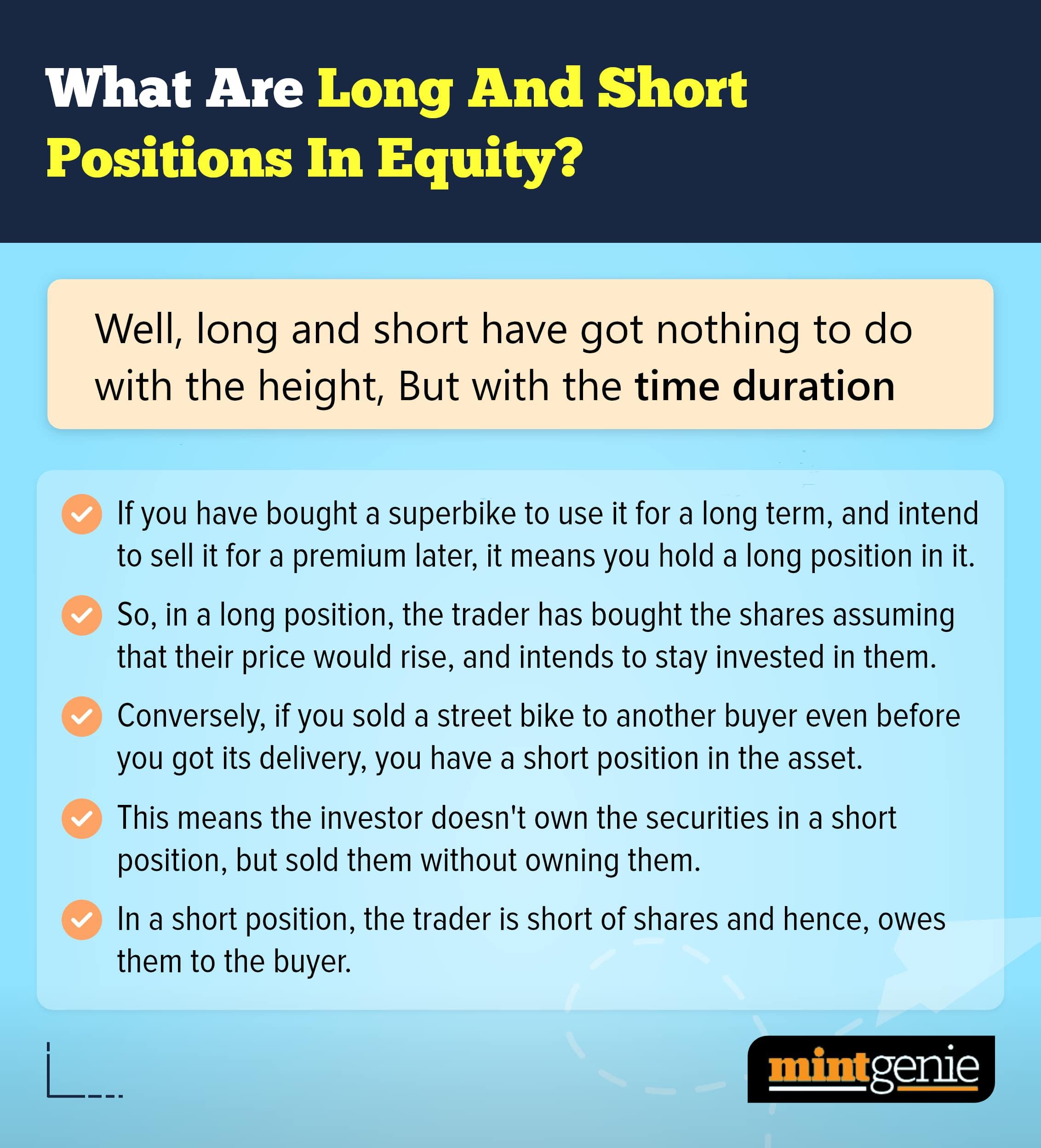

When you change from one plan of a mutual fund scheme to another (e.g., regular to direct), this is considered a ‘transfer’ as per the Income Tax Act. Consequently, you are liable to capital gains tax. It does not help that the funds are saved in the same mutual fund scheme.

However, this could change if this recommendation of Association of Mutual funds in India (AMFI) is accepted in the Union Budget 2023.

What is the background?

If an investor buys units in one plan (direct) of a mutual fund scheme and decides to shift to another, this shift – despite being invested in the same fund scheme – is considered a transfer of assets.

In other words, the Income Tax Department calls it a ‘sale’ and hence, it is subject to capital gains tax.

Therefore, fund houses want this to be changed so that investors are not liable to pay capital gains tax on the same.

“Switching of investment in Units within the same Mutual Fund scheme from Growth Option to Dividend Option (or vice versa), and/or from Regular Plan to Direct Plan (or vice-versa) is considered a “Transfer” under Sec. 47 of the Income Tax Act, 1961 and is liable to capital gains tax, even though the amount invested remains in the mutual fund scheme,” AMFI said in a statement.

There are no realised gains, as the underlying portfolio remains unchanged within the scheme.

Different rule for ULIP

While invoking a similar precedent, the mutual fund body argues that switching of investments from one investment plan to another within the same Unit Linked Insurance Plan (ULIP) of insurance companies is not considered a sale, and hence not subjected to any capital gains tax.

So, when the investor-friendly principle is followed in case of insurance investor – why is it not followed for the mutual fund investors?

Aside from this, there are several other Budget proposals of the mutual fund industry.

These include reducing the time period of debt-oriented mutual funds from the existing 36 months to 12 months for capital gains tax purposes.

The rationale behind this is that the sale of listed bonds and government securities is considered LTCG (long term capital gains) when it takes place after holding it for 12 months, whereas this period is 36 months in case of debt-oriented mutual funds.

Akhil Chaturvedi, Chief Business Officer, Motilal Oswal AMC, believes that it would be an excellent provision if allowed since investors would be able to move between asset classes and manage their allocations between schemes.

“It has long been demanded to allow this and bring mutual funds on par with ULIPs, which allow switching between plans from the same insurance company without being taxed,” he said.