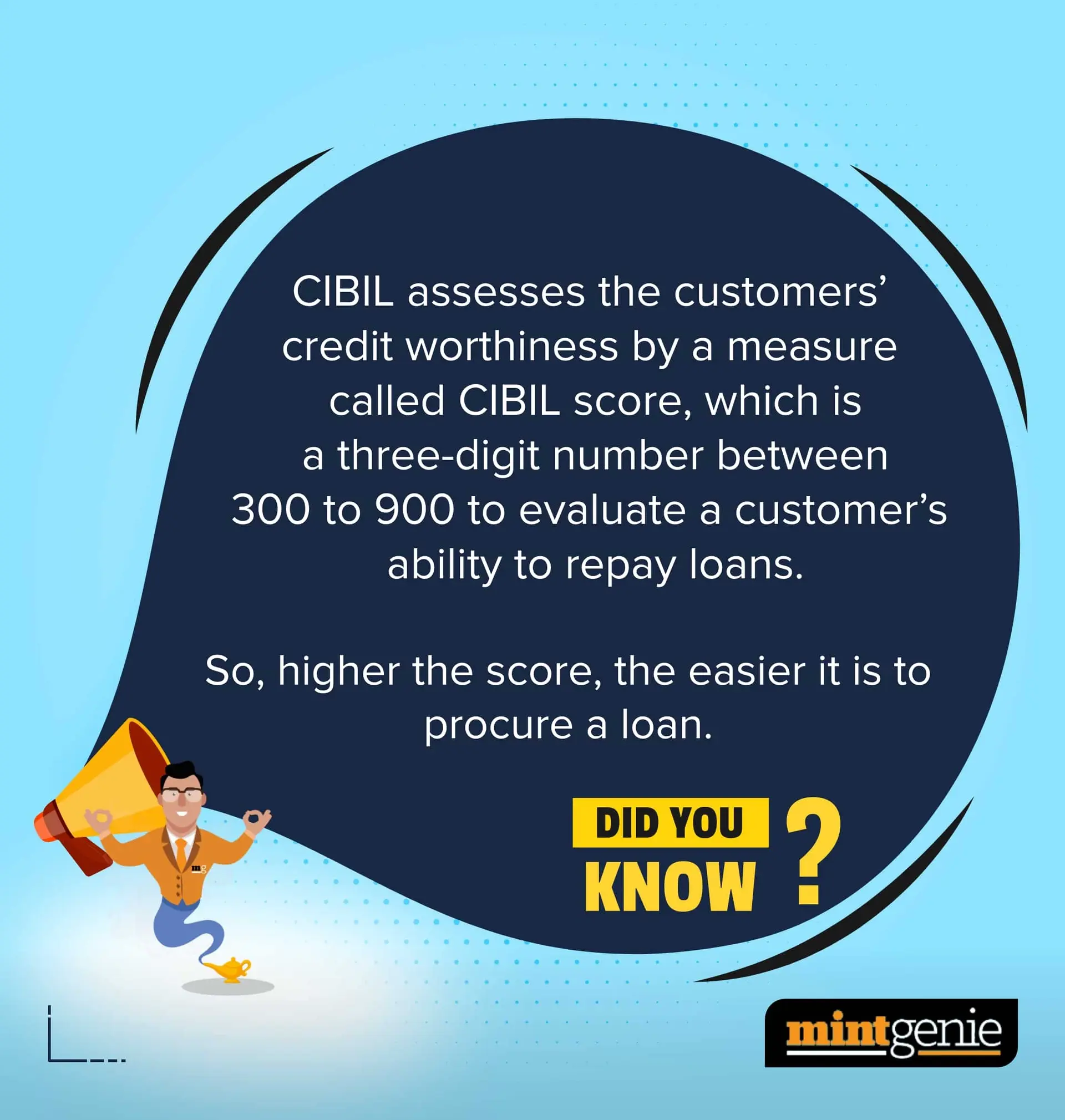

Our country has such a dearth of financial knowledge that even a simple term like CIBIL Score can cause many people to misunderstand and misconstrue it. How many are aware of the meaning of credit score that rates a consumer’s creditworthiness that underscores how interested lenders regard their potential borrowers? Your credit score can be between 300 and 850; the higher your credit score, the higher your eligibility to get credit cards or apply for a personal loan at lower interest rates.

The inability to interpret this term and assess its implications has given way to unwarranted myths that must be busted in the spirit of personal finance which occupies an important position in everyone’s lives.

Myth 1: CIBIL Score concept helps banks and fintech organizations only

This is a myth that has neither base nor reason to support its validity. As opposed to the CIBIL Score being useful to banks and financial institutions only, this score benefits customers by helping them use their credit properly so that borrowers are more careful with their finances.

Myth 2: CIBIL Score improves with your income

Indeed, the rich people living in posh colonies may have a higher purchasing power than you. However, this does not translate to a great CIBIL Score. It is a myth that securing a better job, an appraisal, or a higher payout will help you get a better score. This is wrong considering how your credit report is prepared based on the credit you have used and the frequency of your debt repayment. Credit score has nothing to do with your income or your job.

Myth 3: CIBIL Score is the only factor used to assess a loan application

Nothing could be more misleading than this misinformation as the CIBIL score is important in providing financial institutions with information about your credit history. However, this is not the only factor that is used by banks before deciding to accept or reject your loan application. Lenders obviously consider other factors too including your income, assets, investments, debts and more before deciding what to do with your loan application.

Myth 4: Taking a debit card builds your credit score

Next time, your friends or peers tell you that they took debit cards to build their credit score, be sure to tell them the difference between a debit card and a credit card. A debit card is simply a tool used to manage the funds in your bank account, independent of your credit history. Therefore, having a debit card does not affect your credit score, and using or applying for a card does not affect your credit history.

Myth 5: Zero credit helps

The myth of “Zero Credit” has done more harm than good as many people refrained from taking any loans or credit cards simply to maintain a “Zero Credit” record or history. Lenders look for people who make regular payments and who understand how to manage their credit limit. So, no credit history is also a red flag. As a result, no credit is not considered ideal.

Not many people are aware of the CIBIL Score concept nor are aware of their credit scores unless they are looking to apply for a loan or a credit card. Ignorance only worsens people’s understanding of these concepts that are necessary for our daily lives, thus, explaining the need to interpret them for what they are.