For a considerable segment of our population, the desire to own a home has been a cherished dream. Homeownership not only instills a sense of pride but also offers financial security. The BankBazaar “Aspiration Index for 2023” reaffirms the enduring significance of this aspiration, despite the substantial hurdles that potential homebuyers confront. These challenges encompass the intricacies of obtaining financing and the arduous path toward realising their ideal home.

BankBazaar evaluates the aspirations of individuals from urban and non-urban areas across five overarching categories: Wealth, health, relationships, fame, and personal growth. Past data, as well as current insights, consistently demonstrate that owning a home continues to be a primary aspiration and a pivotal financial goal.

When considering the top five aspirational objectives, purchasing a house holds the third position in significance among Indians. Remarkably, women demonstrate a heightened desire for homeownership, primarily motivated by their pursuit of financial security and the long-term safety of both themselves and their families. Their dedication to this goal surpasses that of men.

Another noteworthy objective identified in the study is the desire to live close to immediate family, marking the second most significant goal in terms of readiness. It trails only behind the aspiration for mental well-being and health.

In the past, prospective homeowners typically waited for an extended period, depending on their savings to accumulate the confidence needed for property purchases. Nevertheless, this waiting period has considerably shortened due to the convenient availability of home loans from banks and other financial institutions. These loans are accessible to eligible individuals with stable incomes and favourable credit scores.

Assessing BankBazaar’s data

Within the context of the desire for homeownership, a noteworthy impediment arises - specifically, the escalating cost of living driven by inflation and rising interest rates. According to BankBazaar’s data, 26 per cent of individuals have reduced or forsaken some of their aspirations, while a striking 56 per cent have delayed their dreams by six to 18 months or even longer, including their ambition of owning their own home.

The data also highlights that a substantial portion of Indians are taking loans to acquire assets like homes, among other things. This pattern endures despite the decreasing affordability of housing in major cities, which is a result of soaring property prices and slower income growth. It underscores the significance of housing as a priority, even in the face of challenges posed by inflation.

Although real estate demand may ebb and flow in response to economic trends affecting potential homebuyers, homeownership will persist as a lasting and essential aspiration for Indians.

More home loans being sought

The rise in property prices and interest rates might have dampened buyer sentiment, but the escalating numbers of housing loans and property sales paint a contrasting picture of the real estate market in India.

As per RBI data, the all-India house price index (HPI) achieved its highest year-on-year increase in the last seventeen quarters, reaching 4.6 per cent in Q4 2022-23. On a quarterly basis, the HPI has consistently risen over the past year, showing an additional 0.6 per cent increase in Q4. Moreover, during Q4 2022-23, house sales surged by 21.6 per cent, and new property launches continued to demonstrate robust growth, indicating strong demand from both end-users and investors.

Over the past 11 years, the proportion of residential housing loans within the overall loan portfolio has grown, reaching 14.2 per cent in March 2023, up from 8.6 per cent in March 2012. The banking system’s total exposure to the real estate sector amounted to 16.5 per cent of total loans as of March 2023. These loans are secured, and due to loan-to-value (LTV) ratio regulations, the default rate remains below two per cent. The post-pandemic era has witnessed a robust demand for houses, driven in part by the desire for increased personal space and larger living areas.

Aspiration for homeownership continues

Repeatedly, data indicates that owning a home remains a prevalent aspiration, with a significant number of Indians, particularly women, prioritising homeownership over men. It stands as a primary financial objective, even though it necessitates long-term financial discipline and planning.

| India’s top 5 aspirations by Aspiration Index | ||||

Rank | Aspiration | Male | Female | Total |

1 | To be mentally healthy and happy | 89.7 | 88.6 | 89.1 |

2 | To save & invest money to provide my children with the best education in life | 88.9 | 87.9 | 88.9 |

3 | To buy a house of my own | 88.7 | 87.8 | 88.2 |

4 | To be able to maintain a nutritious diet | 88.3 | 85.5 | 86.9 |

5 | To live near my immediate family | 87.3 | 86 | 86.6 |

| Data: India’s top aspirations, 2023 BankBazaar Aspiration Index | ||||

Proximity to immediate family members has gained significance for Indians, and owning a home can facilitate the realisation of this aspiration. It affords them the opportunity to concentrate on other vital goals, including mental well-being, children’s education, or initiating a business.

