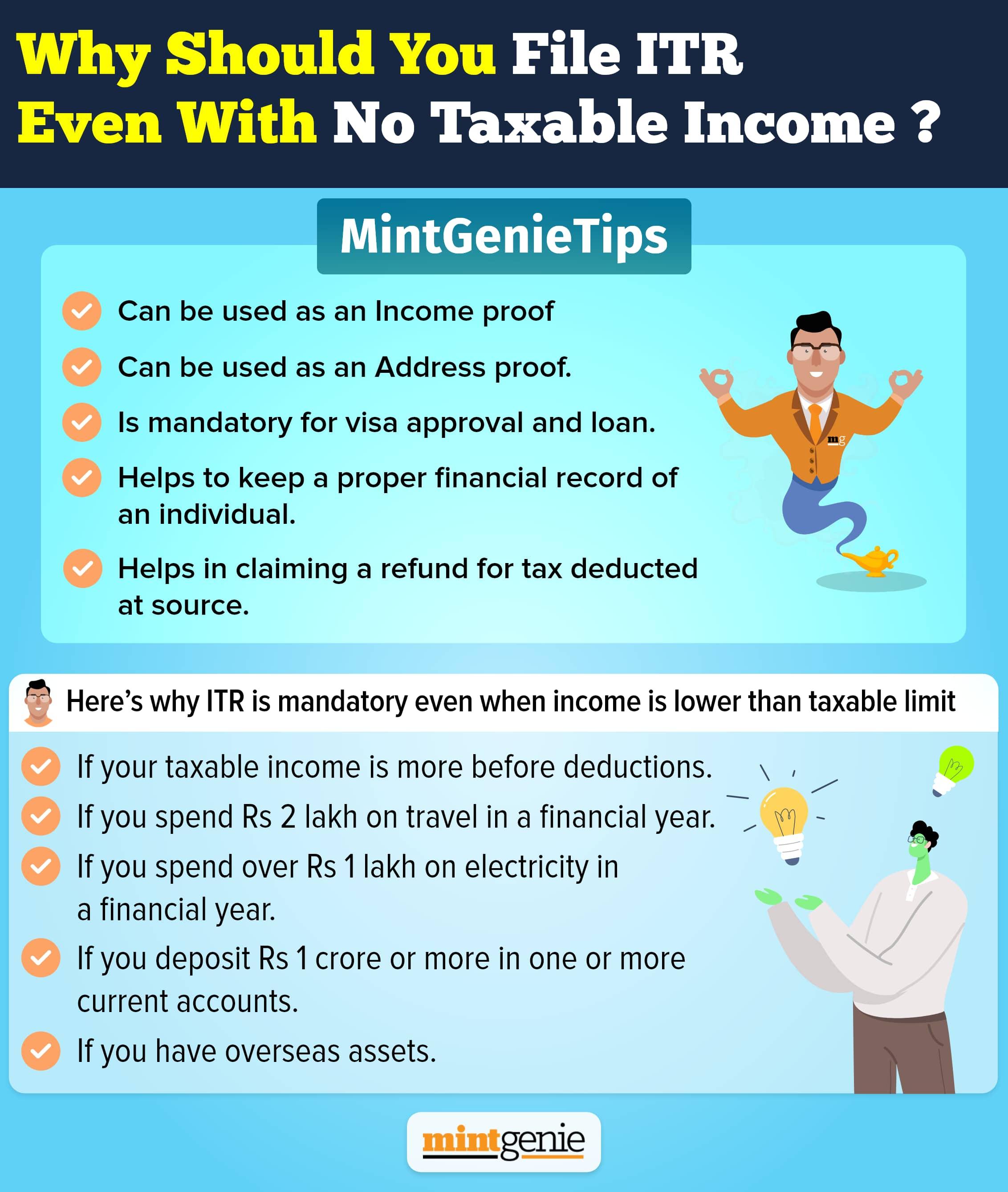

In today’s world, having a bank account has become crucial due to the multitude of advantages and conveniences it offers.

Maintaining at least one bank account forms the cornerstone of your financial transactions. Typically tied to your income, it serves as a hub for regular banking activities like salary deposits, bill payments, and everyday expenses. It is important for your primary bank account to be easily accessible, offering convenient services such as online banking, debit cards, and mobile banking apps, to ensure smooth and effortless transactions.

In the age of financial planning, many people maintain at least three bank accounts for saving, investment, and expenditure purposes.

