Women are said to have a penchant for numbers. Their complexities can leave even the most intelligent minds appalled and fumbling for answers. Despite their immaculate understanding of figures and their importance in daily lives, women are constantly haunted by the myth of not being good with investments and taxes. Unfortunately, some women attach so much seriousness to this myth that they leave investment decision-making to the men in their families.

The rise of women entrepreneurs has put to rest many unfounded myths surrounding women and their ability to plan their finances. The misconception that women are unable to manage anything beyond personal and household budgets must be nipped in the bud. However, before we embark on a journey to ensuring women their right to complete financial freedom, it is necessary to take a look at the age-old myths that continue to hold them back.

Myth 1: That children’s education precedes retirement planning

Ask any woman her priorities and she will rank family and children at the top. That their children must be educated is the goal that most women cherish. To ensure that their children do not fall short of money while pursuing their careers, many women have relegated their retirement planning to the backburner. What many of them fail to realize is that while their children’s education can be funded through education loans, retirement planning mandates early and regular savings coupled with timely investments.

It is important to start planning for your retirement from the day you get your first salary in hand. Staying invested for prolonged periods adds to the corpus owing to the compounding effect. Also, the money set aside for retirement must not be redirected toward other goals. So, even if you do not earn a regular salary, make sure to invest your regular savings to create a sizeable corpus for your old age

Myth 2: Women cannot handle risks

The fair gender has courage, but cannot endure risk. This myth has caused many women to shift to less risky investment options as opposed to parking money in equity instruments that yield high returns only if you stay invested for a long period. However, the risk factor is also high in these investment options. However, the data suggest how women prefer to put their money in fixed-income securities considering their risk-averse nature. Unfortunately, some women shift to putting all their money in fixed and recurring deposits or post office schemes after getting burdened with family responsibilities. Increased frequency of career breaks is also one of the reasons for uncertainties in income and investment decisions. The current volatility in the market may imply an aversion to equity investments, thus, prompting many to look for safe investment options like Public Provident Fund, National Savings Certificates, etc. However, for the money to grow, it is important to stay invested for a prolonged period. This is because the effect of risk gets mitigated with time. The fundamental rule of growing wealth is to invest regularly for a prolonged period to benefit from the compounding effect.

Myth 3: The glitter of gold attracts them like none

You will not find any woman who does not love gold. The affection for the yellow metal transcends their endearment for all other things or investment options. For many women, gold whether bought or inherited constitute the key ingredients in their portfolios. However, their overdependence on the value of gold often diverts from investing in other investment options like equity instruments. However, securing all your money in only one kind of asset can spell trouble in the long run. It is important to diversify your portfolio across asset classes, viz., equity for high returns and debt for stability coupled with moderate stability.