Should you buy a house or live on rent?

You cannot be deemed to have settled down unless you have bought your home, and this association is understandable. Yet, considering the significant financial implications, it’s crucial to take a more practical approach to our financial capabilities.

The debate between buying and renting a home might seem inconclusive. Rather than being a matter of right or wrong, it largely boils down to a matter of personal preference and financial capacity.

The debate over whether to buy or rent a house often revolves around the notion of why pay rent when you can pay EMI and acquire an asset. This is the primary argument put forth by individuals who aim to persuade you to become a homeowner, whether it’s your parents, friends, or financial advisor. At first glance, this argument appears reasonable, as the value of a house tends to go up while rental payments do not contribute to ownership. However, upon closer examination, a significant flaw becomes evident. The main culprits behind this flaw are the exorbitant cost of real estate in India and our approach to home buying.

When you have the cash readily available: Being prepared with approximately 30 per cent cash for a down payment signifies financial readiness for homeownership. Having this minimum cash reserve enables you to secure the remaining funds through borrowing. The out-of-pocket expenses can be either upfront or spread out over time.

When you qualify for a home loan: A credit score exceeding 750, in addition to a consistent income and an extended employment history, positions you as an appealing borrower to lenders and makes you eligible for lower interest rates. Ideally, aim for a score of 800 before seeking a loan.

When you’re prepared to commit for the long term: Embracing homeownership indicates your readiness to invest not only financially but also emotionally in a property, as opposed to viewing it as a short-term venture. The financial advantages become more favourable over the long term.

When you’ve pinpointed your choices: Once you’ve conducted thorough research on the housing market in your preferred location, ensuring it aligns with your lifestyle and financial goals, you may find that attaining the perfect option can be challenging. Your aim should be to secure an option that is “good enough”.

When the property is legally sound: Make sure that the property you’re purchasing possesses the essential legal clearances, clean titles, and is free from disputes. Consider hiring a property lawyer to thoroughly examine the documents. While it incurs an extra expense, it offers peace of mind.

Adhil Shetty, CEO, BankBazaar said, “When you have the cash, the loan eligibility, have identified a suitable property, and are ready to commit to it for the long-term, you’re ready. Till then, rent.”

