For good or bad reasons, the stock of Zomato has been under investors' radar since its listing on July 23, 2021.

Zomato Stock Check: Long-term story or a short-term bet? Here's what fundamental and technical analysts say

TL;DR.

Zomato has been on a downward spiral owing to concerns over its growth and profitability. From its all-time high of ₹169.1 which, as per the BSE data, it hit on November 16, 2021, the stock is down more than 62 percent (as of December 8 closing).

The stock has been on a downward spiral owing to concerns over its growth and profitability. From its all-time high of ₹169.1 which, as per the BSE data, it hit on November 16, 2021, the stock is down more than 62 percent (as of December 8 closing).

Zomato stock in last one year.

As reported by Mint earlier, Zomato's consolidated net loss narrowed to ₹251 crore for the September quarter of the current financial year. In the same quarter last year, the company had seen a consolidated net loss of ₹430 crore.

Consolidated revenue from operations rose by 62.2 percent to ₹ ₹1,661 crore as against ₹1,024 crore in the year-ago period.

Zomato completed the acquisition of Blinkit in August and the September quarter earnings included about 50 days of Blinkit’s financials in the consolidated numbers. Adjusted for Blinkit, the revenue grew 48 percent year-on-year, resulting in an annualized revenue of $1.05 billion.

What is the road ahead for the stock? What do fundamentals and technical indicators indicate? Should you buy, hold or sell it? We collated the views of brokerage firms and analysts on the stock. Here's what they say:

Fundamental Views

Brokerage firm: Nuvama Wealth Management (formerly Edelweiss Securities)

The brokerage has a buy call on the stock with a target price of ₹85.

The brokerage firm highlighted that Zomato’s food-delivery GOV (gross order value) grew 22.6 percent year-on-year (YoY) in Q2FY23 driven by growth in order volumes and AOV (average order value).

GOV growth decelerated as the company focused on trading lower-quality growth for better unit economics. Management also highlighted that app opening was seasonally impacted because of rains and competitive intensity was higher.

Zomato clocked a contribution margin of 4.5 percent (up 170bp quarter-on-quarter), primarily driven by an increase in take rates (17.1 percent in Q2FY23 versus 16.7 percent in Q1FY23) and an improvement in customer delivery charges.

"We expect growth in GOV to recover in a seasonally strong Q3 and Q4 ahead," said the brokerage firm.

Moreover, the brokerage firm believes Blinkit is leveraging Zomato’s customer base for incremental order volumes.

Management is focused on closing the unviable dark stores and uses Zomato’s user data to determine new locations where dark stores could be opened.

"We believe that delivery fleet integration can be a key profitability lever once operations are stabilised," said Nuvama.

The brokerage firm underscored that although the pace of MTU (monthly transaction users) addition in food delivery (1.6mn addition in the first half of FY23) has been slow, the annual transacting user base of 50mn-plus provides comfort on prospects of higher conversions.

"We are building in a 26 percent GOV CAGR over FY23-26E for the food delivery business and expect gradual improvement in unit economics to lead to a contribution margin of 6.6 percent in FY26. We expect Zomato (excluding quick-commerce) to be adjusted-EBITDA positive by Q4FY23 and including quick commerce to be adjusted-EBITDA positive by Q4FY24," said the brokerage firm.

Brokerage firm: JM Financial

The brokerage firm has a buy call on the stock with a target price of ₹125 as the brokerage firm believes the stock is a long-term growth story.

"We remain bullish on the company’s long-term growth prospects in the hyperlocal delivery space as we believe it is well positioned to benefit from robust industry tailwinds such as improving tech penetration and rising income share of digitally native millennials and GenZ," said JM Financial.

The brokerage firm highlighted that the company's balance sheet also continues to be strong with net cash of ₹11,500 crore as of September 2022.

JM Financial underscored that over the medium term, the company expects food delivery to achieve adjusted EBITDA as a percentage of GOV of 4-5 percent, as its contribution margin as a percentage of GOV gradually moves towards 8 percent.

The brokerage believes the company has multiple levers to achieve this target, such as (1) further increase in restaurant take-rates, (2) further rationalisation of customer subsidies (delivery charges and discounts), and (3) operating leverage.

However, given the near-term growth concerns, margin improvement can be slower than earlier anticipated, JM Financial said.

Technical Views

Analyst: Vaishali Parekh, Vice President - Technical Research, Prabhudas Lilladher

The stock has been consolidating for quite some time, moving within a range between ₹60 and ₹70 levels just maintaining near the significant 50EMA (exponential moving average) levels.

The price has come very close to the significant 200DMA level of ₹66 and ahead only a decisive breach above the ₹70-73 zone shall indicate a breakout for a further fresh upward move.

At the same time, a decisive breach below ₹60-58 zone shall further weaken the trend and can trigger for further slide with the next major support visible near ₹42.

The RSI indicator is also moving sideways with no significant improvement and only a decent price movement above ₹72-73 zone with volume participation shall trigger a breakout.

