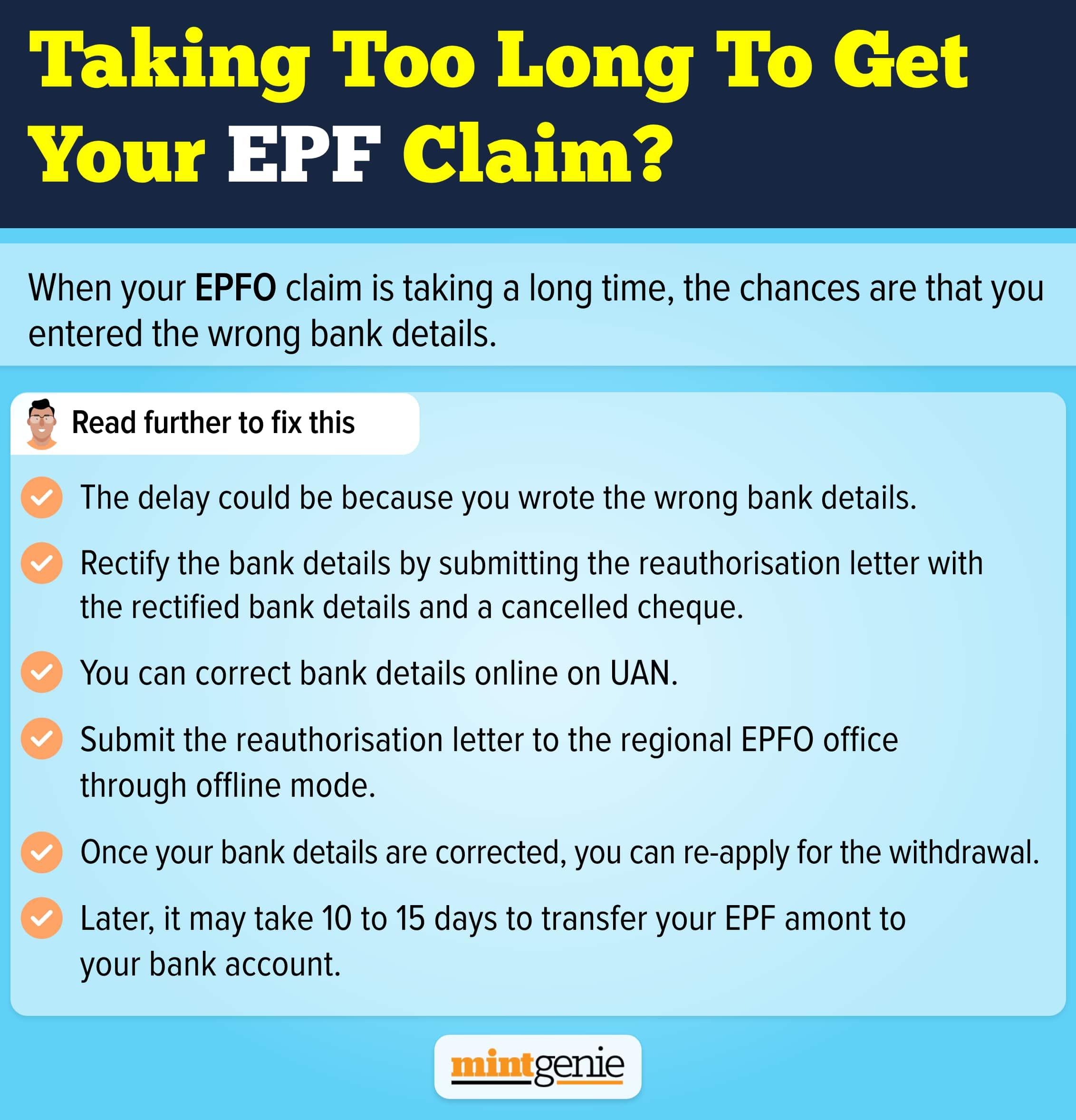

Have you ever checked how your Employees’ Provident Fund (EPF) is faring? Do you bother to look at how your regular contributions to your EPF account have amounted to planning for your retirement? Many people look at their EPF accounts as just another kind of recurring or savings account from which they can withdraw money in need. Though regulations by the Employees’ Provident Fund Organization (EPFO) prohibits its employed subscribers from withdrawing money, some people make unwarranted misuse of the exemptions and relaxations allowed. For example, you can withdraw up to 75 per cent of your EPF balance money if unemployed for a month. You can withdraw your entire money if you have been unemployed for more than two months.

To withdraw or not to withdraw

It is not unusual to see how many people withdraw a major portion of the corpus accumulated to invest and spend the money their way. A lump-sum withdrawal during festivals is nothing short of a bonus. These people either spend or invest the sum in fixed income plans available at very low-interest rates. The reason behind this folly is their ignorance of the law of compounding that enables the creation of a huge corpus in the long run. As the famous physicist Albert Einstein had once quoted, “Compound interest is the eighth wonder of the world. He who understands it earns it … he who doesn’t … pays it.”