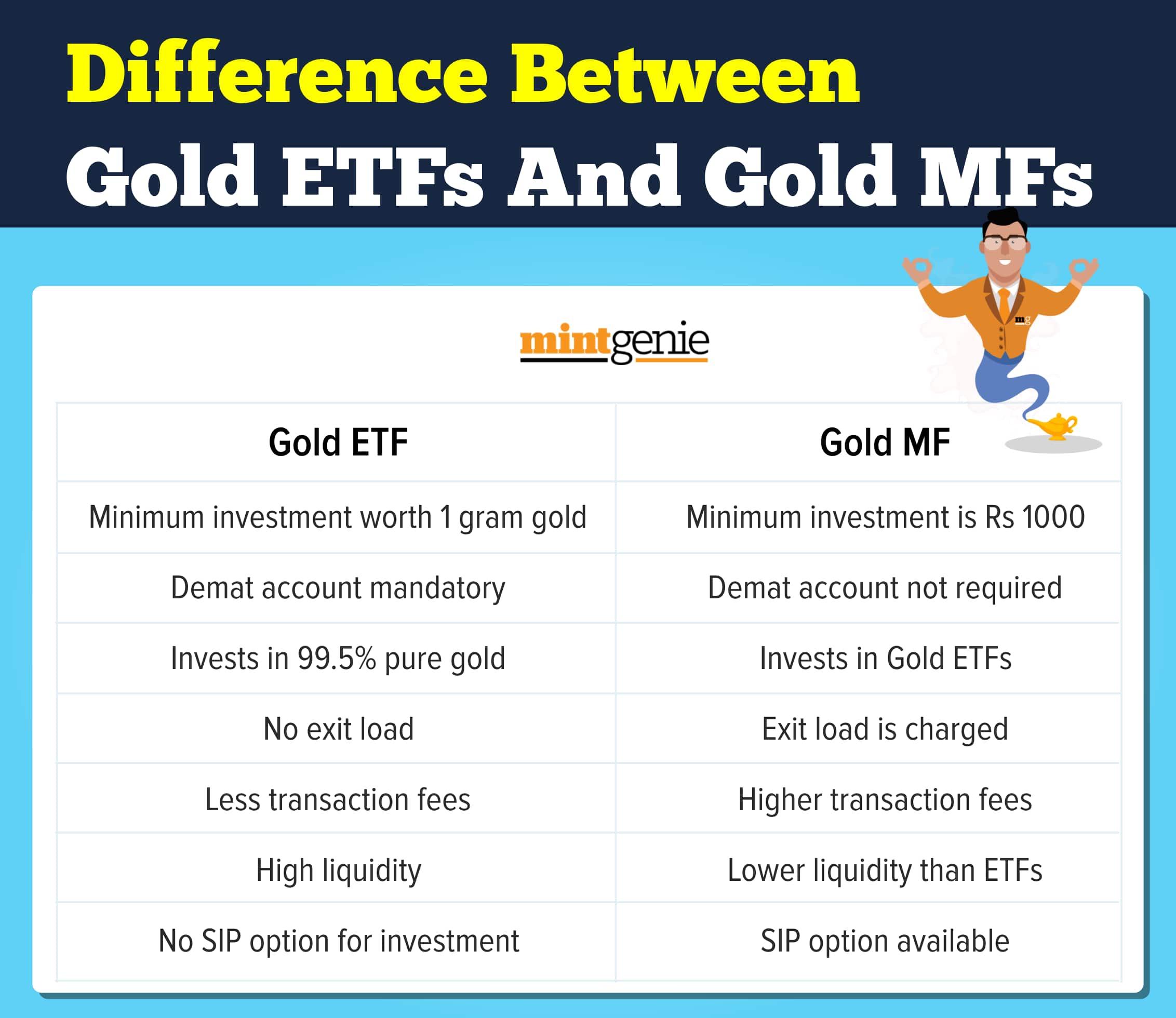

Also, investing in physical gold can be difficult for fear of loss or theft. Prefer alternate gold investment options like gold ETFs and sovereign gold bonds (SGBs). When inflation strikes, the price of gold automatically goes up. Investing in SGBs or gold ETFs ensures a hedge against inflation along with liquidity. Most financial planners recommend investments in gold ETFs and gold bonds to clients who have not yet invested in gold.

Myth 4: Post-marriage, all investment decisions must be taken jointly

Agreed that financial compatibility is the key to a successful marriage. While women may plan and chalk out important financial decisions like buying a house, planning children’s education and retirement planning with their husbands, it makes sense for them to make individual decisions regarding their finances. While joint financial planning is important, women must not shy away from their personal wealth creation goals either. While contributing to joint financial goals, make sure not to lose sight of personal financial goals too.

Myth 5: Let the husband decide

A common factor underscoring most women in India is that they leave financial planning decisions to their husbands. Like it or not, even working women refrain from deciding how to invest or save their money for the future. Women who want to take charge of their lives must first keep a tab on their money and investments. This will help them experience financial independence in an absolute sense, sans any unwanted or unwarranted interference. Women today are more able investors and entrepreneurs. Their investments goals are all-encompassing owing to their ambitious outlook.

For the women of today, nothing is impossible. For them, freedom is synonymous with financial freedom and that comes from making the right investment decisions by themselves.