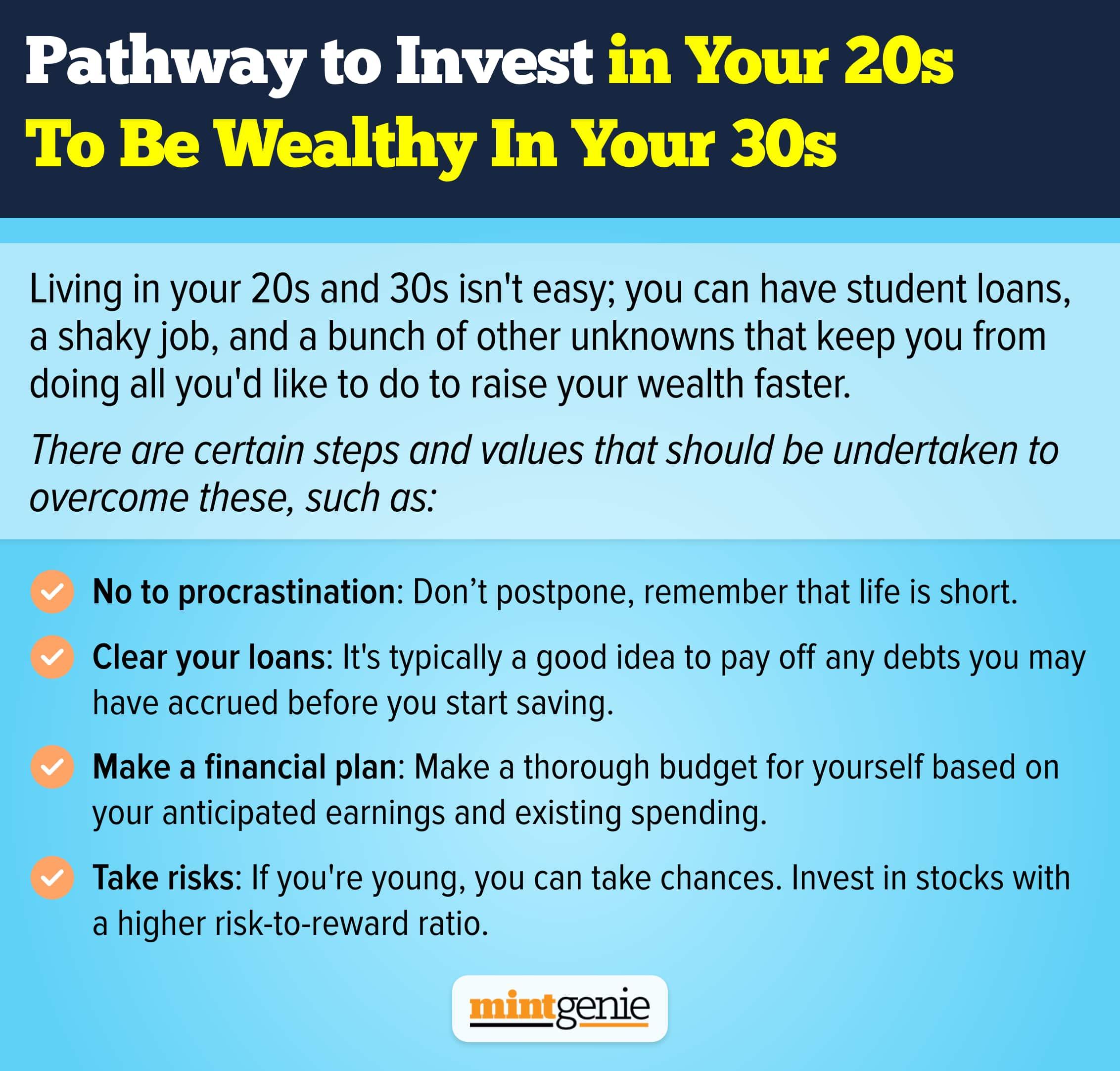

How to amass money to buy your home?

Purchasing a home is a significant lifelong investment, potentially the largest one you’ll ever make, especially in India. Are you concerned about not being able to accumulate sufficient savings for your own home? It’s indeed a major milestone, well worth the sacrifices and diligent saving. Owning your own home is among the most significant accomplishments for an ordinary individual. Fortunately, with banks competing for customers, there are currently excellent home loan deals available in India, making the home-buying process more manageable.

Nevertheless, it’s important to remember that you still need to save for the down payment, as home loans in India typically cover only around 80 per cent of the total cost. Let’s explore some strategies for saving money towards owning your own home.

Deciding the required savings amount: A loan can typically cover 75-90% of the total amount, which includes the base price, GST, amenities, and utilities. The remaining expenses, which can account for 35-50 per cent and encompass significant costs like registration, stamp duty, and furnishing, are typically not financed by the home loan. As buyers approach retirement, their loan tenures tend to be shorter. Older buyers typically have accumulated savings, which may result in a larger upfront payment requirement, exceeding the range of 35-50 per cent. This surplus amount can be set aside for long-term investment opportunities. The remaining cost can be covered by a home loan, depending on the borrower’s eligibility.

Accumulation through equity or traditional investments: The major decision during home planning is deciding how and where to save money for the same. Some people are averse to inherent market risks, thus, explaining their proclivity to traditional bank deposits like fixed deposits (FDs), recurring deposits (RDs), savings accounts, and fixed income plans issued by various fintech organizations. Some also resort to debt funds to benefit from the interest rates on bonds and other investment options that promise fixed returns in the long run.

The FDs or RDs offered by commercial banks or post offices represent secure choices for safeguarding your savings while earning moderate returns. These investments can be easily accessed and converted into cash when needed. Additionally, AAA-rated company deposits can be valuable, but it’s important to review the terms regarding lock-ins and potential pre-closure penalties.