Talking of investment, your money will grow in numbers and volume only when you allow it enough time to grow. Instead of frantically shuffling between various investment options, you can work your way towards more money by not touching your EPF corpus. Even when you leave one organization to join another, you can transfer your EPF account to the next organization and let it grow.

The compounding effect

If you are still wondering how retaining your money in your EPF account year after year while allowing it to accumulate at regular intervals helps, first understand how EPF works.

First, know that 12 per cent of your basic salary is credited to your EPF account every month. Your employer then matches the contribution by contributing 12 per cent from its end. The total amount is bifurcated into contributions under the Employees’ Pension Scheme and the rest to the EPF scheme – 8.33 per cent of the total contribution is credited to the Employees’ Pension Scheme while the remaining 3.67 per cent is added to EPF. There is no age limit to the contributions as long as you are employed with a contributing organization. The total amount when credited month on month helps in building a corpus that you can fall back upon post-retirement.

Consider the following two scenarios to understand how the money in your EPF grows. Since the EPF rates change every year, we have used a 7% standard interest rate for all calculation purposes.

The calculations for both scenarios have been shared by Ayush Goel, Designated Partner, BAS & CO. LLP |Chartered Accountants|.

Scenario 1: Assume the contribution made to your EPF account every month is ₹2500 and the contribution has been made non-stop for 10 years.

| Calculation of total amount a person will get after keeping money account in EPF account for 10 years | |

| Interest Rate | 7% |

| Payment frequency per year (Monthly frequency of contributions) | 12 |

| Interest rate every month | 0.0058 |

| Number of years for which equal contributions have been made | 10 |

| Total period during which contributons have been made (in months) | 120 |

| Amount of contribution every month (in Rs) | 2500 |

| Total accumulated corpus after 10 years (in Rs) | 4,32,712 |

Scenario 2: Assume the contribution made to your EPF account every month is ₹2500. Though the contributions were made for 10 years, intermittent withdrawals were made at the end of the second year, fifth year and eighth year. The amount withdrawn at the end of the second year was ₹50,000 while ₹100,000 was withdrawn at the end of the fifth year. Again, ₹50,000 was withdrawn at the end of the seventh year.

| Calculation of the total amount the person will have in his EPF account after 10 years (post three withdrawals in between) | |

| Interest rate per annum | 7% |

| Frequency of contributions made every year | 12 |

| Interest rate every month | 0.0058 |

| Number of years during which EPF contributions have been made | 10 |

| Total period during which EPF contributions have been made | 120 |

| Amount of EPF contribution every month (in Rupees) | 2500 |

| Post calculation of interest for first and second year | |

| Total amount accumulated at the end of the second year (in Rs) | 64,203 |

| Amount withdrawn at the end of the second year (in Rs) | 50,000 |

| Amount available in EPF account at the beginning of the third year (in Rs) | 14,203 |

| Calculation of accumulated corpus (Principal + Interest) from the third year to the fifth year | |

| Interest on ₹14,203 for three years + Principal at the beginning of the third year (in Rs) | 17,511 |

| Cumulative amount (Principal + Interest) on ₹2500 contributed every month for three years | 99,825 |

| Total amount at the end of the fifth year (in Rs) | 1,17,336 |

| Amount withdrawn at the end of the fifth year (in Rs) | 1,00,000 |

| Amount left in the EPF account at the beginning of the sixth year (in Rs) | 17,336 |

| Calculation of accumulated corpus (Principal + Interest) from the sixth year to the seventh year | |

| Interest on ₹17,336 for two years (Sixth Year + Seventh Year) + Principal at the beginning of the sixth year (in Rs) | 19,934 |

| Cumulative amount (Principal + Interest) on ₹2500 contributed every month for two years (in Rs) | 64,203 |

| Total amount at the end of the seventh year (in Rs) | 84,136 |

| Amount withdrawn at the end of the seventh year (in Rs) | 50,000 |

| Calculation of accumulated corpus (Principal + Interest) at the end of the seventh year (in Rs) | 34,136 |

| Calculation of accumulated corpus (Principal + Interest) from the eighth year to the 10th year | |

| Interest on ₹34,136 for three years (Eighth Year + Ninth Year + Tenth Year) + Principal at the beginning of the eighth year (in Rs) | 42,087 |

| Cumulative amount (Principal + Interest) on ₹2500 contributed every month for three years (in Rs) | 99,825 |

| Total amount (in Rs) | 1,41,913 |

| Total amount collected at the end of the tenth year (in Rs) | 1,41,913 |

Withdrawing money from your EPF account can seem like an easy choice, especially, when the money is taken out in lump sum. Letting your money stay and grow may seem difficult, though not an impossible choice to make. While the EPFO has announced the lowest interest rate in more than 40 years, you cannot discount the importance of including EPF in your retirement planning. The choice is yours – show conviction in your earnings and let it accumulate or squander the money on avoidable spending.