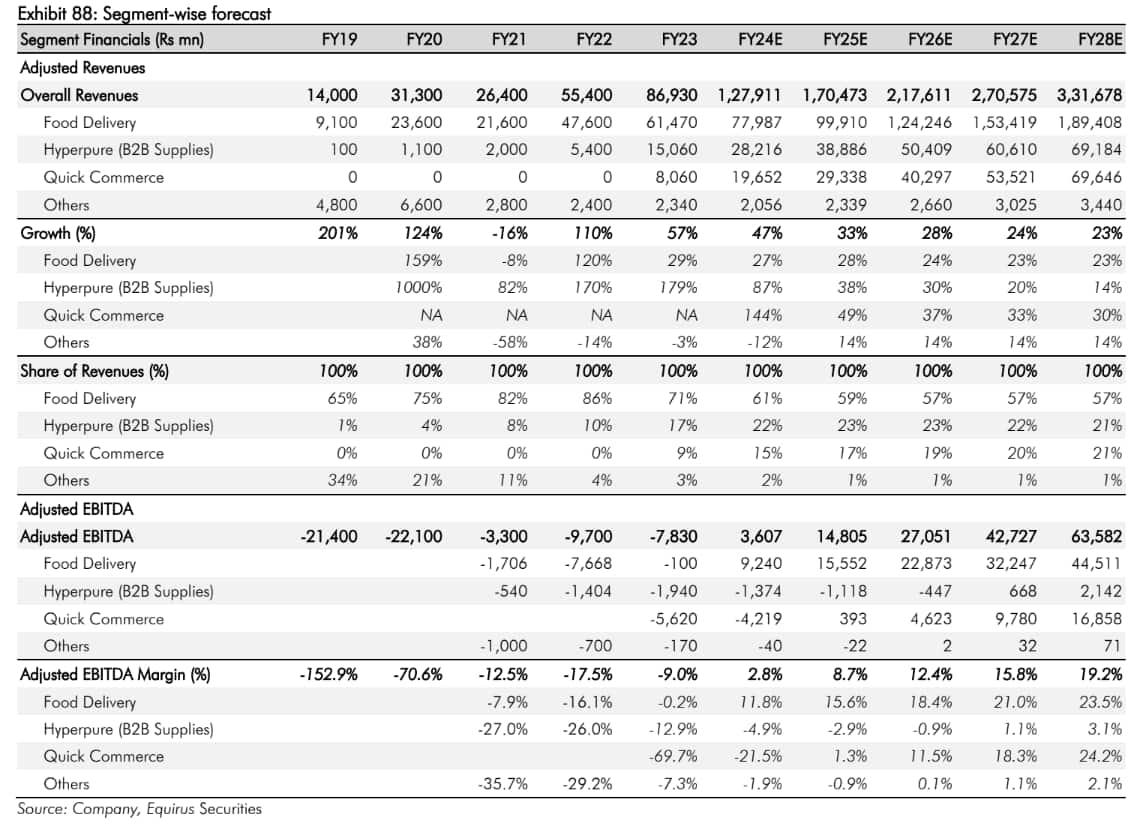

Financial forecasts: Equirus believes Zomato is well-poised to leverage the large, growing opportunity in the food services ecosystem due to its leadership, strong balance sheet and diversified offerings across the value chain. At the consolidated level, it is likely to see a strong 31 percent adjusted revenues CAGR over FY23-FY28E and a 105 percent adjusted EBITDA CAGR over FY24E-FY28E, it forecasted.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie. We advise investors to check with certified experts before taking any investment decisions.

Source: Equirus

First Published: 11 Sep 2023, 02:59 PM IST

Related Stories

markets

Zomato spikes over 13.5% to a 17-month high after company turns profitable in Q1

A Ksheerasagar