The new tax regime that was introduced in Finance Act 2020, got tweaked in the annual Budget FY23 and the general commentary around it has created an impression that this is likely to become more permanent in nature, eventually replacing the current old tax regime.

Calculations are all around the enhanced tax rebate threshold that comes with the new tax regime and the fact that many individual taxpayers will benefit especially if their income is up to ₹7 lakh a year. At the moment, both the old and the new tax regime are in play and you can choose which one to apply while filing your tax returns.

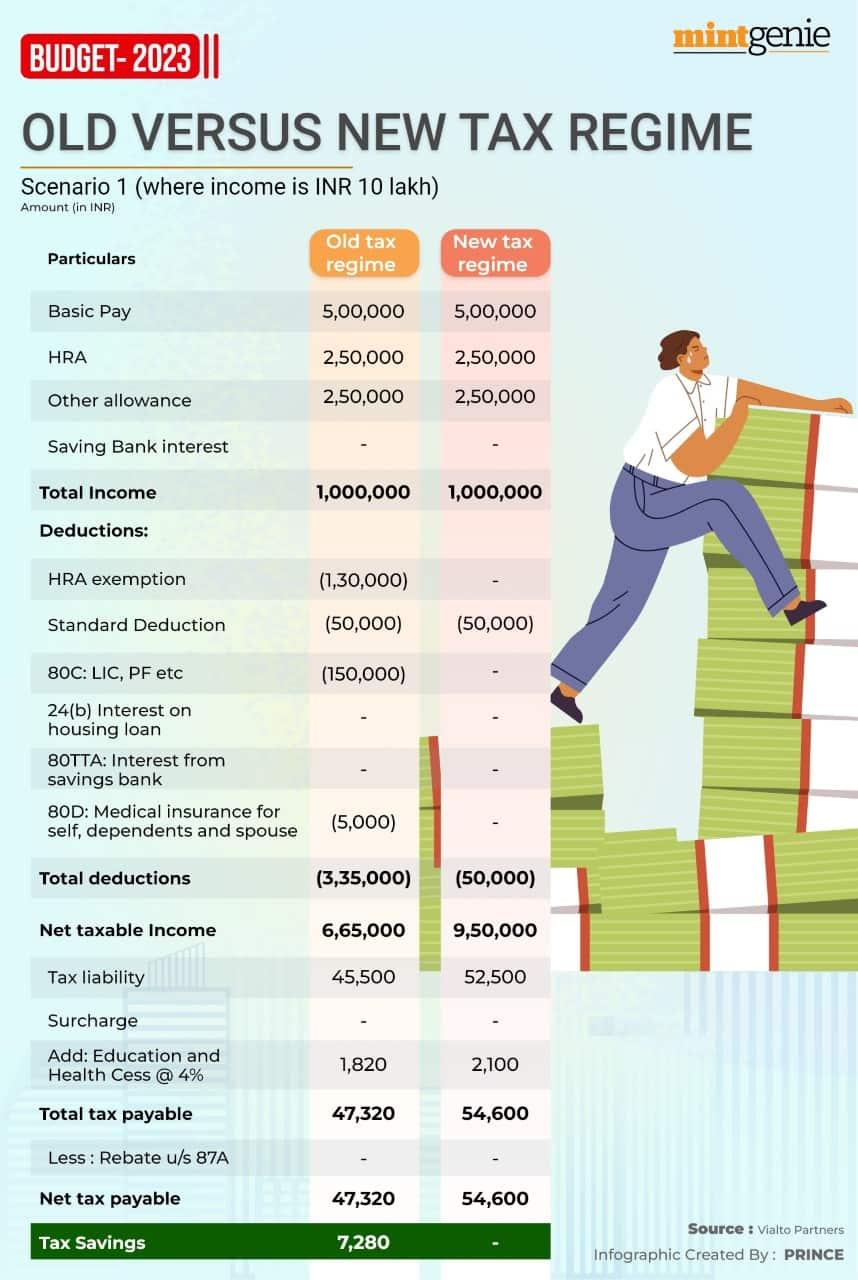

The difference in the two regimes also lies in the deductions you are allowed to make from your taxable income by way of investments. The old tax regime permits you to deduct up to ₹1.5 lakh across various tax saving investments (including tuition fees paid for your child), an additional ₹50,000 for investments in National Pension Scheme, up to ₹2 lakh for interest payment of home loan, up to ₹50,000 for parents medi claim premium and ₹25,000 for self. Then there are other deductions like leave travel allowance, house rent allowance and donations.