There is no thumb rule that allows you to have more or less bank accounts as you age. Apart from a primary account, establishing a distinct savings account can prove advantageous. There are myriad reasons why you must opt for a separate bank account for your savings, some of which include:

- Organised finances: Arranging your finances according to your needs and purpose helps. Maintaining a distinct savings account separate from your primary checking account enhances financial management and oversight. It establishes a clear boundary between your regular expenditures and your savings, simplifying the tracking of expenses and safeguarding your savings from inadvertent usage. This segregation allows for improved control and visibility over your finances.

- Saving with a purpose: Having a dedicated savings account empowers you to allocate funds with precision, tailored to your specific financial goals. Whether you're aiming to save for a down payment on a house, a dream vacation, or an emergency fund, a separate account enables you to effectively monitor your progress and maintain an unwavering focus on your objectives. By having a designated account, you can track your savings growth and ensure that you remain on track to achieve your financial aspirations.

- Earning interest income: Who does not want to see growth in savings? By placing your savings in a separate account, you can capitalise on the potential interest rates offered by many savings accounts. This allows your money to grow gradually over time. With the advantage of compound interest, the interest earned on your savings gets reinvested, leading to even greater growth. By keeping your savings separate, you can leverage the potential of earning interest and witness your money steadily accumulate over the long term.

- Securing emergency funds: It is important to have a dedicated savings account specifically allocated as an emergency fund. This serves as a vital financial safety net, safeguarding against unexpected expenses or potential job loss. By segregating your emergency fund from your regular spending, you establish a distinct boundary that helps protect the funds for genuine emergencies. This separation guarantees that your emergency fund remains intact and readily available when truly needed, offering both peace of mind and financial stability during difficult circumstances.

- Disciplined savings: By maintaining a separate savings account, you establish a psychological boundary between your spending money and your savings, promoting discipline and discouraging impulsive expenditures. This demarcation is crucial for nurturing and maintaining a positive savings habit. The clear distinction encourages a focus on saving rather than indulging in unnecessary expenses, resulting in enhanced financial stability and the capacity to accumulate a significant savings balance gradually.

- A separate account for investment: Individuals with an interest in investing can benefit from maintaining a distinct investment account. This account can be seamlessly linked to your primary account, enabling effortless fund transfers and efficient investment management. It serves as a platform for engaging in activities such as purchasing mutual funds, stocks, or other investment instruments. By having a dedicated investment account, you can effectively track your investments separately and evaluate their performance with precision. This separation facilitates a comprehensive assessment of your investment portfolio and allows for informed decision-making.

- A separate account to manage foreign income: Maintaining a separate savings account to manage foreign income can provide valuable benefits. Firstly, it allows you to keep your foreign funds distinct from your domestic finances, enabling better organisation and tracking. This segregation reduces the risk of confusion or commingling of funds.

Fluctuating exchange rates can impact the value of your foreign income. By keeping it in a separate savings account, you can closely monitor exchange rate trends and choose the optimal time to convert your funds into the local currency. This approach helps maximise the value of your foreign income.

Furthermore, a dedicated savings account for foreign income streamlines tax reporting and compliance. It ensures you maintain a transparent record of your foreign earnings, simplifying the calculation and reporting of any applicable taxes and meeting the reporting requirements of your home country.

Lastly, managing foreign income often requires unique financial planning considerations. By utilising a separate savings account, you can effectively evaluate the contribution of your foreign income to your overall financial goals and customise your financial planning strategies accordingly.

How many bank accounts should you have?

The number of savings accounts you should have in your name depends on your individual needs and preferences. There is no specific rule or prescribed number of savings accounts that applies to everyone. It ultimately comes down to factors such as your financial goals, lifestyle, and personal financial management strategies.

While some people may find one or two accounts to be sufficient, others might benefit from having multiple accounts tailored to specific requirements. It ultimately depends on your personal circumstances and your ability to effectively manage multiple accounts and funds. Additionally, it is important to be aware of any charges and minimum balance requirements associated with each account to avoid potential penalties.

Many people are tempted to open new savings accounts to avail of some temporary benefits. This may create problems in the long run as you face the arduous task of maintaining and securing details of all bank accounts while ensuring to keep the minimum balance in each of them.

Most importantly, ensure that you have savings bank accounts in recognised and reputed banks to prevent usurping of the money set aside in your bank savings accounts and fixed deposits.