National Pension System (NPS) is an affordable, long-term retirement savings instrument that provides retirement income. Anyone between 18 to 60 years of age can invest in NPS.

NPS was started in 2004 by the government to help people build up a retirement corpus. This is being administered by the Pension Fund Regulatory and Development Authority (PFRDA), set up separately by an act of Parliament.

The popularity of NPS as a retirement saving option has increased over the past few years. After all, NPS offers attractive tax benefits.

At the end of the financial year 2022, the total number of NPS subscribers, including central, state government employees and others, stood at 1.57 crores, up 49% from 1 crore at the end of FY 2016-17.

But, before investing in NPS, you should make sure that NPS fits your retirement plans. There are several instances when you should not invest in NPS. So, here we list some of the individuals who should not invest in NPS.

1. You want to put all your money into equities

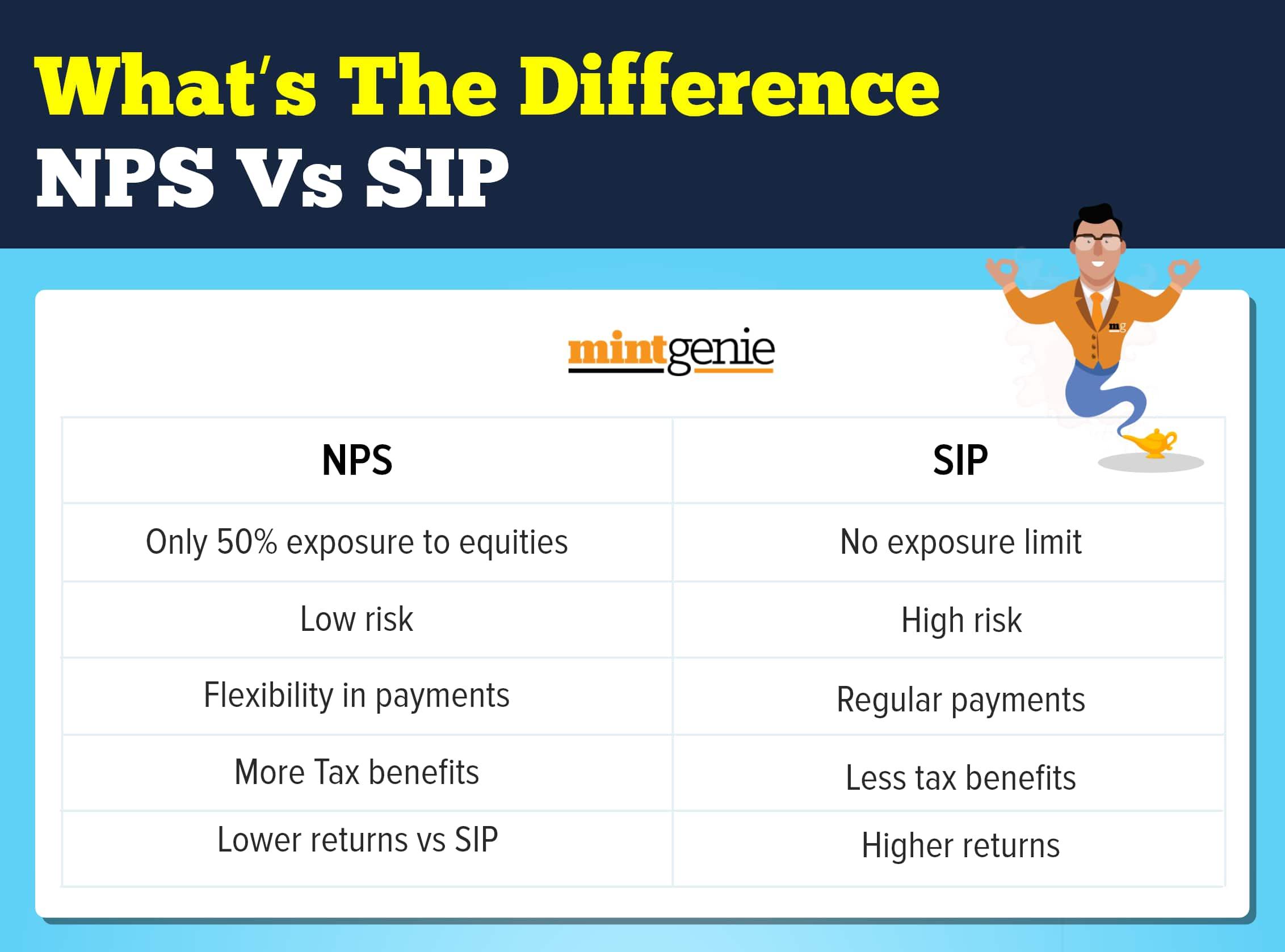

NPS offers the option to invest in different assets such as equities, corporate debt, government bonds and alternative investment funds(AIF). However, there is a cap on the percentage of the total portfolio that can be invested in equities. You can get a maximum equity exposure of 75% by investing in NPS. As per the rules, individuals up to 50 years can invest 75% of their portfolio under the Active Choice. Similarly, individuals opting for Auto Choice can have a maximum equity investment of 75% till 35 under the aggressive life cycle fund.

So, if you are an aggressive investor and want to invest a significant portion of your portfolio into equities, NPS might not be the best for you.

2. Don't want your money locked for a long time

NPS is a long-term savings plan that is meant to build up a corpus for post-retirement expenses. When you turn 60, you need to use at least 40% of the accumulated amount to buy an annuity plan that will work as a pension. The remaining amount is paid as a lump sum payment. This is the default option.

However, you can exit from NPS before turning 60. In this case, you will need to buy an annuity with at least 80% of their accumulated amount and the balance is paid as a lump sum.

So, NPS may not be a good option if you are not looking to keep your money locked for a long time.

3. Want a lump sum amount at retirement

As mentioned in the previous paragraph, you need to buy an annuity plan with the accumulated corpus. At retirement, you can get a maximum of 60% of your funds as a lump sum amount. Hence, if you want a lump sum amount after your retirement, you can look at other investment options that offer the facility to withdraw the entire amount in one go.

4. Don’t want a fixed pension

Under the NPS, after turning 60, the annuity provider gives you a fixed amount of money based on the interest rate at the time. If you want to use your savings for retirement the way you want, this retirement plan may not be for you.

5. Don't care about the tax benefits

NPS has a lot of tax advantages, and it can help cut down on your tax liability.

Under Section 80CCE, the total amount of deductions taken under sections 80C, 80CCC, and Section 80CCD(1) can be up to Rs. 1. 5 lakh. In addition, deduction of up to Rs. 50,000 is allowed under 80 CCD(1B).

Finally, you can get tax relief on your employer contributions to NPS. The tax benefit is capped at 10% of your salary (basic plus dearness allowance). This is above the Rs. 2 lakh investment limit that you can claim for a tax deduction. It is important to note that this tax deduction is available under the new and old tax regimes.

However, if you don't want to take advantage of tax breaks or have already chosen the New Tax Regime, NPS tax benefits won't help you.

The NPS has been a great initiative that has encouraged Indians to invest their hard-earned money for a stable future. However, just like any other investment option, it might not be for everyone. People who want a higher exposure to equities, a lump sum amount at retirement, don’t want to stay invested for a longer duration and don't want a fixed monthly income should not invest in NPS. Moreover, if you are not looking at any tax-saving incentives or have taken care of tax planning through other options, you might not feel NPS as an attractive option for your retirement planning.

Padmaja Choudhury is a freelance financial content writer. With around six years of total experience, mutual funds and personal finance are her focus areas.