Thousands of people are losing their jobs as some of the biggest consulting and tech companies are laying off their employees to tackle the effect of the global recession. Besides, the slow growth in various sectors owing to global economic turmoil has translated into mass layoffs in small and mid-sized companies as well.

As these layoffs are likely to continue with more to come, chances are that many people would find themselves financially distressed in the coming months. While you may cut down on your lifestyle expenses, paying for your needs may also be difficult if you do not have adequate corpus in your emergency fund.

The time has come to check if you are financially prepared in case of a sudden layoff. Instead of waiting for your company to strike your name off its payroll, it will do a lot of good if you plan your coming six months’ expenses way ahead of your unemployment status if it is likely to be happen.

You must adhere to the following steps:

Ensure savings at every step

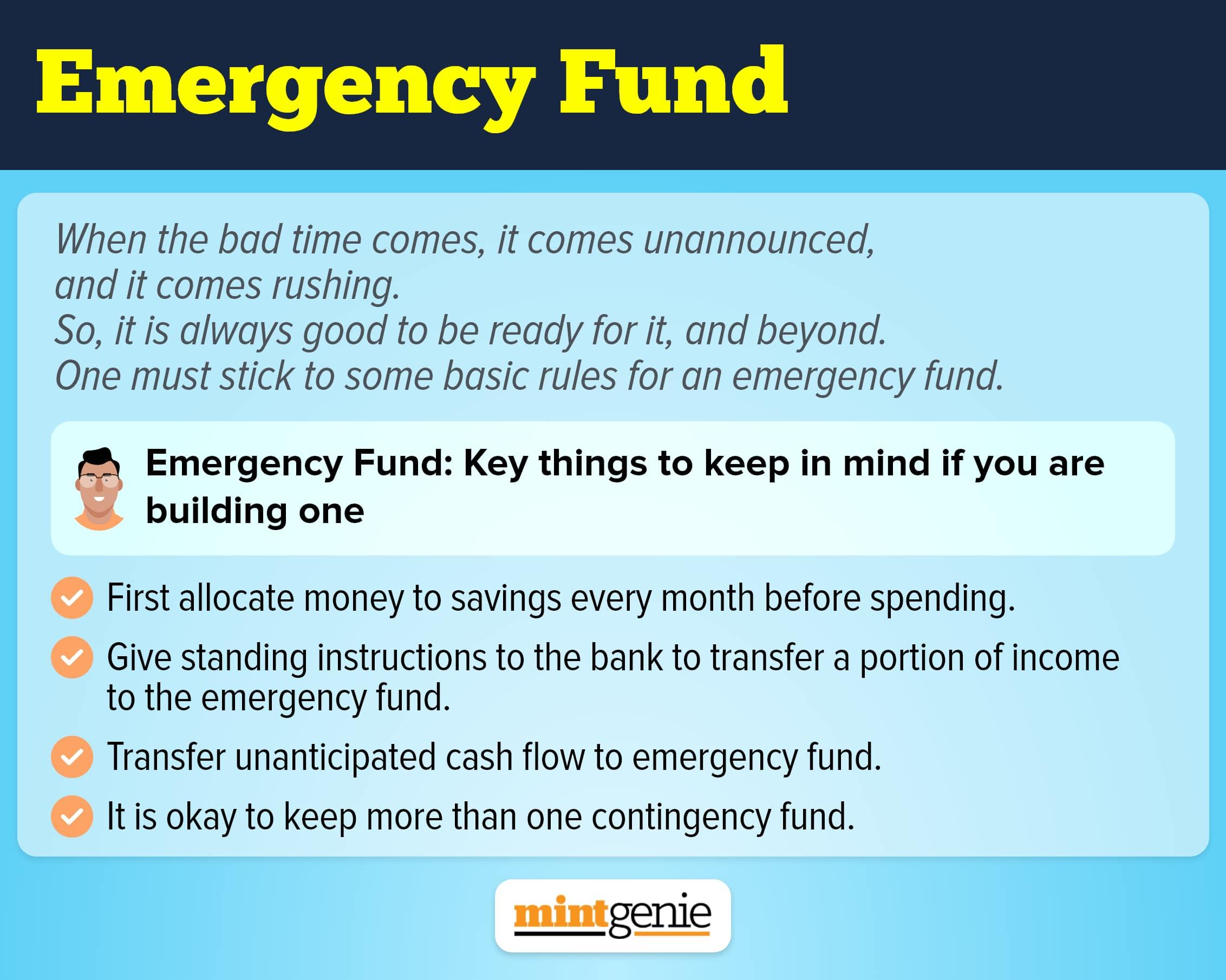

You are dependent on your monthly salary. However, this does not mean that you must leave your savings account bereft of money when you do not have income credited to your account. Your earnings must be different from your savings and investments, which is why you must set up three different accounts dedicated to each one of them.