Zomato tech chart

Analyst: Jigar S. Patel, Senior Manager - Equity Research, Anand Rathi Share and Stock Brokers

For the last three months, this counter has been moving in a range of ₹57-69. On November 11, 2022, it tried to break this range but failed and formed a bearish dark cloud cover pattern on a daily scale followed by an 18.5 percent cut in price from the high of ₹75.45.

On the indicator front, the daily MACD has formed a bearish divergence structure on the histogram as well as a signal line and MACD line. Anyone holding this stock can exit immediately. As of now, wait and watch for this counter.

Zomato Technical Chart

Overall, the stock appears to be suitable for a long-term bet. For the short term, as per analysts, one should play this stock cautiously.

Disclaimer: The views and recommendations given in this article are those of individual analysts and broking firms. These do not represent the views of MintGenie.

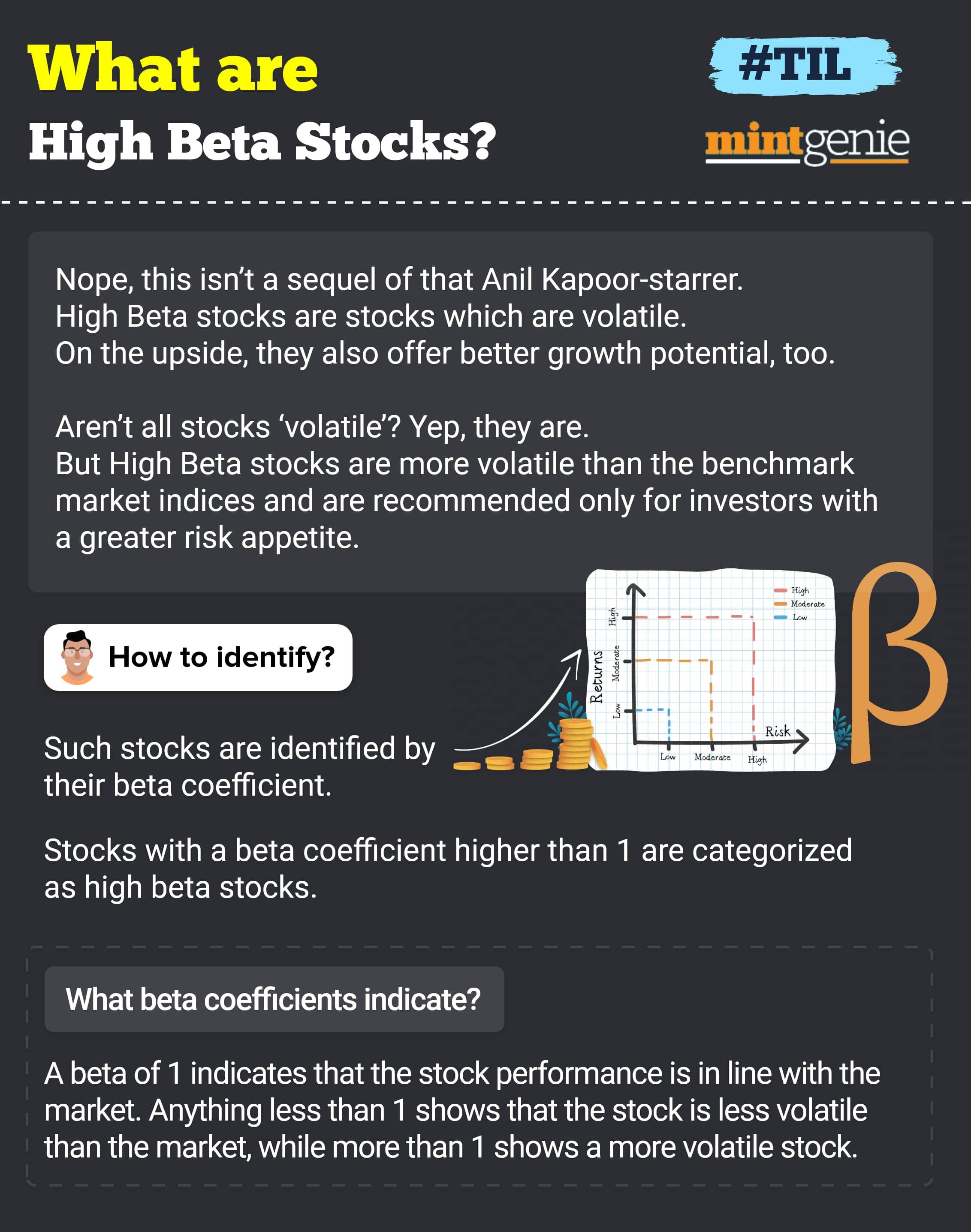

Understanding high beta stocks

First Published: 09 Dec 2022, 12:31 PM IST

Related Stories

infographics

India’s digital payments records 23 billion transactions worth ₹38.3 lakh crore in Q3

Team MintGeniemarkets

Yes Bank at 52-week high, rises over 13% in Friday's intra-day session; here's why

Dhanya Nagasundaram