All these put together, not only reduce your overall tax payable but also help you save for the future by utilising the deductions completely.

The new tax regime has no such provision, what is not taken up as tax comes as cash in hand. There are no deductions and hence, as some experts have opined, no forced savings.

The Finance Minister in this year’s budget said that the new regime was to become the default regime. Which means that if you don’t make a choice, it’s assumed that you are picking the new regime. If and when it will move from default to the only regime is anyone’s guess. Nevertheless, the popular assumption is that it could happen sooner than later.

The number game aside, what does this change really mean for your money?

Is choice being narrowed or expanded?

One way to consider this change is to think that your choice is being narrowed. You can no longer opt for ‘forced’ savings and accumulate wealth for the future. The other, more practical money management perspective is to consider it an expansion of choice, which is now devoid of the tax efficiency limitation.

Accepting this change, however, is not just a matter of choice, it’s also about changing behaviour.

When our minds perceive that the choice is missing, you do what you have to. Under the old tax regime, you are ‘forced’ to save because, hey, what’s the choice? If you don’t save, you’ll just pay more tax. Who wants to do that?

But in this bid to save tax, you may also be ‘forced’ to make subpar investment choices, like buying traditional insurance plans, for tax deduction on premium paid.

On the other hand, given a choice (as the new regime does), you have the ability to make investment choices based purely on merit. That is if you don’t spend what is left over after tax.

The confusion arises because, the choice in the old regime was save or pay tax, whereas in the new regime it’s save or spend. The human mind abhors paying tax, which by definition is a levy, whereas spending your money is what you are meant to do. It’s not hard to see the choice our basic human behaviour will arrive at in both cases.

In reality, the new tax regime is telling you to grow up by leaving all the choices in your lap. It needs you to stop being lazy about your money decisions. Rather than just tax saving, do your homework around risk-return balance, cost, transparency, liquidity and flexibility when choosing investments for your future financial security.

Using this expanded choice, will work out only if you make a conscious effort to understand your options better. This is not an easy task.

What should you do?

Step one involves overcoming behavioural lethargy of making the easy choice, instead working towards making the right choice. This requires you to step back and look at the canvas of your personal finances with objectivity.

One way is to do your initial one time homework around which type of investments will help you the most in creating long term wealth and automate your investment in such securities. Systematic investment plans in equity stocks and mutual funds are a good way to start.

These are long term investments, which can be automated as per a frequency you define. For the debt portion of your portfolio, you can do the same with debt mutual funds or start a monthly recurring deposit with a bank, again both these automated choices; you don’t need to act on them each time.

Pencil in a minimum investment in Sovereign gold bonds for each issue that gets launched, if gold is your investment of choice. Fix a date for an annual review and reset the automation each year. Thus, after the initial work, automation ensures that you can get lazy again for an entire year before you review the choices.

If you are not the kind to take the reins in your hands or if you prefer outsourcing the tax saving investments to your chartered accountant , then outsource the task of your new merit based portfolio too. Except you don’t need a tax expert for this, look for an investment expert who can help you create, maintain and review a portfolio of suitable long term investments aligned with your life objectives.

The old tax regime nudges us to take the easy way out with ‘forced’ savings. The new tax regime, instead is nudging us to be aware and focus on taking the smarter way forward towards our future financial security.

Lisa Pallavi Barbora is a financial coach and founder of moneypuzzle.in