Despite, a fall in the online food aggregator, Zomato Ltd profits during the third quarter of FY23, three brokerages are bullish on the stock and have recommended 'buy' rating as analysts believe the results somewhat are in line with the street's estimates.

The company reported a consolidated net loss of ₹347 crore for the quarter ended December, on the back of higher expenses and slowdown in food delivery business.

The total expenditure of the online food app jumped over 51% on year for the October-December quarter and stood at ₹2,485.3 crore versus ₹1,642.6 crore. Whereas, the food delivery's business' gross order value (GOV) growth in Q3FY23 grew by just 0.7% sequentially, in an otherwise seasonally strong quarter.

"We have seen an industry-wide slowdown in the food delivery business since late October (post the festival of Diwali). This trend has been seen across the country but more so in the top 8 cities," said the company in a press release.

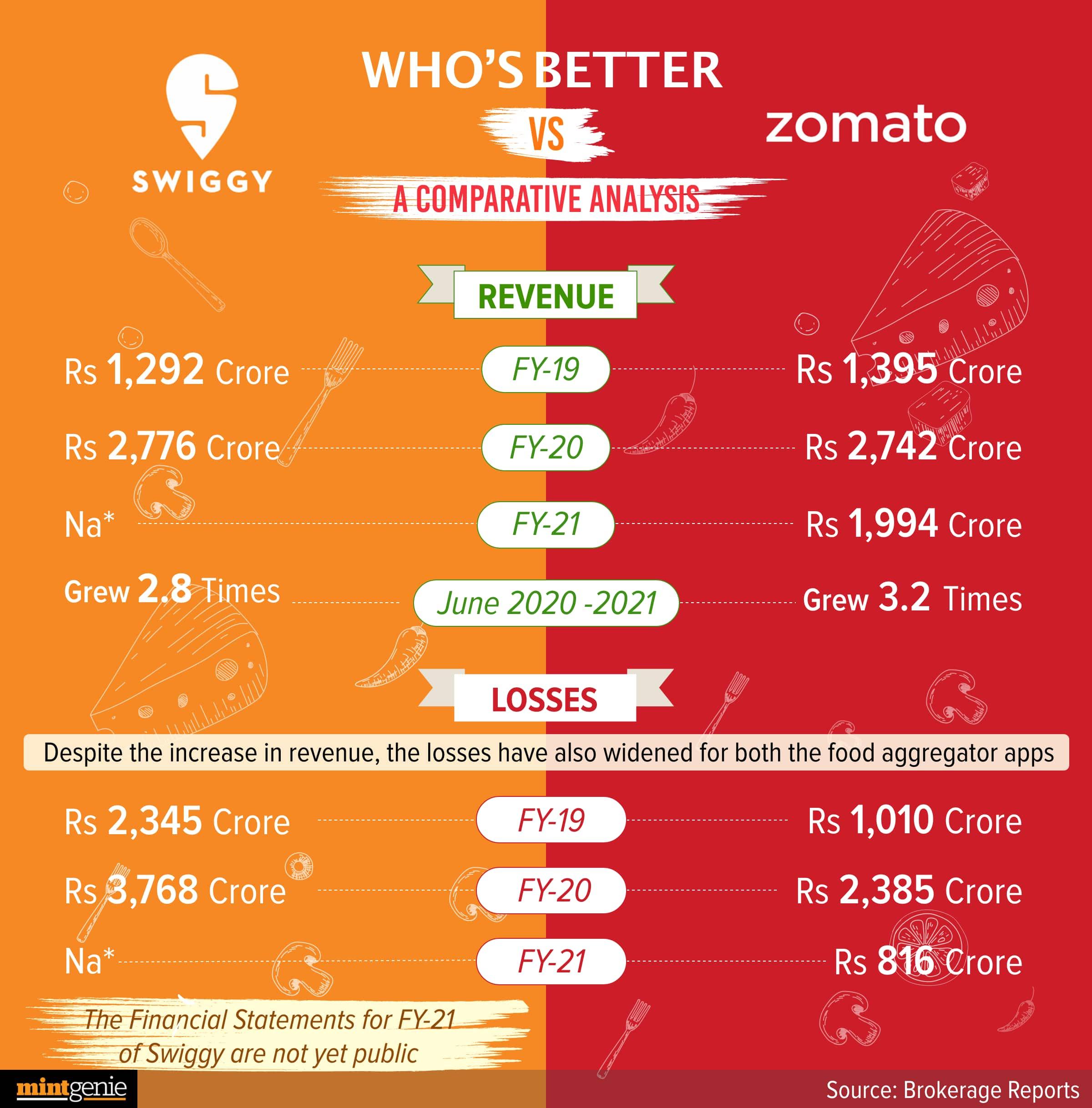

The company's consolidated revenue from operations during the December quarter under review stood at ₹1,948.2 crore. It was at ₹1,112 crore in the corresponding period a year ago. So far, since June 2020, the company posted the highest revenue so for in Q3FY23.

Brokerage Nuvama Wealth Management Ltd stated in its report that the company posted a better than expected Q3FY23 revenues, and the profitability was in line with brokerage's expectations.

Additionally, the brokerage thinks Blinkit's performance was positive given its 18% quarter-on-quarter (QoQ) growth in GOV and improvement in profitability.

The company acquired the quick commerce business Blinkit in August 2022. Hence, this quarter was the first full quarter of consolidation of Blinkit financials, as per company's exchange filing.

"GOV in food delivery was flat QoQ because of a decrease in monthly transacting users (MTU) with the closure of the Zomato Pro membership program, increase in dining out and boost in travel. While growth was impacted, contribution margin improved from 4.5% in Q2FY23 to 5.1% in Q3FY23," added the brokerage in its report.

Growth should return with Zomato's relaunch of its Gold membership program

Brokerage firms also expect that the company's relaunch of its gold membership program will further aid the business.

Zomato Gold, a brand-new membership program, was introduced by the company in late January. This program is the outcome of lessons learned over the previous few years, including modifications based on feedback from customers, restaurant partners, and investors. According to the business, the new model is more long-term for patrons, restaurant partners, and our profit and loss (P&L).

"We expect this program to drive loyalty and higher frequency of ordering going forward, and in less than a month, the Zomato Gold program has scaled to 900k+ members," said the company in its filing exchange.

Brokerage house, Kotak Institutional Equities expects Zomato Gold to be margin dilutive in the near term, nevertheless, this should spur growth in the medium run.

Similarly, Nuvama Wealth Management too believes the Zomato Gold’s relaunch to be a big boost to growth. However, the brokerage in its report said that all eyes would be on sustainable profitable growth.

Depending on execution-related gains, the brokerage expects the company to achieve profitability in Q4FY23 itself, two quarters ahead of its target.

Additionally, brokerage JM Financial Institutional Securities Ltd stated in its report that the management underlined that improvements in other revenue and fixed and variable cost drivers will offset the short-term negative impact due to the free delivery benefits of Gold membership.

"In the long term, it believes the program will turn profitable. It also noted that the program launch was several months in the making, so the investments towards the program were already baked in their projections and therefore they are confident of achieving the adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) breakeven target for the core business by 2QFY24," added the brokerage.