For many parents, true financial freedom means giving their kids the best education they can. This dream often pushes them to explore colleges outside India, to provide their children the opportunity to study at some of the world's top institutions. Yet, the rising cost of education can cast doubts on this aspiration. However, with prudent financial planning and commitment, this dream can transform into a reality.

Keeping that in mind, let’s explore the ideal way to build a corpus for your child's future education plans.

1. Getting a realistic estimate of the cost

While you might not know which course your child will pursue, you can estimate costs by checking the fees of top colleges for various courses. Consider factors beyond tuition, such as living expenses, insurance, travel, and unforeseen circumstances. For instance, a four-year undergraduate program in the USA might cost $80,000 to $200,000 in tuition fees, with living expenses of around $25,000 per year. This sums up to a corpus ranging from ₹89 lakhs to ₹1.8 crores ($1 = ₹82), depending on factors such as the university, course, location, and more.

2. Consider inflation and currency depreciation

These figures merely scratch the surface, as they don't consider inflation, currency fluctuations, and the possibility of unforeseen financial challenges. Therefore, it's essential to factor in these variables for a realistic financial blueprint.

Considering around 4% inflation and approximately 3% currency depreciation and a 15-year period, the total corpus needed could range anywhere from ₹~2.45 cr to ₹~4.96 cr.

Considering the example above and assuming there are 15 years till college, parents would need to invest around ₹59,000 monthly, assuming a 10% annual return to reach the target corpus of ₹2.45 crores.

3. Consider how much you can invest and when you can start

Ideally, parents should start saving and investing in their child’s education as soon as possible. The more time they have on their side, the more their investments can grow and compound over the years.

Considering the example above and assuming there are 15 years till college, parents would need to invest around ₹45,000 monthly, assuming a 10% annual return to reach the target corpus of ₹1.08 crores. While the numbers might appear daunting, increased savings and income over time can bridge any shortfall. Additionally, scholarships, fee waivers, and education loans could help close the gap between your investment and the required corpus.

4. Where should you invest?

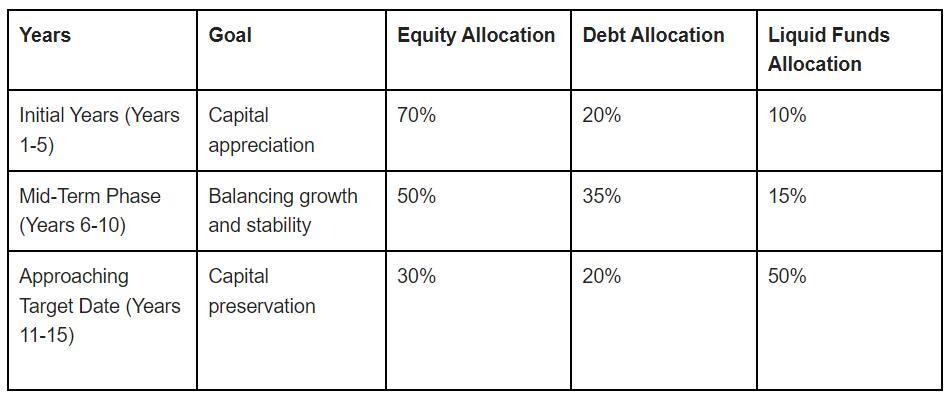

Target date investing is a method tailored for long-term financial goals like funding education. This strategy revolves around adjusting your investment portfolio's asset allocation as your target date (the year your child starts college) draws nearer.

In the initial years, when there's ample time for investments to grow, a more aggressive allocation towards high-growth assets is suitable. These could include equity mutual funds which have the potential to yield substantial returns over the long run.

As the target date edges closer, it's prudent to rebalance the portfolio to mitigate potential market volatility. This involves reducing the exposure to high-growth assets and increasing allocation to relatively stable options like debt mutual funds.

In the final stretch leading up to the target date, capital preservation becomes paramount. Shifting the allocation towards more conservative assets like debt mutual funds or liquid funds helps safeguard against sudden market downturns.

Let's illustrate the concept with an example of how asset allocation can be structured over the course of 15 years starting in 2023. Keep in mind that these percentages are examples and should be customised based on individual risk tolerance, financial goals, and market conditions.

An example of dynamic asset allocation for fulfilling long-term financial goals

Remember, these percentages are just a hypothetical example. Consulting with a financial advisor is essential to tailor your asset allocation to your specific circumstances and risk tolerance. Additionally, periodic reviews and adjustments are crucial to ensure your investment strategy remains aligned with your evolving goals and the ever-changing market conditions.

The takeaway

In a world of rising education costs, realising the dream of providing a top-tier international education for your child demands meticulous planning. By gauging expenses, starting early investments, and adopting a dynamic asset allocation strategy, parents can navigate this long financial road with ease.

Naveen K R is the Senior Director of Investments at Windmill Capital Private Limited. Windmill Capital is a SEBI registered research analyst creating Thematic & Quantamental curated stock/ETF portfolios.