Equities have historically generated significant real returns over extended periods, making them an excellent choice for long-term objectives like retirement planning. If you’re postponing your plans to purchase a home, it’s advisable to include equities in your investment portfolio to potentially achieve higher returns. As you approach your capital protection target, it’s crucial to gradually transition towards debt investments in a systematic manner.

Short-term mutual funds like overnight funds and liquid funds primarily allocate their investments to money market instruments. These funds offer a lower level of risk and are more suitable for short-term savings compared to equity funds, which can exhibit higher volatility. It’s important to note that risks do exist. Unlike FDs, these funds do not promise or advertise specific future returns.

Long-term debt savings vehicles like the Employees’ Provident Fund (EPF) are primarily designed for retirement planning but can also be utilised to facilitate home purchases. Eligible subscribers have the option to withdraw as much as 90 per cent of their savings for home construction or acquisition. However, it’s important to ensure that such withdrawals do not jeopardize your long-term retirement financial goals.

As Lovaii Navlakhi, CEO, International Money Matters rightly shared, “In the short term, ensure the investment is not subject to market volatility. Stable assets like arbitrage funds or FDs work. For the longer term, invest in equity funds as per your risk profile. Reduce the equity exposure when near the goal.”

Occupation or investment?

Not all deem real-estate investments with the same view. Some buy a house to live in with their families whereas others buy property for their investment value. To shift to a property and occupy it is debatable and no specific data or statistics point out the validity and effect of any of these decisions regarding property purchase.

The decision to view and use a property for self-occupation or as a pure investment depends on myriad factors including demand, supply, location, price, size of the property, inflationary trends, and many more.

When purchasing a home for your own residence, the primary focus should be on whether the house fulfills your family’s immediate requirements. This decision is often driven by emotions rather than financial returns, and the mathematical aspects take a back seat in this context. However, when acquiring a property solely for investment objectives, the foremost consideration is the potential returns it can generate. These returns can come from both market appreciation and rental income.

The information sourced from the House Price Index published by the Reserve Bank of India (RBI) reveals that over the past decade, returns on house prices have been on par with those from a fixed deposit account. Multiple industry reports indicate that net rental yields, which represent rental income as a percentage of the property’s price, are three per cent or lower in several Indian real estate markets. The net rental yields, which account for maintenance expenses, taxes, and loan interest, frequently turn negative in the short term.

The decade-long performance data for 10 major markets analysed through the RBI’s House Price Index reveals that real estate investments do not exhibit favourable returns when compared to other investment avenues. Both price returns and rental yields, prior to accounting for maintenance costs, taxes, and loan interest, have shown negative trends in the short term. Moreover, when considering ‘real’ returns, which account for inflation at a rate of six per cent during this period, they have often been negative in many cases.

However, the above data is of variable nature considering how rental yields differ between markets and from one investor to another. If the idea of buying and owning a house is self-occupation, the income from rental yields does not matter as these would be viewed as an added and unnecessary income in the long run. However, if one invests in a house to earn from rental yields, numbers suggest a better income opportunity when the money is invested in equities, debt, and gold investments. Even traditional bank deposits like fixed and recurring deposits now promise higher return rates than the available rental yield, when compared in percentage terms.

Risk inherent in real estate investments

Investing in housing is a financially demanding commitment that can put significant strain on a household’s finances and savings in the near term. Additionally, housing is considered an illiquid investment because it cannot be readily converted into cash. In comparison, financial investments like mutual funds or fixed deposits offer greater liquidity in this aspect.

Considering the surplus of housing inventory, including both completed and ongoing construction, these patterns are unlikely to undergo significant changes. Returns from housing investments are anticipated to remain unpredictable. Hence, for individual retail investors, real estate poses various risks, and the potential for positive rental yields may only materialise through extended periods of ownership.

As a result, for the majority of investors, the most suitable purpose for purchasing a home tends to be self-occupation. Wealth accumulation can often be achieved more effectively through investments in mutual funds, provident funds, debt instruments, and equities.