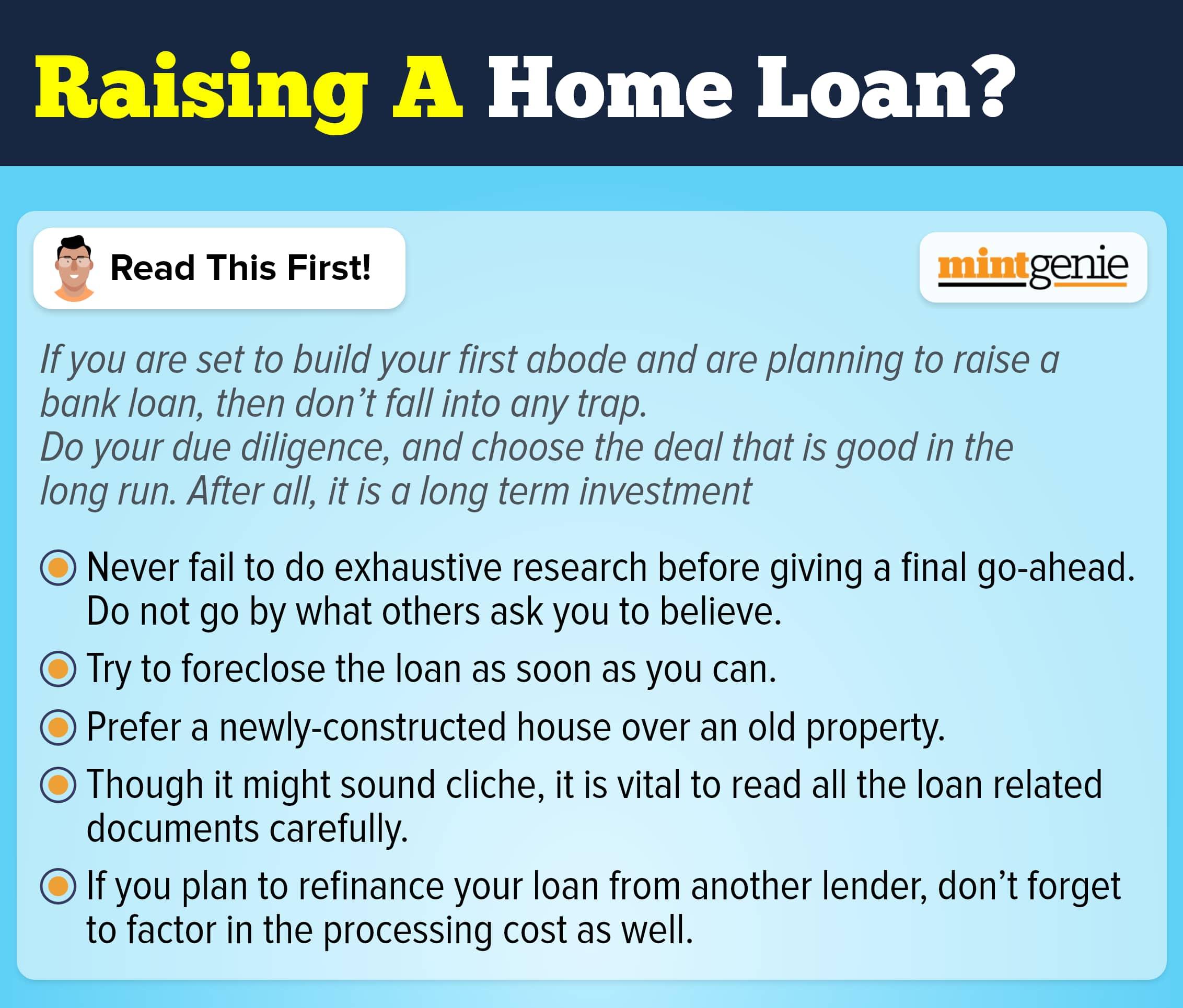

The Monetary Policy Committee (MPC) of the Reserve Bank of India (RBI) decided to hike the policy repo rate by 35 basis points to 6.25 percent on December 7. The central bank has taken multiple rate hikes this year to control rising inflation.

| Date of Update | Repo Rate |

| September 30, 2022 | 5.90% |

| August 05, 2022 | 5.40% |

| June 08, 2022 | 4.90% |

| May 2022 | 4.40% |

Subsequently, the lenders passed on the rise in interest rate to borrowers who either opted for higher equated monthly instalments (EMIs) or chose increased loan tenure. Borrowers now fear the banks may again respond to the repo rate hike by passing on its effect to them.