While the income is credited to your salary account, your savings get accumulated in a separate bank account, the amount set aside for investment in an altogether different account while the remaining can be used to pay off your expenses. To ensure that you have enough savings left in your bank account, automate your savings. This means that a part of the salary credited to your account must automatically be transferred to your savings account on a particular date.

This is not difficult if you synchronize the same with your monthly payout, thus, allowing you to set aside some savings before you use the remaining money to invest or spend on your daily essentials. Inculcating this disciplined savings habit will ensure timely and continued savings as and when necessary.

Continued investing through SIPs

Investing is much needed to build your desired corpus, which is why you cannot dare to ignore the same. Regular investing helps to benefit from the cost-averaging effect. The magic of compounding acts only when you continue to invest wherein you earn not only on your principal investment but also the interest income earned on it. Investing is now easy, thanks to various apps and sites available on the web. Once you have decided how much you want to put in through systematic investment plans (SIPs), ensure that your SIP investments continue to be in sync with your financial goals.

Have enough emergency corpus in place

Emergencies do not come knocking at your door to warn you of the tough times ahead. You never know when your company decides to get rid of your services or hire a cheaper alternative. With artificial intelligence replacing human intelligence, many employees are gradually getting insecure about their jobs.

To tackle sudden unemployment, you must have an emergency fund in place. Planning such a fund will ensure that you have enough money to pay for your essential expenses and will keep you financially afloat till you get your next job.

An emergency fund is a fund that is only used in times of emergency. To start an emergency fund, open a simple savings bank account in which you deposit a percentage of your income on a regular basis.

Once you have a sizable corpus, you can also invest the extra amount in a liquid fund or short-duration fund or fixed-income plan depending on your assumption of emergencies, the extent of cash in hand, your risk profile and your ability to continue contributing to the fund. Keep in mind that your emergency fund should be at least six to twelve times your monthly expenses.

Review your debt repayment plan

Do you have any overriding debt that you must pay off in time? However, the sudden loss of your job may disable you from repaying your loans on time. To determine if you will be able to repay your debts in the event of being laid off, it is critical to analyse your monthly debt payments. Your debt repayments may be an upcoming loan, an equated monthly instalment (EMI), or borrowings you made for particular dates or events.

You must make a complete list of all the monthly or yearly payments along with information on how you plan to repay your debt and any precautionary steps you have taken to initiate an irregular revenue stream. In case, you are unable to repay your loan due to financial constraints stemming from job loss, you may consider transferring your loan amount to a lender charging a lower interest rate. You may also consider transferring the remaining loan amount to a lender willing to lend for a prolonged tenure. This is because a longer loan term translates to cheaper EMIs for the same loan amount, thus, significantly lessening the load on the borrower.

To lessen or mitigate the EMI load, you may also want to consider lenders availing of loans with a moratorium advantage, particularly for semi-constructed properties.

Reining in spending habits

Shopping mindlessly can be addictive. This problem can be acute if you are constantly glued to the web to shop online. By making a list of the things you want to buy and setting a spending limit, you may avoid being careless with your money. Spread out the amount you want to spend on vanity things over a few months to make sure you don't go overboard in one month and prevent cash burnout. It can be challenging to restrain from impulsive spending habits, and it takes a lot of financial discipline to get oneself out of an unwanted mess.

Have a budget in place

The most effective technique to establish a daily budget is to write down your needs in a journal that you use to guide your monthly purchases of necessities. An enduring financial habit, daily budgeting helps you control your spending on necessities and prevents you from making excessive purchases when you are enticed by product firms’ clever marketing tactics. Most importantly, before you spend, keep in mind your earnings, savings, and how much you can afford to pay without damaging your monthly or yearly budget.