Q. I am a 31-year-old salaried professional working at a state government PSU. I have been filing taxes under the old tax regime since I started earning, I now understand that at present there are two tax regimes in operation concurrently. In the recent budget a number of changes were introduced in respect of the new tax regime. Can you please elaborate on the new tax regime and if there are any exemptions or deductions available for salaried individuals under the new tax regime.

Jagteshwar Sahni, Indore, Madhya Pradesh

At present in India, there are two tax regimes which are concurrently operational. The taxpayers have been given the option to choose either tax regime at the time of filing tax. The new tax regime was introduced in the financial year beginning on April 1, 2020 (FY 2020–21), through an amendment to the Income Tax Act, a new section 115 BAC was added. Section 115 BAC introduced lower tax rates for individuals as well as for Hindu Undivided Families (HUFs).

However, the new tax regime was not very popular amongst the general public, most individuals continued filing their income tax returns under the existing tax regime / old tax regime. The biggest reason behind the unpopularity of the new tax regime in spite of the low tax rates was the removal of almost all the tax exemptions which were available under the old tax regime. Below is an indicative list of tax deductions and exemptions:

Exemptions

- House Rent Allowance

- Leave Travel Allowance

- Mobile and Internet Reimbursement

- Food Coupons or Vouchers

- Company Leased Car

- Uniform Allowance

- Leave Encashment

Deduction

- Equity Linked Savings Scheme (ELSS)

- Employee Provident Fund

- Public Provident Fund

- Children Tuition Fees

- Health Insurance Premiums

- Investment in NPS

- Life Insurance Premium

- Principal and Interest Component of Home Loan

- Tuition Fee for Children

- Saving Account Interest

Under the new tax regime there are only a limited number of tax exemptions/deductions available for the tax-payer. Following is a brief summary of the tax deductions/exemptions available under the new tax regime:

National Pension Scheme: Section 80CCD (2) of the Income Tax Act, provides tax deduction for contributions made by employers on behalf of employees towards their NPS Tier-I accounts. This tax deduction is available under both the old tax regime and new tax regime.

However, it is important to note that the maximum tax deduction an employee can claim under Section 80CCD(2) is capped at 14% for central government employees and 10% for state government and private employees.

Standard Deduction: Section 16(ia) of the Income Tax Act, permits a flat deduction for salaried individuals up to a limit of ₹50,000 known as the standard deduction. In the 2018 Union Budget, standard deduction was introduced for the first replacing the tax-deductible medical and transportation allowances of ₹19,200 and ₹15,000, respectively. At that time standard deduction was capped at ₹40,000.

The Union Budget for 2019 changed the Section 16 standard deduction limit in order to give salaried people greater tax relief. The deduction amount was increased from the previous cap of ₹40,000 to ₹50,000. Uptill now only the salaried individuals opting to file their tax under the old tax regime were eligible to claim standard deduction. However, pursuant to the Budget 2023, the central government has now allowed even individuals who are filing tax under the new tax regime to claim standard deduction under Section 16(ia).

Income Tax Rebate: The Indian government first introduced income tax rebate under the 87A rebate in the 2003 Budget. This rebate aids in lowering taxpayers' income tax obligations. Any resident individual can claim rebate under Section 87A, the only prerequisite to receiving the benefit is that the taxpayer should be an Individual resident and the threshold limit specified under Section 87A shall not be exceeded by your total taxable income.

This cap is set at Rs. 5,00,000 for the Financial Years (FY) 2021–2022–2023 [Assessment Years (AY) 2022-23–2023–2024]. This means that anyone with a total taxable income of more than Rs. 5,00,000 will not be eligible for the tax rebate provided under Section 87A, and their tax will instead be computed at the standard rates.

The rebate under section 87A was increased to ₹7 lakh from ₹5 lakh under the new tax regime in the Union Budget 2023–24. Pursuants to the amendment to the Income Tax Act introduced vide the Finance Act, 2023, any persons who earn less ₹7 lakh would be eligible to claim tax rebate under Section 87A and consequently have nil tax liability.

Conclusion

The biggest attraction of the new tax regime is not the deduction available under but the low tax rate applicable to different tax slabs relative to the tax rate applicable under the old tax regime. However, one should not jump to the new tax regime solely because of this, there are a number of tax benefits available under the old tax regime which one can use to reduce this tax liability.