Consider, for example, you have a home loan worth ₹75 lakh that you are repaying at 8.20 percent interest rate. The hike in repo rates means that the bank will charge higher interest, henceforth. This implies increased EMIs or an increased loan tenure to repay the debt sought.

Shrikant Shrivastava, Chief Risk Officer, India Mortgage Guarantee Corporation, said, “Most banks have fully passed on the repo rate increase of 190 bps to the consumers of home loans till date. This rate hike of 190 bps has resulted in a loan tenor increase of ~ 13 years for borrowers who had initially opted for 20 years loan period, assuming they had taken a home loan at six at the time of home purchase. Alternatively, those borrowers who opted for an EMI increase instead of a loan tenor increase have seen their EMI go up by ~20 percent already.”

At 8.20 percent interest, a loan of ₹75 lakh sought for 20 years will beget an EMI of ₹63,670. The EMI goes up to ₹69,665 for the same amount of loan taken at 9.45 percent interest for 20 years. Assuming that the borrower does not have the necessary monetary means to pay off the extra interest burden, the renewed loan tenure is 335 months. This way, the total interest outgo would be ₹13,829,450 and the total amount of loan repaid would amount to ₹21,329,450. This means that those not willing to extend the loan tenure will have to shell out an added instalment of ₹5,995 every month.

Considering that the increase in instalments is not too high, one may opt to pay higher EMIs and get rid of the loan in due time. The added monthly outgo will take a beating on middle class’ savings already struggling under the rising effect of inflation.

What should borrowers do?

Many borrowers make the mistake of ignoring the statements corresponding to their monthly outgo. Borrowers must be aware of the interest rates they are being charged. This becomes more important if the interest rates have risen and the banks are either charging higher EMIs or extending the loan tenure.

Seeking a longer loan tenure will only increase the burden of the total loan repayment. It makes more sense to repay more than the EMIs stipulated by the bank.

Loan prepayment is a known concept though many find it difficult to prepay the loan amount in lump sum chunks. Instead of prepaying the loan in a lump sum at sporadic intervals, you may resort to the same but do it every month in small instalments.

Numbers speak more than words, so the following table will help you to understand how paying ₹1000 extra every month can help bring down the loan tenure and consequently the total loan outgo.

| Loan repayment (sans prepayment) | |||||

| Loan Amount | Interest rate | EMIs | Loan tenure | Total interest | Total loan amount repaid |

| ₹75,00,000 | 9.45% | ₹69,665 | 241 months | ₹92,19,633 | ₹1,67,19,633 |

| Loan repayment by repaying over and above the EMIs | |||||

| Loan Amount | Interest rate | EMIs | Loan tenure | Total interest | Total loan amount repaid |

| ₹75,00,000 | 9.45% | ₹70,665 | 231 months | ₹88,23,615 | ₹1,63,23,615 |

| ₹75,00,000 | 9.45% | ₹71,665 | 222 months | ₹84,09,630 | ₹1,59,09,630 |

| ₹75,00,000 | 9.45% | ₹72,665 | 214 months | ₹80,50,310 | ₹1,55,50,310 |

| ₹75,00,000 | 9.45% | ₹73,665 | 207 months | ₹77,48,655 | ₹1,52,48,655 |

| ₹75,00,000 | 9.45% | ₹74,665 | 200 months | ₹74,33,000 | ₹1,49,33,000 |

| ₹75,00,000 | 9.45% | ₹75,665 | 194 months | ₹71,79,010 | ₹1,46,79,010 |

Paying more through EMIs gradually will limit the effect of interest rate volatility on loan tenure. This means instead of carrying the loan burden for an extended period, one may close the loan ahead of schedule.

An increased loan tenure binds you to debt for a prolonged period and forces you to spend more on the interest component. Prepaying the loan can be hard on many people, especially, those with no access to a secondary income source. However, saving more by curtailing down on unwanted expenses or resorting to a freelance gig will ensure that you are not only able to prepay but also get rid of the lingering debt. Additionally, one may liquidate his fixed deposits to repay the loan considering how the home loan interest rates exceed the interest one earns on bank deposits.

Prepaying the loan is a known but ignored concept considering how many people refrain from extra EMIs without realising that it will result in them repaying a higher loan amount than intended.