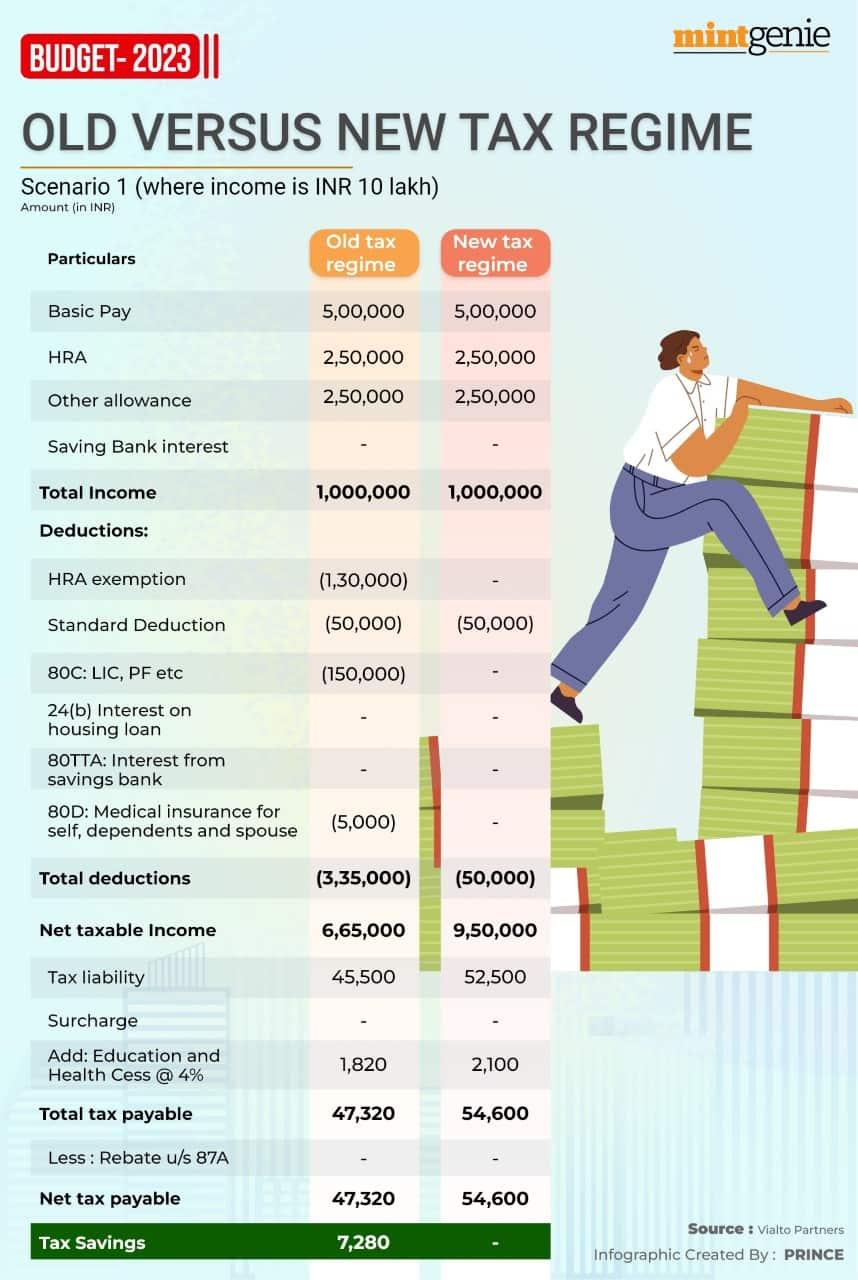

All individuals should assess their tax liability with the help of an expert and determine which tax regime is more beneficial to them. For instance a person earning ₹10 Lakhs who has a house loan, as contributes to ELSS mutual funds and has availed medical insurance may save more under the old tax regime because of the tax deduction available for house loan, tax free investment and medical insurance under the old tax regime.

Kuvera is a free direct mutual fund investing platform.

Note: This story is for informational purposes. Please speak to a financial advisor for detailed solutions to your questions.